Federal budget revenues gratuitous income. The regional budget crash is getting closer

INTRODUCTION

1. NON-GRAVE LISTINGS: CONCEPT AND STRUCTURE

1.1 Budget classification of income

1.2 Gratuitous transfers as a form of inter-budgetary relations 2. ANALYSIS OF NON-INTERFERRED TRANSFERS TO THE RF BUDGETS

2.1 the Structure and trends of budget revenues of the Russian Federation

2.2 Analysis of intergovernmental transfers (for example, Alagir district) 3. WAYS TO IMPROVE BUDGET FINANCING OF RUSSIAN

FEDERATIONS

3.1 Inter-budget transfers coming from the federal budget 3.2 Inter-budget transfers coming from the budgets of entities Russian Federation

3.3 Inter-budget transfers coming from the local budget

CONCLUSION

LIST OF USED SOURCES Appendix A

Appendix B

INTRODUCTION

One of the mechanisms allowing the state to carry out

economic and social policy, is the financial system

society and its state budget.

Using the state budget, government authorities

receive financial resources for the maintenance of the state apparatus,

implementation of social events, implementation of economic tasks,

those. to carry out the functions assigned to it by the state.

The modern system of budget financing is implemented by all

budgets included in the budget system of the country within

intergovernmental relations.

The budgets of the Russian Federation are divided into three types:

Federal budget

Budgets of constituent entities of the Russian Federation

Local budgets

All budgets are independent and are not included in each other, i.e.

budgets of constituent entities of the Russian Federation are not included in the federal budget, but local

budgets are not included in the regional budget.

Budgets have income-generating sources inherent in

various levels budget system in accordance with the budget

classification and Budget code of the Russian Federation.

One such source is gratuitous transfers to

budgets. It is this type of income that we will consider in this

course work.

Inter-budget transfers are transferred from both budgets

higher level budget system lower level budgets

(for example, from the FB to regional budgets), and in the reverse order

(for example, from regional and local budgets of the FB), as well as

be provided within one level of the budget system (for example, from

budget of the municipal district to the budget of settlements).

This approach to regulating intergovernmental fiscal relations in general

justified because it allows you to more effectively align the social

the economic situation of municipalities formed on

the territory of the subject of the Russian Federation, and between the subjects of the Russian Federation.

So, the goal of this study is comprehensive, reliable

study of gratuitous transfers. From the goal, we highlight the following tasks:

Consider budget classification of income;

To characterize gratuitous transfers, and determine them

structure;

Explore gratuitous transfers as a form of intergovernmental

transfers;

Analyze budget revenues (including gratuitous) for

various levels;

Identify ways to improve intergovernmental funding.

The subject of the study are gratuitous transfers.

The object is the budget system of the Russian Federation (federal

budget, budget of the constituent entities of the Russian Federation, local budgets).

When writing a term paper applied analysis methods,

economic methods.

The information and methodological basis of the work are

legislative documents (Budget Code of the Russian Federation),

economic statistics, scientific works of Russian scientists,

periodicals.

The selected topic is relevant, and is of interest to the researcher.

In addition, these issues are not sufficiently covered in the educational literature.

So, let's move on to the consideration of gratuitous transfers -

a special source of budget funding.

1. NON-GRAVE LISTINGS: CONCEPT AND STRUCTURE

1.1 Budget classification of income

A budget is a form of education and expenditure of a monetary fund

funds intended for financial support of tasks and functions

state and local government.

Central to the financial system of any state is

state budget - a lawful financial plan

state (list of income and expenses) for the current (financial) year.

The new Budget Code of the Russian Federation defines the budget as

“The form of formation and expenditure of the cash fund,

intended for financial support of tasks and functions of the state

and local government. ”

Thus, the state budget gives state power

the possibility of maintaining the state apparatus

social events, the implementation of priority economic tasks,

those. performance by the state of its inherent functions.

The budget system of the Russian Federation consists of budgets of three levels:

· The first level is the federal budget of the Russian Federation and

budgets of state extra-budgetary funds;

· The second level - the budgets of the constituent entities of the Russian Federation (89 budgets - 21

republican budget, 55 regional and regional budgets, 10 district

budgets of autonomous okrugs, budget of the autonomous Jewish region,

city \u200b\u200bbudgets of Moscow and St. Petersburg) and budgets

territorial state extra-budgetary funds;

· The third level - local budgets (about 29 thousand city,

district, village and rural budgets).

Classification of budget revenues of the Russian Federation

based on legislative acts of the Russian Federation,

determining sources of revenue generation of budgets of all levels

The structure of budget revenues is shown in Fig. 1.

Fig. 1 Budget revenue structure

In reality, their ratio is not the same and

determined by various factors:

The nature of monetary and financial policies;

The economic condition of the country;

Political and economic conditions;

The specific features of the historical period.

In accordance with Art. 41 Budget Code of the Russian Federation,

budget revenues at all levels of the budget system of the Russian Federation - federal

budget, budgets of constituent entities of the Russian Federation and local budgets - are divided into

tax, non-tax and gratuitous transfers. They found their

reflected in the classification of budget revenues of the Russian Federation (Appendix 2 to the Law on

budget classification), which includes five income groups:

1) tax revenues;

2) non-tax revenues;

3) gratuitous transfers;

4) income of targeted budget funds;

5) income from entrepreneurial and other income-generating

activities.

Section 2 of the commented article defines the composition tax revenue.

Tax revenues include those provided for by tax

russian legislation federal, regional and local taxes and

fees and penalties and fines.

But we describe in more detail gratuitous transfers.

According to paragraph 5 of article 41 of the Budget code of the Russian Federation, to

gratuitous and irrevocable transfers include transfers to

Financial assistance from budgets of other levels in the form

subsidies and subsidies;

Subventions from the Federal Compensation Fund and (or) from

regional compensation funds;

Subventions from local budgets to budgets of other levels;

Other gratuitous and irrevocable transfers between

budgets of the budget system of the Russian Federation;

Gratuitous and irrevocable transfers from budgets

state and (or) territorial state extra-budgetary

Gratuitous and irrevocable transfers from individuals

and legal entities, international organizations and governments

foreign states, including voluntary donations.

We give the definitions of the above enumerations:

Grants are budget funds provided to the budget of another

level of the budget system of the Russian Federation at no cost and

irrevocable basis.

Subventions are budget funds provided to the budget

another level of the budget system of the Russian Federation or

legal entity on a gratuitous and irrevocable basis on

the implementation of certain targeted costs.

Subsidies are budget funds provided to the budget

another level of the budget system of the Russian Federation, the physical

or to a legal entity on the basis of equity financing of targeted

expenses.

Common for subsidies, subventions and subsidies is their free

and irrevocable in nature. A distinctive feature of subventions and subsidies from

subsidies is their target. And subventions and subsidies

differentiated by the amount of financing: due to the subvention completely

certain targeted expenses are financed, and subsidies are provided

on conditions of shared financing of target expenses.

It should be noted that subsidies, subventions and subsidies as methods

allocation of financial resources to territorial budgets

imperfect. These sources of budgets lack incentive features,

they create a dependent mood in local administrations. Such

the practice of transferring funds does not contribute to the development of economic

initiatives of local administrations, reduces their impact on

economic processes in the territory and reduces on this basis

the possibility of overfulfilling the revenue side of their budgets weakens

financial control.

However, noting all the negative aspects of subsidies, subventions and

subsidies, completely eliminate them as methods of vesting territorial

budgets by necessary means is impossible. With a formal approach to

solving the problem of liquidating the subsidies to these budgets and transferring them to

large deductions from unsustainable sources of income

situation may be worsened. This will result in a permanent cash register

gaps and the need for multiple applications for loans from

higher budgets. In general, this will complicate the financing of planned

events.

