Tax breaks for entrepreneurs. Tax breaks for individual entrepreneurs

According to the current legislation, SPs that maintain their own tax and accounting records can receive certain benefits.

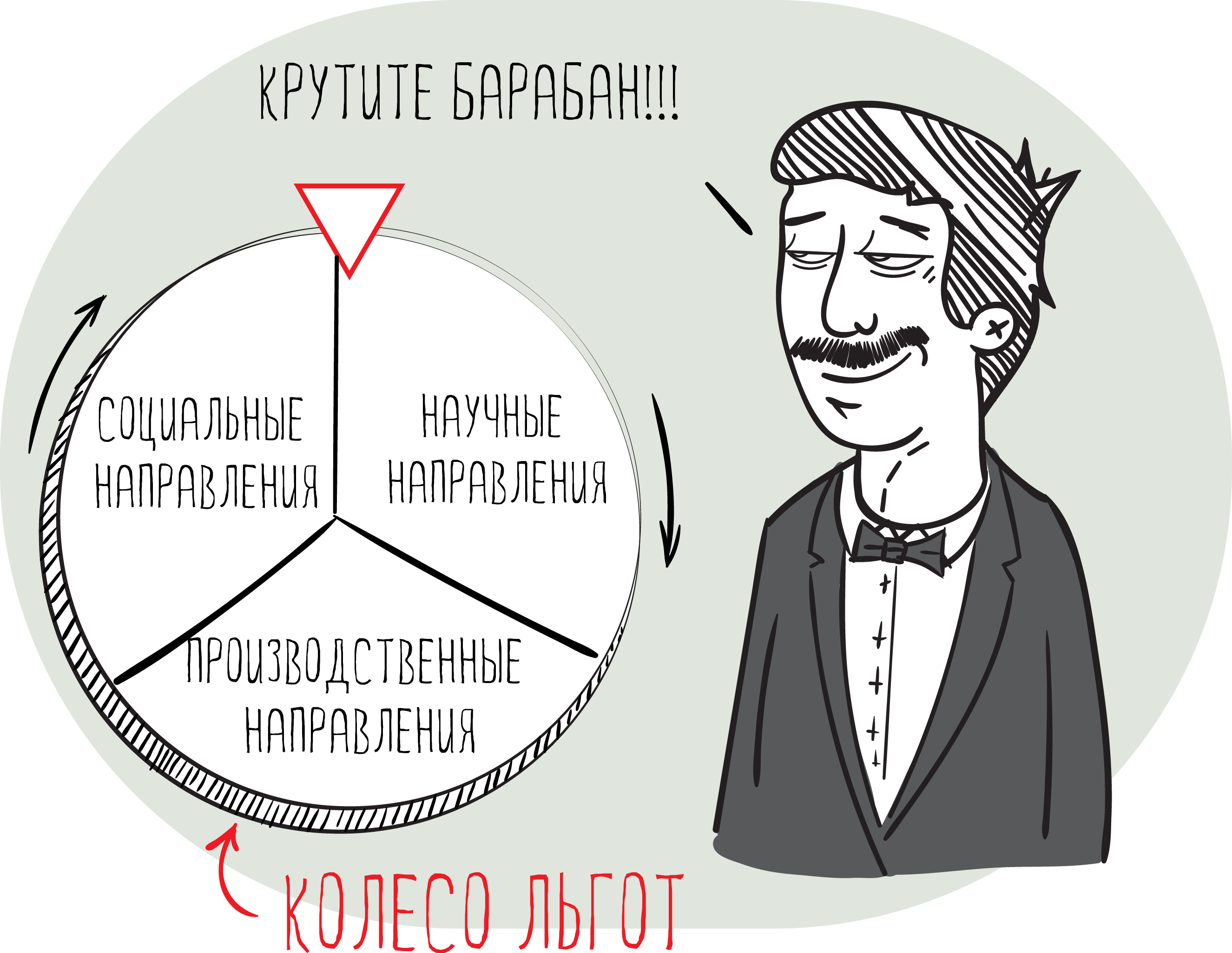

This opportunity can be used by entrepreneurs who, within 2 years after registering their un, have switched to the simplified taxation system or PSN and are engaged in scientific, social or industrial activities.