Therefore, not everywhere and not always should strive to replace subsidies,

subventions and subsidies by any means. They are necessary in those

settlements where, due to prevailing conditions and ongoing

environmental policies, historical availability

monuments and other reasons, economic potential cannot be

expanded in size to provide territorial

revenue generation. Local sources are not able to provide

covering the necessary expenses. Examples are cities and

resort towns, cities - historical and architectural reserves,

research centers and others. Subventions should be issued for the intended purpose

for certain events for which local implementation is not

enough money.

Gratuitous transfers are classified by their source

receipt: from non-residents; budgets of other levels; state

extrabudgetary revenues; government organizations; supranational

organizations; funds transferred to targeted budget funds; other

gratuitous transfers.

Budget revenues may also include gratuitous transfers.

by mutual settlement 1.

It should be noted that in different sources, it is treated differently as

income structure, as well as its individual sources. In particular, sometimes

gratuitous transfers are referred to as transfers (financial assistance).

This source of income is adopted exclusively in countries with complex

budget system consisting of several budget levels. For

most regional and especially local entities they have

a large role, since they make up a significant share of their income

budgets, reaching in some cases 70-80%. Characteristic

subsidies and subventions serves a targeted nature. So it could be help

to maintain minimum budgetary security or

specific functions (administrative, military, environmental, etc.)

authorities of administrative-territorial formations.

1 Mutual settlements are understood as operations involving the transfer of funds between budgets of various levels in the event of changes to the tax or budget legislation of the Russian Federation, when transferring powers to finance expenses or transfer revenues that occurred after the approval of the budget law and therefore are not taken into account in it.

Gratuitous transfers relate to own income

budgets i.e. full fixed income

partially for the relevant budgets by the current legislation.

But, it should be borne in mind that financial assistance (subsidies, subventions,

subsidies) does not apply to own revenues of the corresponding budget

and the state extrabudgetary fund.

1.2 Gratuitous transfers as a form of intergovernmental

the relationship

All budgets included in the budget system of the country are interconnected

in the framework of intergovernmental relations.

Inter-budgetary relations are relations between bodies

state power of the Russian Federation, state bodies

authorities of the constituent entities of the Russian Federation and local authorities

self-government related to the formation and execution

relevant budgets.

Transfers are funds received from the federal and

regional funds for financial support to regions whose size

calculated according to the methodology and formula established by the government.

Intergovernmental relations are formed at the expense of intergovernmental

transfers.

The very concept of intergovernmental relations is broader in terms of

in relation to the concept of inter-budget transfers, inter-budget

transfers are provided and used as part of intergovernmental

relations, but the current chapter 16 of the RF BC does not focus on

these issues and generally does not draw a parallel and interconnection

intergovernmental relations and intergovernmental transfers, limited to

only the definition of intergovernmental relations in Art. 6 BC RF “Concepts and

terms used in this Code. ”

To analyze the basics of providing intergovernmental transfers

it is necessary to identify key concepts and their relationships:

Gratuitous and irrevocable transfers. As already mentioned,

they include not only transfers in the form of financial assistance (subsidies

and subsidies) and subventions to budgets of other levels of the budget system, but

gratuitous and irrevocable transfers from state budgets

and (or) territorial state extra-budgetary funds, as well as

gratuitous and irrevocable transfers from physical and legal

persons, international organizations and foreign governments,

including voluntary donations;

But in order to disclose the stated problems, we will be interested

only those irrevocable and gratuitous transfers that come

from the budget of one level of the budget system to the budget of another level

budget system of the Russian Federation.

A budget loan is a form of financing budget expenditures,

which provides for the provision of funds legal entities or

another budget on a repayable and reimbursable basis;

Budget loan - budget funds provided to another

budget on a refundable, gratuitous or reimbursable basis for a period not

more than six months within a fiscal year;

State or municipal loan (borrowing) - transfer

into the ownership of the Russian Federation, the subject of the Russian Federation or

municipality cash that is Russian

Federation, subject of the Russian Federation or municipality

undertakes to return in the same amount with payment of interest (fee) in the amount

2. ANALYSIS OF NON-INTERFERRED TRANSFERS TO THE BUDGETS OF THE RUSSIAN FEDERATION

2.1 the Structure and trends of budget revenues of the Russian Federation

Consider the structure and trends of budget revenues of the Russian

Federation, including focus on gratuitous

income.

In the Russian Federation, as in the USSR and other former states

socialist camp, in 1991-1995. receipts from

privatization of state property and issue of credit money.

The latter took place during the period of socialism, but was of a hidden nature.

The specifics of the budget system of the Russian Federation suggests a system

distribution of income between specific budgets -

federal, constituent entities of the Federation and local, as well as extrabudgetary

funds. The federal budget revenues include:

Own tax revenues;

Own non-tax revenues;

Funds for mutual settlements from the budgets of constituent entities of the Russian Federation, others

gratuitous transfers;

Revenues of federal targeted budget funds;

Funds from federal social extrabudgetary funds.

General structure of federal budget revenues in 2005-2008

presented in table 2.1.

Table 2.1. - Dynamics of the structure of the federal budget of the Russian Federation, billion

Indicator 2005 2007 2008

Total revenue

1. Tax income 2. Non-tax

3. Target income

budget funds 4. One

social tax (UST)

federal laws on the implementation of federal budgets for 2005-2008

As can be seen from table 1.1, these revenues are the main; on

federal level, donations do not play practically

no role.

The structure of budget revenues is developing somewhat differently.

subjects of the Russian Federation. Budget revenues of the Russian Federation are formed primarily due to

own and regulatory tax revenues.

The general structure of the regional consolidated budget is reflected in

Table 2.2 - the structure of the income of the consolidated budget

territories of the Russian Federation in 2008, billion rubles Total indicator Including:

on budgets

subjects of the Russian Federation

by local

budgets

1. Tax revenues

2. Non-tax

3.Free

listing 4. Target income

budget funds

Total revenue

Internal turnover Total revenue

Note. Here is the data on the consolidated budget of the entities

RF are used from source: Consolidated Performance Report

of the territory budget, form code 0524108. - www.minfin.ru.

Analyzing the data, we can conclude that most

budgets of the territories of the Federation is formed by tax revenues.

Their share in the consolidated budget of the regions amounted to 57.5%, in

budgets of constituent entities of the Russian Federation - 59.8%, and in local budgets - 53.6%.

But, a significant share of territorial budget revenues

represented by gratuitous transfers (13.2% of the budgets of entities)

and domestic turnover (40, 1% of local budgets).

They play a particularly important role for local budgets,

practically along with tax revenue (40.5% or 286.7 billion

Consider more detailed gratuitous transfers to local

budgets on the example of the Alagir district in the next paragraph.

2.2 Analysis of intergovernmental transfers (for example, Alagirsky

district)

Based on indicators of intergovernmental transfers in Alagirsky

area for 2007-2008 (see Appendices A, B), analyze the percentage

execution of the budget of municipal districts, and also the budget of urban and

rural settlements.

Percentage of budget execution of municipal districts for the period

2007 and 2008

Budget execution of municipal districts took place in

insignificant.

Grants received in one hundred percent of the volume, according to the approved

decreased by 1.21%, and for subsidies by 3.77%.

Budget funds transferred to the budgets of municipal districts

for the implementation of the Federal Targeted Investment Program

executed in one hundred percent in 2007, and the rest are free

revenues from other budgets of the budget system by 94%.

The analysis of indicators is presented in table 2.3.

Table 2.3 - Percentage of budget execution of municipalities for

period 2007 and 2008 (rub.)