An additional condition for obtaining benefits is the determination of the minimum amount of income from a business, which according to the letter of the Ministry of Economic Development No. D05-136 dated January 19, 2011, cannot be less than 70%.

PI exempt from accounting

In accordance with the Federal Law No. 129 of November 21, 1996, which regulates the procedure for of accounting, entrepreneurs are exempt from bookkeeping. These benefits were retained even after the adoption and approval of the new Federal Law No. 402 of December 6, 2011.

If a unit operating on a simplified taxation system maintains accounting for its activities, then the procedure for maintaining it should comply with the requirements specified in the Tax Code of the Russian Federation, ch. 26.2.

Reducing the amount of tax on the payment of insurance premiums

The SP is entitled to pay a reduced amount of simplified tax when paying insurance premiums and benefits issued as a result of the acquisition of temporary disability by employees. This is governed by art. 346.21 p. 3 of the Tax Code of the Russian Federation.

The total amount of the deduction may not exceed 50% of the total amount accrued for payment of tax. This restriction does not apply to SPs who do not make payments. individuals and those who pay insurance premiums to the funds of the OMS and Pension Fund of the Russian Federation in the amount determined on the basis of the cost insurance year. This provision is governed by the Federal Law of the Russian Federation №212 Art. 1 p. 8 of July 24, 2009

Only un are entitled to receive these benefits, which can document the type of their activities, which must necessarily comply with the provisions of the letter of the Ministry of Healthcare and Social Development of the Russian Federation “1335-19 of April 14, 2011

Tax deductions at reduced tariff rates in the total amount can be 26%:

- FFOMS - 3.1%

- PF - 18.0%;

- FSS - 2.9%;

- MHIF territorial level - 2.0%.

What is the installment plan and deferral of fees and taxes?

The procedure and the list of granting a delay in payment of fees and taxes is governed by Art. 64 of the Tax Code. These benefits are granted by un if:

- There are clear signs of bankruptcy due to the payment of the full amount of the tax by the entrepreneur;

- There is a fact of causing material damage to the applicant as a result of a man-made disaster, natural disaster or due to other force majeure circumstances;

- The production of un or the sale of its products has a seasonal character;

- The entrepreneur has delayed the provision of commitments on budget limits and / or allocations to the interested party;

- Other cases that are marked by the legislation of the Russian Federation.

The installment plan for payment of fees and taxes may be provided for one or a group of taxes. The delay in payments is valid for 1 year. An entrepreneur may receive such benefits at the tax authority by submitting a relevant application for consideration.

How do I pay VAT?

If the entrepreneur does not work on the simplified payment, he is obliged to pay VAT. If for the last three calendar months the amount of income from the sale of products (services) does not exceed 2 million rubles in total, un exempted from paying VAT.

Not pay VAT may also be persons who provide a number of services in the territory of the Russian Federation, provided they have the appropriate license. This category of services includes conducting classes in sports and developmental sections, clubs or studios in which minor children study. This condition is governed by Art. 149 point 2 subparagraph 4 NK the Russian Federation.

Additional subsidies and subsidies

Unemployed citizens of the Russian Federation who decide to start their own business can receive additional benefits in the form of subsidies and subsidies from the employment authorities. The amount of material assistance is 58,800 rubles, which is equivalent to the maximum amount of unemployment benefits, increased 12 times. The same amount can be obtained also for the organization of jobs for all potential employees. Uni can also expect to receive other compensation payments, which is provided for regional programs business support and entrepreneurship.

Documents allowing to receive tax deductions in the form of subsidies and subsidies:

- Passport of a citizen of the Russian Federation;

- A document confirming the status of the applicant as "unemployed";

- Diploma of Higher / Secondary Education;

- Application in writing (executed in the prescribed manner) with a request to provide subsidies to the person;

- A business plan that economically justifies obtaining financial support. The business plan must necessarily reflect the planned amount of costs that are expected to go to the organization and development of business.

The decision to grant the applicant benefits is mainly based on the estimated costs that will go to:

- The organization of jobs in the required quantity for the employment of temporarily unemployed citizens of the Russian Federation;

- Payment of wages, the amount of which should not be lower than the minimum established in the region. At the same time, the entrepreneur undertakes to pay the wages due to the employees during the entire term of the subsidies in a timely manner.

For example, municipal funds that support small businesses and entrepreneurship help start-up businessmen in terms of allocating funds for the purchase of technological equipment (equipment, etc.). In some cases, the amount of the benefit may be 350,000 rubles, but this amount is paid exclusively on co-financing terms, when the entrepreneur invests a similar amount in the development of his project.

The applicant’s personal funds are set off when he contacts tax authorities with a request to register it as a legal entity or an individual entrepreneur.

Subsidies granted for limited activities

According to the order of the Ministry of Economic Development of the Russian Federation No. 227 of May 20, 2011, which reflects the provisions of the small business support program, there is a clause providing for the transfer to entrepreneurs of mechanisms, devices vehicle and equipment leased.

These benefits are provided from the federal budget and are directed to:

- Subsidizing costs that are associated with the payment of leasing payments by a medium and small business entity. The amount of subsidies may not exceed 2/3 of the refinancing rate of the Central Bank of Russia, established at the time of payment by the entrepreneur of the amount of interest;

- Providing targeted grants that rely on start-up business entities and are paid for the development and organization of business. Also, these benefits are provided to business entities and legal entitieswho work in the chosen direction less than 1 year. Grants are awarded free of charge, subject to the share of financing for expenses incurred to repay the initial payment for leased equipment. The amount of the grant can be up to 1 million rubles. no more;

- Subsidizing the payment of the initial fee, subject to the conclusion of the contract for the leasing of machinery, vehicles or equipment.

Along with subsidies and subsidies, un can expect to receive preferential conditions for payment transport taxif their activity is related to the carriage of goods or passengers.

There are also a number of loan programs designed for business entities. Providing loans at lower interest rates carried out by regional branches of banks participating in the program to support small and medium-sized businesses.

By contacting the tax authorities, the entrepreneur can claim to receive a property deduction, subject to the registration of the purchased real estate in your name or using your status as an individual.

This condition is governed by the letter of the Ministry of Finance of the Russian Federation No. 03-04-05 / 3-489 dated July 06, 2011. The document notes that the business entities operating on the simplified tax system do not apply property deductions regarding the payment of taxes on personal income.

In the Moscow region, work continues to create an enabling environment for small and medium-sized businesses (SMEs). Thanks to an attractive background, more than 9,000 SMEs were opened in the region last year. The authorities of the region expect that 2017 will also be “prolific” for new enterprises - this year it is planned to open 10 thousand SMEs.

Business support measures

The entities of small and medium-sized businesses are enterprises whose number of employees does not exceed 250 people, for small businesses - from 16 to 100 people, for joint ventures - from 101 to 250 people. All of them can count on state support at the federal, regional and municipal levels. At the same time, it is available only for officially registered subjects. You can apply for registration of an IP on the regional site.

Federal level

- Subsidies for reimbursement of part of the cost of paying interest on loans.

- Subsidies for the compensation of part of the cost of using energy resources and the maintenance of jobs.

- Subsidies for the development of engineering.

- Subsidies for the implementation of seasonal purchases of raw materials for the organizations of light and textile industry.

- Subsidies in the form of a property contribution of the Russian Federation to the Rostec Group of Companies for projects to create mass production of machine-tool products under the Machine Tool Industry industry subprogramme of the state program Development of Industry and Improving its Competitiveness (http://base.garant.ru).

Also, small business in Russia for three years is protected from scheduled inspections - from January 1, 2016, the country was introduced to such events. The Cabinet of Ministers of the Council of the Federation believes that the moratorium will help to create favorable conditions for the development of small business in Russia.