Indicators 2007%

execution

2008% execution

Gratuitous receipts, including:

Subsidies from others

budget budgets

rF systems

Subventions from

other budgets

budget system of the Russian Federation

Facilities,

received on

compensation for additional costs,

arising from

decisions taken

authorities of a different level

Subsidies from

other budgets

budget system of the Russian Federation

Facilities

budgets transferred

municipal budgets

areas for the implementation of the Federal Address

investment

programs

gratuitous receipts from others

budget budgets

The percentage of budget execution of urban and rural settlements for

period 2007 and 2008

Budget execution of urban and rural settlements took place in

in accordance with the decision of the Assembly of representatives of the Alagir district.

Deviation in the percentage of execution received from the republican

budget of gratuitous receipts for the period since 2007 to 2008

insignificant.

The execution of subsidies in 2008 was exceeded by 0.58%.

In 2008, the performance of subventions compared to 2007

decreased by 6.42%.

Funds received to compensate for additional costs,

arising from decisions taken by the authorities of another

levels were provided only in 2007 and executed in one hundred percent

The findings are reflected in the summary table 2.4.

Table 2.4 - the percentage of budget execution of urban and rural

settlements for the period 2007 and 2008 (rub.)

Indicators 2007% execution

2008% execution

Plan Fact Pl

Gratuitous

receipts, including:

Grants from other budgets

budget system

Russian Federation

100 312 00000,00

Subventions from other budgets

budget system

Russian Federation

Facilities,

compensated

additional

expenses

resulting from decisions

adopted by authorities

authorities of a different level

Now we will analyze the structure of gratuitous transfers, their

shares and dynamics. Why, let's build table 2.5.

Table 2.5 - the Structure and dynamics of gratuitous transfers for

Alagir district Municipal indicators

Urban and rural

settlements

Grants from other budgets

budget system of the Russian Federation,%

Subventions from others

budget system budgets

Russian Federation,% Other non-paid

income%

As you can see, in 2008 compared with 2007 the structure of gratuitous

revenue has undergone significant changes: in the budget

in municipal districts, the share of subsidies decreased (by 12.7%) and increased

subventions (by 27.8%). Whereas, in the budget of urban and rural

settlements, on the contrary: subsidies increased (by 12.1%) and other free

revenue declined. In general, subsidies are the main

percentage of gratuitous transfers.

3. WAYS TO IMPROVE THE BUDGETARY

FINANCE

To improve budget financing is carried out

budget alignment, which is divided into vertical and

horizontal.

Vertical alignment is the process of achieving a balance between

the volume of liabilities of each level of government for expenditures with its potential

income resources (tax revenues).

At a higher level liabilities are imposed: in the event that

potential revenue opportunities for

lower level insufficient to finance those assigned to

functions, the central government is obliged to provide this

regional or local government missing budget

resources. Central government, possessing far more than any

region, economic regulation opportunities and volumes

tax revenue should compensate for the imbalance of regional

budgets at the expense of funds accumulated at the federal level

Vertical alignment must certainly be combined with

horizontal, meaning a proportional distribution of taxes and

subsidies between the subjects of the Federation to eliminate inequality in

the possibilities of various territories caused by territorial

factor.

Thus, it turns out that the federal budget expenditures for

solving social and economic problems of the federal scale

also added are the costs of achieving a balanced budget

system (subsidies to balance the level of budget

security).

The basis of the organization of vertical budget regulation

laid down principles that stimulate a decrease in deficit

budget, for example - the existing methodology for allocating funds

Federal Fund for Financial Support of Regions (transfers). First

part of it goes to the so-called “needy” regions,

the second - to the “especially needy". “Needy” is a region

whose average per capita incomes are lower than the average for Russia, “especially

needy ”- a region whose budget expenditures are higher than its income, then

there is a budget with a deficit. Thus, the cost overrun of regional

budgets based on this technique will be automatically covered from

federal budget. The natural result of this is that

the desire of the federal government to reduce the budget deficit

encounters economically determined confrontation between regions.

3.1 Intergovernmental transfers coming from the federal

the budget

Inter-budget transfers from the federal budget to budgets

1. Subsidies for equalizing the budgetary provision of the constituent entities of the Russian Federation,

which are distributed among the subjects of the Russian Federation in accordance with a single

methodology approved by the Government of the Russian Federation in accordance with

requirements of the BC RF. Grants form the Federal Fund for Financial

support of the subjects of the Russian Federation.

The project of distribution of subsidies for equalizing budget

security of constituent entities of the Russian Federation between constituent entities of the Russian Federation is included in

State Duma as part of the draft federal law on

the federal budget for the next fiscal year and planning period and

approved when considering a draft of the specified federal law.

In this case, approval for the planning period is allowed

unallocated between the subjects of the Russian Federation volume of subsidies for equalization

budgetary provision of constituent entities of the Russian Federation in the amount of not more than 15% of the total

the volume of these subsidies approved for the planning year of the planned

period, and not more than 20% of the total volume of these subsidies approved

for the second year of the planning period.

provided to the subjects of the Russian Federation, the level of settlement of which

does not exceed the level set as a leveling criterion

estimated budgetary provision of the constituent entities of the Russian Federation.

The level of estimated budgetary provision of the subject of the Russian Federation

determined by the ratio between the estimated tax revenues for

one resident who can be received by the consolidated budget

subject of the Russian Federation based on the level of development and structure of the economy and tax

base, and a similar indicator on average for consolidated

budgets of constituent entities of the Russian Federation, taking into account the structure of the population, socially -

economic, geographical, climatic and other objective

factors affecting the cost of providing the same volume

state and municipal services per capita.

As part of subsidies for equalizing budgetary provision

subjects of the Russian Federation can be allocated subsidies that reflect individual

factors and conditions taken into account when determining the level of budget

security subjects of the Russian Federation. The volume of these subsidies cannot

exceed 10% of the amount of subsidies for equalizing the budget

security subjects of the Russian Federation.

executive authorities of the subjects of the source data for

calculation of the distribution of subsidies for equalizing budget

security of the subjects of the Russian Federation for the next financial and planning period

executive bodies of the constituent entities of the Russian Federation in the manner established

Ministry of Finance of the Russian Federation.

Grants for equalizing the budgetary provision of the constituent entities of the Russian Federation

for territories, regions, which include autonomous okrugs,

calculated for the consolidated budget of the region, region, including

budgets of autonomous okrugs, and are credited to the budget of a region or territory,

unless otherwise provided by federal budget law and contract

between the state authorities of the region, region and bodies

state authorities of the autonomous region.

2. Subsidies to the budgets of the constituent entities of the Russian Federation, by which

inter-budget transfers provided to the budgets of the constituent entities of the Russian Federation in

co-financing of expenditure obligations arising from

fulfilling the powers of state authorities of the constituent entities of the Russian Federation in

subjects of jurisdiction of the constituent entities of the Russian Federation and subjects of competence of the Russian Federation and constituent entities of the Russian Federation, and

expenditure obligations to fulfill the powers of local authorities

The totality of subsidies to the budgets of the constituent entities of the Russian Federation from the federal

the budget is formed by the Federal Fund for Co-financing of Expenditures.

Subsidies may be included in the federal budget

budgets of constituent entities of the Russian Federation for equalizing the security of constituent entities of the Russian Federation in

in order to implement their individual expenditure obligations.

Purpose and conditions for the provision and expenditure of subsidies to budgets

constituent entities of the Russian Federation from the federal budget, selection criteria for constituent entities of the Russian Federation for

the provision of these intergovernmental subsidies and their distribution

between subjects of the Russian Federation are established federal laws and

normative legal acts adopted in accordance with them

Government of the Russian Federation for a period of at least three years.

The distribution of subsidies is established by federal laws on

the federal budget and regulatory standards adopted in accordance with them

legal acts of the Government of the Russian Federation.

3. Subventions to the budgets of constituent entities of the Russian Federation, by which

inter-budget transfers provided to the budgets of the constituent entities of the Russian Federation in

financial support of expenditure obligations of the constituent entities of the Russian Federation and

municipalities arising in the exercise of authority

RF transferred for implementation by public authorities

subjects of the Russian Federation and local authorities in the established

The totality of subventions to the budgets of the constituent entities of the Russian Federation from the federal

the budget is formed by the Federal Compensation Fund.

The project for the distribution of subventions to the budgets of the constituent entities of the Russian Federation from

the federal budget between the constituent entities of the Russian Federation is introduced into the State

i think in the draft federal law on the federal budget for the next

fiscal year and planning period and is approved when considering

draft federal law.

Subventions granted for the execution of individual expendables

obligations of the constituent entities of the Russian Federation are credited to the budget of the subject and are spent in

the procedure established by federal laws and adopted in

compliance with normative legal acts of the Government of the Russian Federation.

Subventions are distributed among all subjects of the Russian Federation uniform for

the corresponding type of subventions to the method in proportion to the number

population, consumers of relevant state

(municipal) services, other indicators taking into account standards

budget appropriations for the implementation of relevant

obligations of objective conditions affecting the cost of state

(municipal) services in the constituent entities of the Russian Federation

Subvention allocation methods presented by the Government

RF as part of documents and materials submitted to the State Duma

RF simultaneously with the draft federal law on the federal budget

for the next financial year and planning period.

4. Other inter-budget transfers to the budgets of the constituent entities of the Russian Federation, which

provided for by federal laws and adopted in accordance with

normative legal acts of the Government of the Russian Federation, budget budgets

rF systems can provide other inter-budget transfers.

3.2 Inter-budget transfers from budgets

subjects of the Russian Federation

Inter-budget transfers from budgets of constituent entities of the Russian Federation to budgets

the budget system of the Russian Federation are provided in the form of:

1. Subsidies for equalizing the budgetary provision of settlements and

municipal areas (urban districts).

Subsidies for equalizing the budgetary provision of settlements

are provided in the budget of the subject of the Russian Federation in order to align

financial possibilities of settlements for implementation by local authorities

self-government powers to resolve issues of local importance proceeding

from the number of residents and budgetary provision. Subsidies on

equalization of budgetary provision form a financial fund

settlement support.

The volume of these subsidies is approved by the law of the Russian Federation on the budget of the subject

All urban settlements and

rural settlements of the subject of the Russian Federation. The law of the subject of the Russian Federation local authorities

municipalities may be vested with

powers of state authorities of the constituent entities of the Russian Federation to calculate and

the provision of subsidies to the budgets of settlements at the expense of budget funds

subjects of the Russian Federation. Distribution of subsidies for equalizing budget

security of settlements between settlements and their substitutes

additional standards for deductions from personal income tax

to the budgets of settlements are approved by the law of the subject of the Russian Federation on the budget

subject of the Russian Federation.

Subsidies for equalizing the budgetary provision of municipal

areas are provided in the budget of the subject of the Russian Federation in order to align

budgetary provision of municipal areas. Indicated subsidies

form a regional fund for financial support of municipal

These subsidies are provided to municipalities,

the level of budgetary security which does not exceed the level

set as a criterion for leveling the estimated budget

security of municipal areas.

The level of estimated budgetary provision of municipal

areas is determined by the ratio of tax revenues per inhabitant,

which can be obtained by the budget of the municipal district based on

level of development and structure of the economy and tax base, and similar

average for municipal districts and urban districts

given subject of the Russian Federation, taking into account differences in the structure of the population, socially -

economic, climatic and geographical factors affecting

the cost of providing municipal services per inhabitant.

2. Subsidies to local budgets, which are understood as

intergovernmental transfers provided to municipal budgets

entities for the co-financing of expenditure obligations,

arising in the exercise of powers of local authorities

local government.

The totality of these subsidies forms a regional fund

co-financing expenses. Also in the budget of the subject can

leveling subsidies to local budgets

provision of municipalities for their implementation

separate expense obligations.

Purpose and conditions of granting and spending subsidies to local

budgets, selection criteria for municipalities for

the provision of these subsidies and their distribution between

municipalities are established by the laws of the subject of the Russian Federation and

normative legal acts of the highest executive body

state power of the subject of the Russian Federation.

3. Subventions to local budgets, which are understood as

inter-budget transfers provided to local budgets to

financial support of expenditure obligations of municipal

The other day, the authorities again reported on their inefficiency, and this time the case again affects the country's budget. At a meeting of the State Duma Committee on Budget and Taxes, the head of the Accounts Chamber Tatyana Golikova announced that according to data for 2015, 41 constituent entities of the Federation have a budget deficit of more than 10%. Along with this, in 14 constituent entities of the country, public debt is fixed, which exceeds 100% of the region’s budget, which is already contrary to the Tax Code.

Today, the budgets of many regions are experiencing a much greater crisis compared to the federal

Back in 2014, Russian President Vladimir Putin noted that the cheaper the ruble and the higher the dollar exchange rate, the better for the Russian budget - most of the deductions are made by oil and gas revenues and foreign trade revenues, at which the cost of goods and, accordingly, duties and taxes from dollars to rubles. As a result, the state treasury receives more rubles, although at the same time, gigantic inflation is already laid in the national currency. In 2015, due to a similar situation, we were able to slightly compensate for the effect of falling world prices for raw materials, so 2015 ended for the federal budget with a slight minus. Revenues amounted to 13.7 trillion rubles (-6%), expenses - 15.6 trillion rubles (+ 5%). The budget deficit amounted to less than 2 trillion rubles.

At the same time, the budgets of the regions are formed differently, and to a lesser extent have a “recharge” from devaluation - most of them are taxes on corporate profits, taxes on personal income, on property, transport taxes, income from business activitiesVAT. Moreover, more than a third of all revenues accounted for gratuitous income in the form of subsidies, subventions and other transfers from the federal budget, as well as funds allocated by non-residents.

In 2015, most categories of revenues showed growth - for example, income from income taxes increased by 5.6%, from property taxes - 11.6%, from fines and sanctions by 18.6%.