Regional level

Nadezhda Osodoeva

Take time out

Vacations are good, but “tax holidays” are even better. To make it easier for start-up entrepreneurs to get on their feet, the state exempted them from paying one or several taxes. This turned out to be a great incentive for newbies, since tax reporting is a difficult business. But do not be very happy: the holidays will last only 2 years from the date of registration of the IP. Who can afford such a vacation, now find out.

Important points

The grace period for individual entrepreneurs during which they are exempted from paying taxes is called “tax holidays”. According to Art. 346.20 of the Tax Code of the Russian Federation at the level of amendments to the legislative act FZ No. 477 of 29.12. 2014, changes were made according to which the regional authorities of the Russian Federation have the right to establish zero tax rate for sp. The official entry into force of the law took place on January 1, 2015. Benefits are available until 2020.

Regional authorities can introduce a “tax holiday” for individual entrepreneurs for 2 years, as well as independently set their start date and order. If an entrepreneur wants to take advantage of "tax holidays", he needs to make sure that this federal legislation has already been adopted in his region. List of regions in which the "tax holidays", you can see.

Regional authorities can introduce a “tax holiday” for individual entrepreneurs for 2 years, as well as independently set their start date and order.

Terms of use

Not all entrepreneurs can use the right to “tax holidays”.

- New PI, registered for the first time. If the entrepreneur has suspended his activities for a period, the re-opening of the IE does not give him the right to enjoy the benefits.

- "Tax holidays" can take the PI, working on a patent or USN. If an entrepreneur has transferred to these types of taxation within 2 years from the date of registration, he will also have benefits.

- “Tax holidays” can be used by individual entrepreneurs who have opened after the region has adopted a law on the entry into force of a grace period.

Attention! The period during which the entrepreneur is exempt from taxation is only the first 2 years of its activity. However, he is obliged to keep a record of income during this time, as well as to make mandatory contributions of pension and insurance payments to extra-budgetary funds.

Regional authorities have the right to impose additional restrictions on the granting of “tax holidays” to individual entrepreneurs (for example, benefits are not granted to individual entrepreneurs with the amount of income above the established amount (Art. 249 of the Tax Code of the Russian Federation) or there are more employees in the enterprise than the norm).

Areas of activity

In developing this legislation, a number of restrictions were imposed on the types of activities to which these benefits would be granted (clause 4 of Article 346.20 of the Tax Code of the Russian Federation). Privileges can be used by individual entrepreneurs whose fields of activity are as follows:

- social;

- production;

- scientific.

The list of areas of activity falling under the "tax holiday" covers about 40 destinations. This is the production of medical equipment, textiles, computing equipment, cellulose, the provision of social services, scientific work. During the “tax holidays” in Moscow, the authorities expanded this list to include tutoring, transfers, and sightseeing activities.

The volume of income of IP, received in the provision of services, works or sale of goods, upon completion tax term must be at least 70% of total income.

Tax Holidays in 2017

From 2016, it is allowed to use the patent system (PSN) without workers. They can get a patent in a simplified manner and use the "tax holiday" at a rate of 0%.

Patents may be received by individual entrepreneurs whose activities cover the following areas:

- tailoring of leather goods;

- forestry;

- livestock grazing services;

- collection and sale of medicinal plants;

- catering services;

- translation (orally or in writing);

- use of forest resources;

- care services for people with disabilities and older people;

- fishing

Also, the regional authorities significantly expanded their powers in 2016. They have the right to independently determine:

- The boundaries of the introduction and transition to tax holidays.

- Nuances in specifying the tax base.

- Types of activity of IP that can use the patent system of taxation.

- The tax rate depends on the taxpayers and the scope of activities of the individual entrepreneur.

- Tax exemptions and the process of their application.

“Tax holidays” is a powerful incentive for start-up entrepreneurs, which allows minimizing the tax burden. Such benefits provide significant support to small businesses and allow you to expand your business activities.