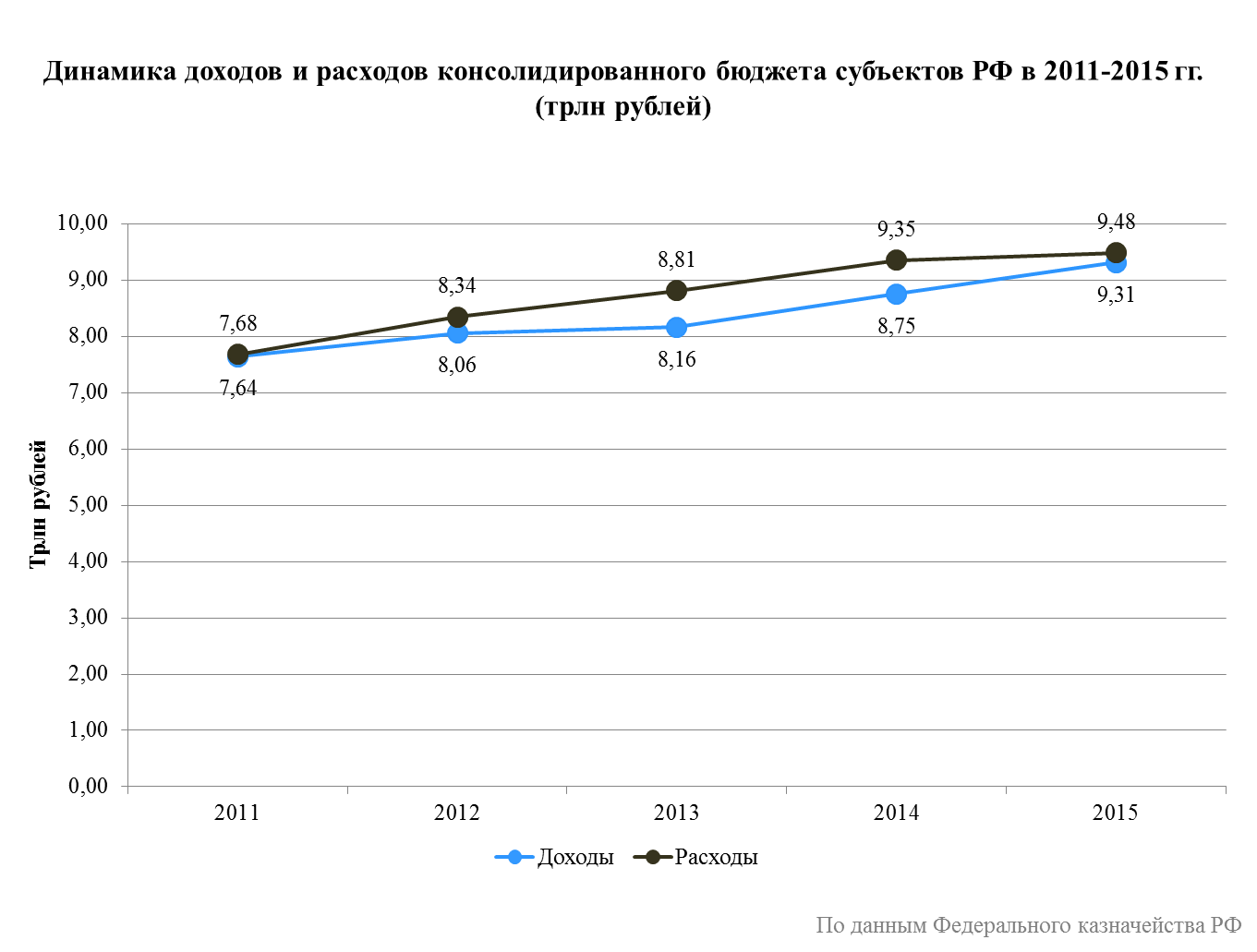

The total amount of budget revenues of entities increased to 9.31 trillion rubles, and expenses to 9.48 trillion rubles. Moreover, the deficit amounted to only about 170 billion rubles. Thus, at first glance, regional budgets even better cope with the crisis than the federal budget.

At the same time, if we analyze the data for individual regions, we can see that many of them barely make ends meet, and the overall positive dynamics are provided by the metropolitan regions, as well as entities where hydrocarbon production is being conducted.

So, for example, the growth of Moscow budget revenues compared to last year amounted to 120.6 billion rubles, Moscow region - 36.96 billion rubles, St. Petersburg - 13.8 billion rubles, Sakhalin region - 67.89 billion rubles.

However, many subjects of the country completed the year, barely exceeding last year's values \u200b\u200bor even with a minus. Among them, the Yamalo-Nenets Autonomous Okrug set an anti-record among them, whose revenues decreased by 24 billion rubles. The reason for this was the general crisis state of the Russian economy, the decline in profits of enterprises and real income population. In addition, many regions in which mechanical engineering was developing showed negative dynamics — some of the foreign automakers left the Russian market, and domestic enterprises significantly reduced their workloads.

Regional budget expenditures, meanwhile, were growing, and the “May decrees" of the president, which provided for various social obligations, in particular the indexation of wages, pensions and benefits, in turn, exerted additional pressure. According to estimates of the Accounts Chamber, about 70-80% of all expenses on them fell on the shoulders of the regions.

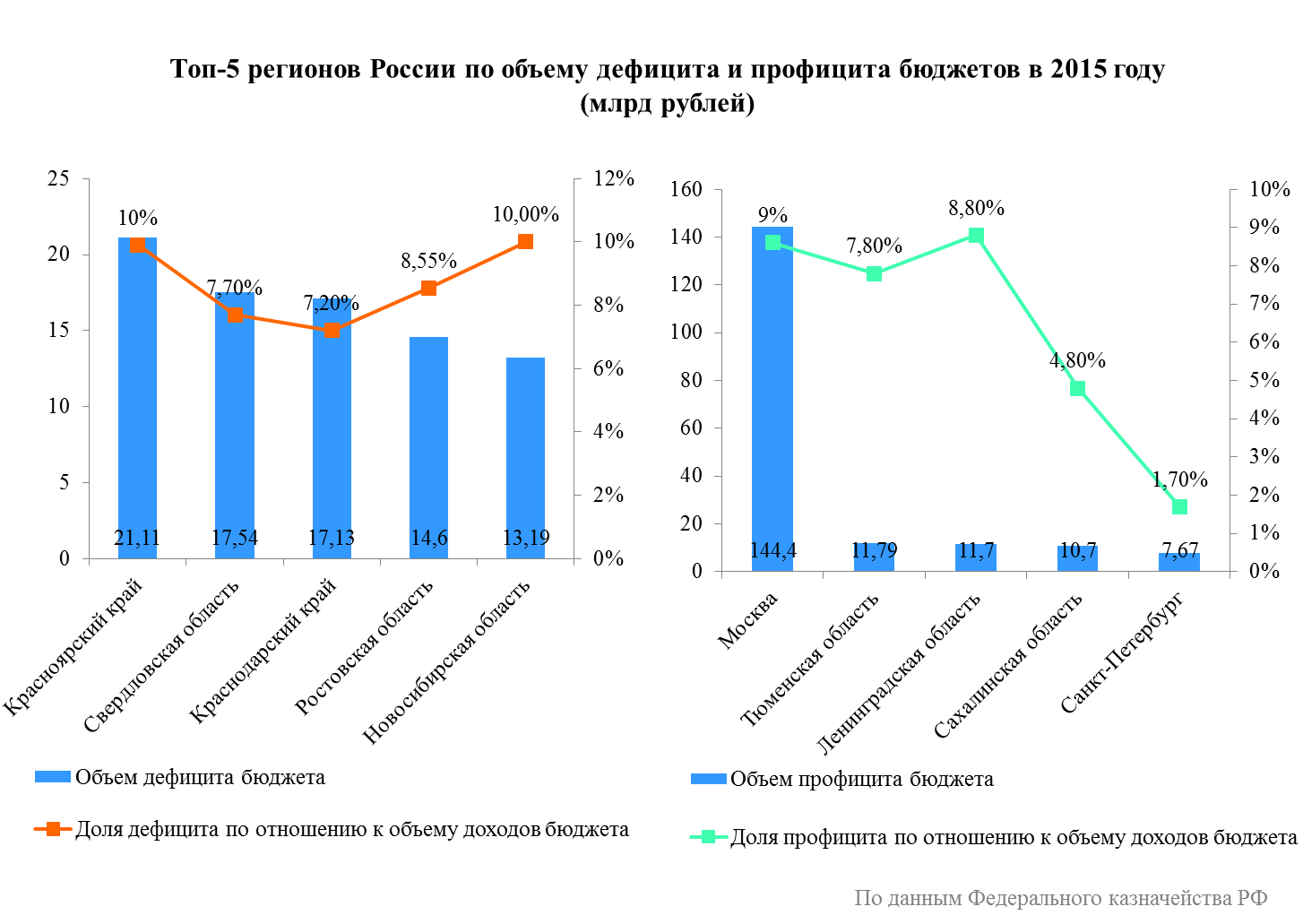

As a result, the budget deficit in the regions began to increase. So, for example, the worst situation is in the Siberian Federal District and Volga, where it reached 78.5 billion rubles and 84.38 billion rubles, respectively. The most significant deficit is typical for the Krasnodar Territory (17.13 billion rubles), Sverdlovsk Region (17.54 billion rubles), Krasnoyarsk Territory (21.11 billion rubles), Novosibirsk Region (13.19 billion rubles).

In many entities, budget deficits significantly exceed the critical level of 10% of revenue. So, for example, in the Magadan region it is 19.9%, the Republic of Mordovia - 23.2%, the Kaliningrad region - 18.8%.

At the same time, there are regions that ended this year with a plus - traditionally, these are financial and resource-producing centers: Moscow (+144 billion rubles), St. Petersburg (+7.6 billion rubles), Khanty-Mansi Autonomous Area (+ 7.2 billion rubles), Sakhalin Oblast (+ 10.7 billion rubles).

Not all regions have enough support from the center

Revenues from budgets of other levels account for more than a third of all regional budget revenues. However, in the last year there has been a trend towards a reduction in such assistance, and the allocated funds are distributed extremely unevenly. In 2015, a total of 1.683 trillion rubles was allocated to the budgets of the regions, which is less than in 2014 by 45 billion rubles. At the same time, only certain subjects felt full support. Thus, payments to Moscow doubled to 40.89 billion rubles, the Khanty-Mansi Autonomous Okrug - by 57% to 5.73 billion rubles, the Karachay-Cherkess Republic - by 22.5% to 2.72 billion rubles. At the same time, there were 52 regions that felt a decline in funding. Among them, the Nenets Autonomous Okrug (-80%), the Yamalo-Nenets Autonomous Okrug (-86%), the Republic of Crimea and Sevastopol (-39%) had the lowest rates.

The recession has affected many regions that survive mainly through government subsidies. For them, even a slight drop in such revenues can become critical - Smolensk and Tambov regions. In these regions, the share of gratuitous transfers is about 44%, while their volume fell by 5%. In the Altai Republic, where state subsidies account for 72% of budget revenues, the decline was about 15%. Things are slightly better for the Kaliningrad and Pskov regions - in their budgets, one-third come from gratuitous receipts, and the revenues themselves decreased by 4 and 13% over the year, respectively.

In general, the reduction affected mainly high-subsidized regions, but at the same time, revenues to entities increased, which in 2015 were characterized by a deeper economic crisis and a lack of budget funds - the Volga region, certain regions of Siberia and the Central Federal District.

Along with regional spending, debts are growing

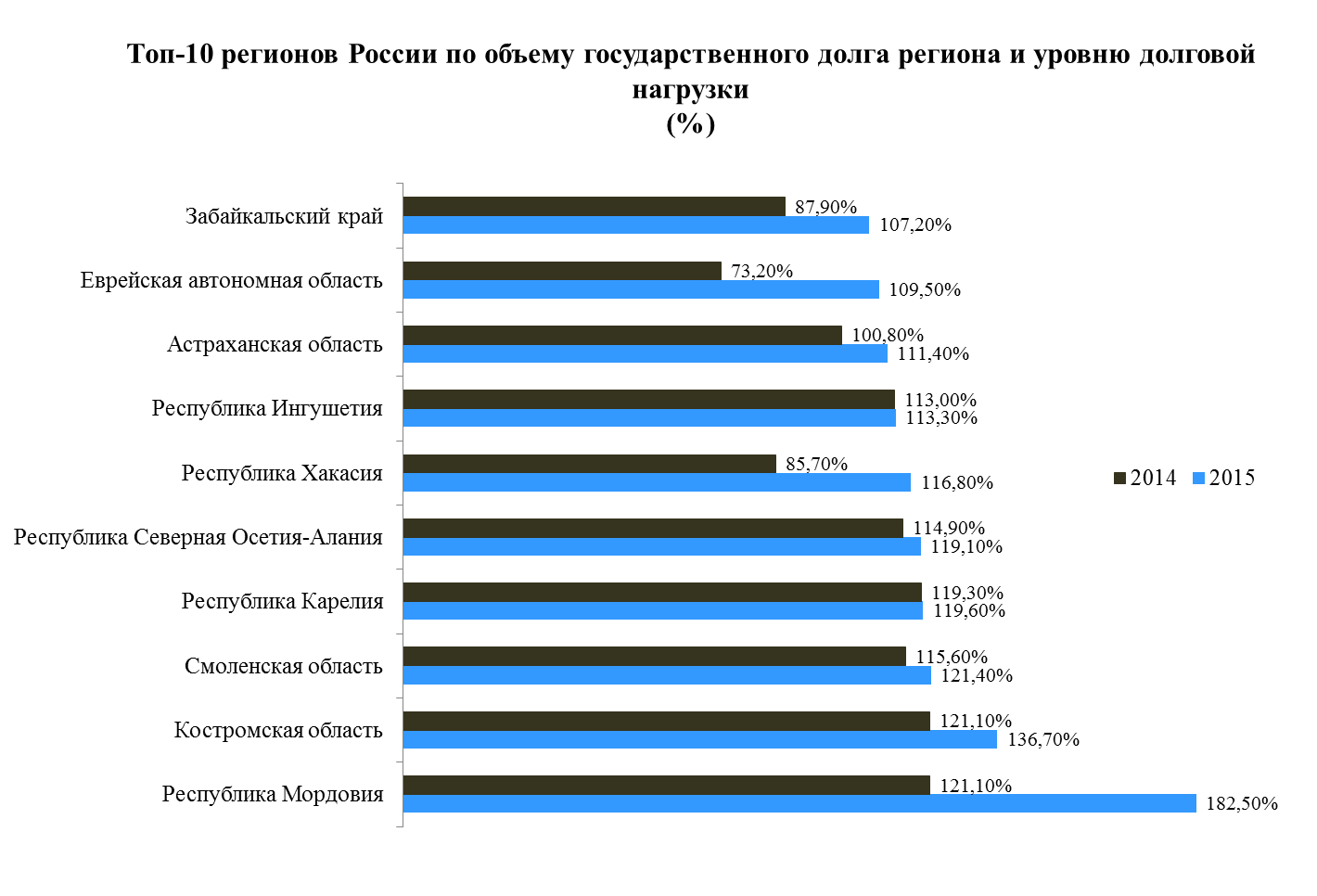

Experts note that even the money allocated by the state from the federal budget is still not enough. Gratuitous receipts - grants, subsidies are received in the region to cover current expenses - for major repairs, construction of infrastructure, social needs. However, every year the regions find it increasingly difficult to carry out existing tasks without attracting money from outside. As a result, many regions are gaining debt by attracting loans from the state and commercial banks. In 2015, the total debt burden of the regions, excluding debts of municipalities, increased by 229 billion rubles, exceeding the mark of 2.318 trillion rubles. In just a year, it increased by 10.96% - against the backdrop of the economic downturn, entities continued to borrow funds. At the same time, in 44 regions of the country, debt exceeded 70% of its own budget revenues, and in 14 regions all 100% of revenues. According to the results of 2015, the Republic of Mordovia became leaders in terms of the debt burden - the level of public debt exceeds the volume of budget revenues by 82.5%, Kostroma region (exceeding 36.7%), Smolensk region - by 21.4%.