In this article we will try to prepare answers to questions about what tax benefits for individual entrepreneurs can be obtained. For example, in which cases, an individual entrepreneur may refuse to maintain accounting, or receive preferential tariffs for paying insurance premiums, as well as how to get a deferment on tax payment.

Are PIs required to maintain accounting records?

According to the law 129-ФЗ, adopted on 21.11.1996, individual entrepreneurs are not obliged to keep accounts. The same privilege was preserved even when the law No. 402-ФЗ was passed 06.12.2011. At the same time, the legislation established that all organizations and entrepreneurs who have chosen the simplified taxation system should keep records of their income and expenses in the prescribed manner.

It turns out that an entrepreneur may not keep accounting records, provided that he will keep documents confirming the income and expenses received.

Application of preferential tariffs

Since 2011, tax incentives for individual entrepreneurs have been operating that affect insurance premiums according to USN. At the same time, an entrepreneur falls under the benefits only if he is engaged in the main types of activities specified in the OKVED and falling into the list specified in paragraph 8 of the first part of article 58 Federal law. In order to receive a reduced rate, an individual must confirm its type of activity.

The preferential activities include:

Food production;

Textile manufacture;

Chemical production;

Wood processing;

Car manufacturing;

Production of soft drinks;

Furniture manufacture;

Production of sports equipment;

Manufacture of toys;

Scientific research;

Recycling of secondary raw materials;

Building;

Education and other activities.

One of these types of activities can be recognized as main only if the share of income from the sale of its products is more than 70% of the total income.

Tax breaks for individual entrepreneurs can reduce the rates of insurance premiums to the size of 26%. The percentage of contributions is distributed as follows:

18% in the Pension Fund;

2.9% to the Social Insurance Fund;

3.1% to the Health Insurance Fund;

2% to territorial health insurance funds.

How can I reduce the tax

This method of tax reduction will be available only to entrepreneurs located on the simplified system of the "income" system. They have the opportunity to reduce their insurance contributions, as well as receive benefits for temporary disability. At the same time, the amount of the deduction cannot be more than 50% of the accrued tax. For individual entrepreneurs paying insurance premiums to the Pension Fund of the Russian Federation, as well as not making payments or any other remuneration to individuals, this restriction does not apply.

For example, if the taxpayer paid the amount of insurance contributions in the amount of 140 thousand rubles, and the amount of his tax amounted to 260 thousand rubles, according to the third paragraph 346 of the article, the SP has the right to reduce the amount of his tax by 50%, i.e. 130 thousand rubles (260000 rubles. / 2). Thus, the entrepreneur can save on the payment of taxes in the amount of 130 thousand rubles.

How can I defer payment of taxes?

The list of grounds on which a deferment can be obtained for the payment of taxes is regulated by Article 64 of the Tax Code.

Thus, it turns out that the delay can be provided to the entrepreneur, whose financial position does not allow paying the tax within a strictly fixed period, but at the same time, there is no reason to believe that the entrepreneur will not be able to pay the debt in the future. At the same time, granting a delay is allowed only if there is one of the following reasons:

1. The damage was caused to the entrepreneur as a result of a natural disaster or other disaster.

2. Budget allocations or budget commitments were not provided on time.

3. The entrepreneur was threatened with bankruptcy if he paid the tax.

4. The sale of a product or its other services is seasonal.

At the same time, tax breaks for individual entrepreneurs in the form of a delay can be presented for several taxes at once. The installment period should not exceed one year. To obtain such benefits, you must write a statement to the tax authority.

VAT exemption

Any entrepreneur who does not use the simplified payment system is obliged to pay VAT. But there is an opportunity to get rid of the payment of VAT.

Article 145 of the Tax Code states that individual entrepreneurs may be exempted from compulsory payment of their duties if in the last three months the amount of income received from the sale of services or goods did not exceed two million rubles.

Moreover, it is possible to get benefits for paying VAT and in the provision of certain types of services. For example, if an entrepreneur has organized his own circle or section and conducts classes for minors. For more information about other types of services, you can find out in article 149 of the Tax Code.