Currently, the share of commercial loans is approximately equal to the amount of funds provided at interest to the state. However, even despite the fact that reducing the debt burden of the regions is one of the main tasks of state policy, according to estimates of the Accounts Chamber, it is not being implemented very effectively. In particular, to reduce the credit load, the Ministry of Finance has introduced a mechanism for issuing treasury loans to regions for up to two months, and also continues to refinance at lower interest rates commercial loans taken. At the same time, the agency does not forgive debts, and although these measures today help pay off creditors, this is only a temporary solution to the problem, which in the future will lead to an even greater increase in the burden on taxpayers. At the same time, according to estimates of the Accounts Chamber, already in 2017 the amount of debt will reach a critical level.

What did 2016 prepare for us?

According to experts, next year the load on regional budgets will increase even more. In addition to the expected increase in expenses due to inflation and the unfavorable economic situation, the authorities plan to reduce the amount of funds allocated to the budgets - both gratuitous receipts and treasury loans. For example, the regions will receive 310 billion rubles to repay commercial loans. 320 billion rubles were allocated for these purposes a year ago. The volume of inter-budget transfers is also planned to be reduced by the level of 2015 by 92.2 billion rubles to 1355.2 billion rubles.

In the meantime, the regions show not very optimistic indicators. Despite the fact that the draft budget for 2016 predicted an increase in budget revenues, for the first 2 months of 2016 the deficit already amounted to 201 billion rubles - 22% of the revenue. According to the forecasts of the Standard and Poors (S&P) international rating agency, the regions' debt to regions will also increase, reaching a record 1.7 trillion rubles, and the total debt of the regions will grow to 4.3 trillion rubles by the end of 2017. The costs of the constituent entities of the Federation will be reduced, but this is not possible in all areas. For example, many regions have already reduced spending on culture, education and health care, major repairs, but most of the entities left social spending at the level of last year ahead of the upcoming elections.

Word "budget" comes from the Old Norman bougette - wallet, bag, leather bag, bag of money. Currently, the term has lost its original meaning, since “budget” in the modern sense no longer means a piggy bank ”- a physical or bank account in which funds are stored. Today, the budget must be seen as a documented revenue and payment plan. So, for example, the state budget of the Republic of Sakha (Yakutia), annually adopted by the State Assembly (Il Tumen), in its simplest sense, is a list of sources of income (revenue), a list of directions for spending incoming funds (budget), and also expected annual values.

Types of budgets

The budget system includes:

- The federal budget and the budgets of state extra-budgetary funds of the Russian Federation (Pension Fund of the Russian Federation, Fund social insurance Russian Federation, Federal Compulsory Medical Insurance Fund);

- the budgets of the constituent entities of the Russian Federation and the budgets of territorial state extra-budgetary funds;

- local budgets, including:

- budgets of municipal districts;

- budgets of urban districts;

- budgets of urban and rural settlements.

A set of budgets of various levels forms a consolidated budget. So, for example, the compilation of the state budget and local budgets forms the consolidated budget of the Republic of Sakha (Yakutia). The code of the federal budget and the consolidated budgets of the constituent entities of the Russian Federation forms the consolidated budget of the Russian Federation.

Budget execution

The total budget does not mean that the indicated amount has been collected from taxes and other receipts and, as of the beginning of the year, is stored on any account, and is spent during the year. In fact, the receipt and expenditure of funds is “stretched” throughout the year and is carried out approximately uniformly. This process is called "Budget execution". Thus, they distinguish between budget execution by income (income over time from taxes and fees, gratuitous revenues to a single budget account) and budget execution by expenses (payments over time from a single budget account).

For example, a family budget consists of a parent's salary of 25,000 rubles per month, so the annual income of the family budget will be 600,000 rubles. With salary each parent once a month, budget revenues will be executed at 25,000 rubles. In addition to utility bills, annual budget expenditures will also include food, clothing, mobile phone and other expenses; budget expenditures will be implemented throughout the year every day, depending on needs.

Budget revenues

The remaining share of the state budget of the Republic of Sakha (Yakutia) is tax and non-tax revenues (usually referred to as “own revenues” 1).

In an enlarged grouping, tax and non-tax revenues can be represented as follows:

1. Tax revenues:

- income taxes and income taxes (corporate income tax, personal income tax);

- taxes on goods, work, services (excise taxes: on gasoline, alcohol, beer, tobacco, etc.);

- taxes on comprehensive income (tax levied in connection with the application of the simplified taxation system, single tax imputed income, single agricultural tax);

- property taxes (corporate property tax, transport tax, property tax of individuals);

- taxes, fees and regular payments for the use of natural resources (mineral extraction tax, fee for the use of wildlife, fee for the use of water biological resources);

- state duty (funds levied for committing legally significant actions: for state registration, issuing permits, etc.);

2. Non-tax revenues:

- income from the use of property owned by state and municipal property (income from the rental of state and municipal property, income from transferring part of the profit of state and municipal unitary enterprises, etc.);

- payments for the use of natural resources (payment for negative impact on the environment, payment for the use of forests, mineral resources, etc.);

- income from the sale of tangible and intangible assets (income from the privatization of state and municipal property);

- administrative fees and charges;

- fines, sanctions, damages;

- income from the provision of paid services (work) and compensation of state costs.

All sources of tax and non-tax revenue generation in accordance with the Budget Code of the Russian Federation are assigned to the corresponding budgets of the budget system of the Russian Federation.

Gratuitous income

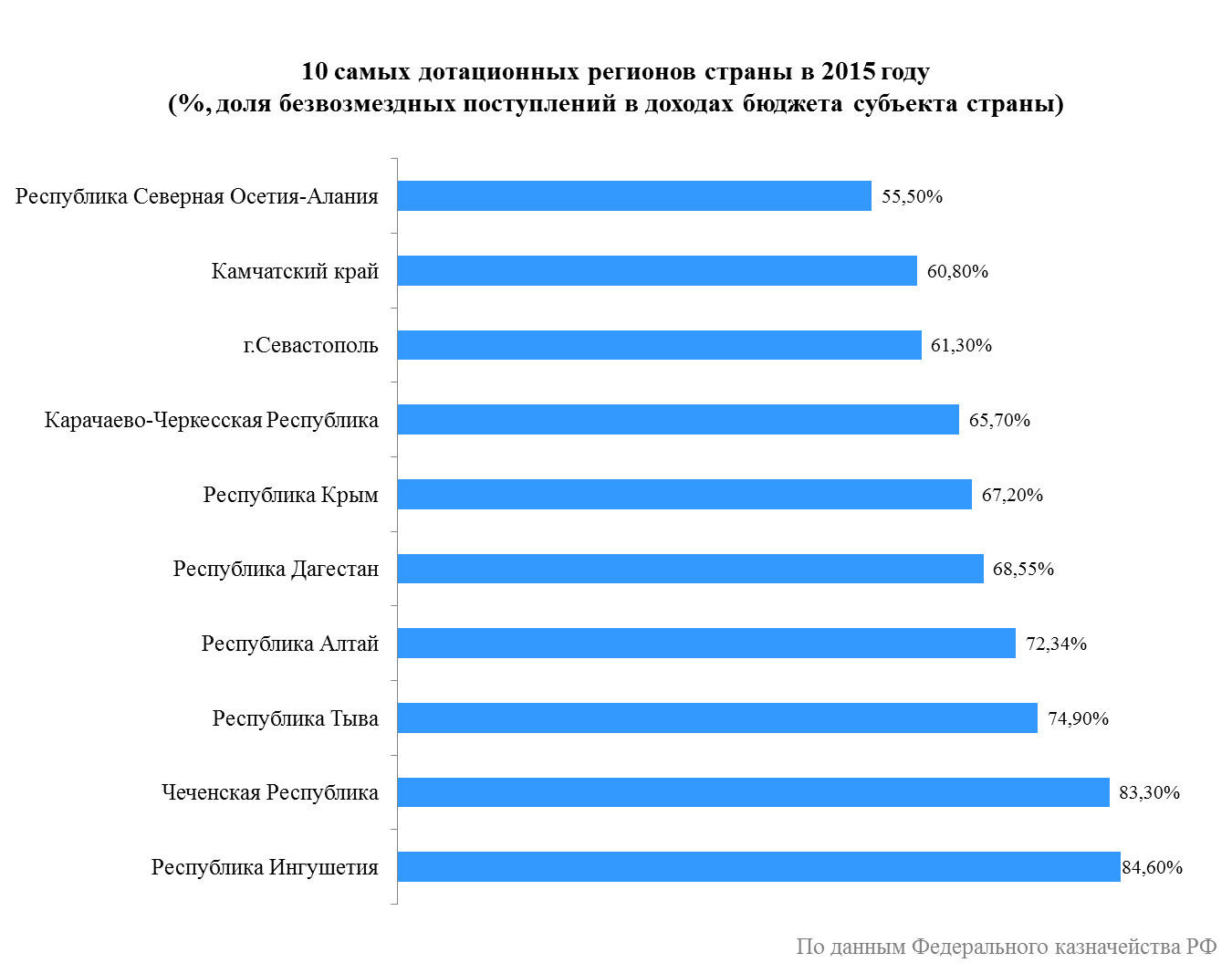

Gratuitous income to the budget - inter-budget transfers (funds) provided by one budget to another. Inter-budget transfers form a significant part of the budgets of all levels. Thus, the share of gratuitous revenues to the budget of the Republic of Sakha (Yakutia) is about 25% -30% of the total income. The minimum share of financial assistance in total revenue among the regions of the Russian Federation is the Yamalo-Nenets Autonomous Okrug (1.1% as of July 1, 2014), the maximum share is the Republic of Ingushetia (85.5%).

Intergovernmental transfers divided into subsidies, subsidies, subventions.

Subsidies are provided free of charge and irrevocable without establishing directions and (or) conditions for their use, i.e. sent to goals determined by the recipient on their own. Grants are commonly referred to as “non-targeted inter-budget transfers.”

Subsidies provided to support the exercise of authority, the performance of which is assigned to the recipient of subsidies. So, for example, the constituent entities of the Russian Federation are assigned powers to implement agricultural support programs. Targeted subsidies (subsidies to support livestock breeding, subsidies for the purchase of elite seeds and others) were provided to entities to support the exercise of these powers over the course of each year. Subsidies are usually provided on a co-financing basis - this means that the recipient of the subsidy must, at his own expense, provide for a certain proportion of financing (usually from 5% to 50%) for the same purposes.

Subventions granted to exercise the transferred powers, that is, powers that are not assigned to the recipient of the subvention. For example, the authority to register a civil registration is related to the authority of the Russian Federation and should normally be exercised by federal authorities. The specified powers were transferred for execution to the constituent entities of the Russian Federation. Subventions are provided to the regions to exercise these powers. The composition of the powers assigned to the subjects of the federation for permanent execution, or transferred to the subjects for execution along with subventions, periodically changes. So, since 2015, for the execution of the subjects of the federation, powers are transferred to provide social support measures for citizens exposed to radiation.

For example, a family, if a mother gives her son money for pocket expenses, which he spends at his discretion, this is a subsidy. If the son wants to buy a toy that costs 500 rubles, and he has only 200, then the mother adds 300 rubles to him to buy this toy and this is a subsidy. If a mother sends her son to the store for purchases and gives him money for them, then this is a subvention.

Surplus and budget deficit

If budget revenues exceed expenses, this means that the budget is formed with surplusif, on the contrary, expenses exceed revenues, then the budget in short supply. A budget deficit does not mean that any of the planned expenses will not be paid. All commitments made in the budget must be fulfilled, however, some expenses will not be paid for at the expense of income, but at the expense of sources of financing the budget deficit. These include: bank loans, budget loans (loans received from other budgets), budget account balances (unused funds from the previous year) and other sources. The very existence of a budget deficit also does not indicate problems in the financial system.

It is fundamentally important to have an understanding of sources of financing the budget deficit. Thus, the proceeds from the sale of shares or shares in the authorized capital owned by the state, in accordance with the Budget Code “by definition”, do not refer to budget revenues, but to sources of financing the deficit. Unused balances of last year’s budget funds, which are usually included in the budget after it statements (when specifying the budget) are also sources of financedeficit. Deficit financed bysuch sources are sometimes called "technical."

The size of the budget deficit is tightly limited by the Budget Code. Prethe effective size of the budget deficit of a subject of the Russian Federation cannotexceed 15% of total revenue excluding gratuitous receipts,deficit of local budgets - 10% of total revenue excluding carriagemeat revenues.

For example, a child is given 1000 rubles each month for pocket expenses. Throughout the year, the child accumulates this money on New Year plans to buy a phone for 15,000 rubles, of which 12,000 rubles come from "own" income for the whole year, so the deficit is 3,000 rubles, the sources of financing are the remaining budget funds in the amount of 1,000 rubles that the child left from last year, and an inter-budget transfer to buy a phone in the amount of 2000 rubles from the "federal" family budget from parents.

1 When interpreting the term "own income", caution must be exercised. In everyday use, “own revenues” is usually understood to mean tax and non-tax revenues (that is, budget revenues that are generated on the territory of a particular entity, rather than coming from the federal budget). At the same time, in accordance with the Budget Code, the concept of “own revenues”, in addition to tax and non-tax revenues, includes all gratuitous revenues with the exception of subventions (Article 47 of the Budget Code of the Russian Federation).

In the Russian Federation, as in the USSR and other states of the former socialist camp, in 1991-1995. receipts from the privatization of state property and the issue of credit money were noted. The latter took place during the period of socialism, but was of a hidden nature.

The specifics of the budget system of the Russian Federation implies a system of distribution of revenues between specific budgets - federal, constituent entities of the Federation and local, extrabudgetary funds. The federal budget revenues include:

Own tax revenues;

Own non-tax revenues;

Funds for mutual settlements from the budgets of the constituent entities of the Russian Federation, other gratuitous transfers;

Revenues of federal targeted budget funds;

Funds from federal social extrabudgetary funds.

General structure of federal budget revenues in 2005-2008 presented in table 2.1.

Table 2.1. - Dynamics of the structure of the federal budget of the Russian Federation, billion rubles

As can be seen from table 1.1, these revenues are the main; at the federal level, gratuitous transfers play virtually no role.

The structure of budget revenues of the constituent entities of the Russian Federation is developing somewhat differently. The revenues of the budgets of the Russian Federation are generated primarily from their own and regulatory tax revenues.

The general structure of the consolidated budget of the regions is shown in table. 2.2.

Table 2.2 - the structure of the revenues of the consolidated budget of the territories of the Russian Federation for 2008, billion rubles.

Note. Here, the data on the consolidated budget of the constituent entities of the Russian Federation are used from the source: Report on the execution of the consolidated budget of the territories, form code 0524108. - www.minfin.ru.

Analyzing the data, we can conclude that most of the budgets of the territories of the Federation are formed from tax revenues. Their share in the consolidated budget of the regions amounted to 57.5%, in the budgets of the constituent entities of the Russian Federation - 59.8%, and in local budgets - 53.6%.

But, a significant share of the revenues of the territorial budgets is represented by gratuitous transfers (13.2% of the budgets of the subjects) and domestic turnover (40, 1% of local budgets).

They play a particularly large role for local budgets, almost along with tax revenues (40.5% or 286.7 billion rubles).

Let us consider in more detail gratuitous transfers to local budgets using the example of the Alagir district in the next paragraph.