What is a selective tax benefit. Preferential taxation

Tax benefits - an advantage for taxpayers

Types and effectiveness of tax benefits, on tax benefits, benefits 2013

Tax breaks are the definition

Tax rebate - this an advantage that is provided by the state or local governments, a certain category of taxpayers. This is the advantage of a more favorable economic position in relation to other taxpayers. - one of the mechanisms of the state tax policyintroduced to solve problems in the social and economic spheres.

Tax rebate - thisthe advantage granted to certain categories of taxpayers and payers of fees provided for by the legislation on taxes and fees, compared with other taxpayers or payers of fees, including the possibility of not paying tax or pay them less.

Tax breaks arethe most important element of any taxhaving an exceptional character.

Tax benefits can be divided into the following groups: personal and for legal entities. individuals; general economic and social tax benefits; and foreign economic tax incentives aimed at stimulating exports, and general economic benefits. Any benefits have both negative consequences for of the state and positive for the people to whom it is provided. So for of the state this is a decrease in tax revenue, and for those to whom it is provided is an opportunity to improve their well-being. Usually, tax breaks are granted within the framework of government support for business, often during economic crises.

The purpose of tax benefits

The purpose of tax exemptions is to reduce the tax liability of a taxpaying obligation - deferment and installment payment, which, ultimately, indirectly also leads to a reduction in tax liabilities (deferment and commitments of payment can be considered as the actual presentation of a free or concessional loan). The main objective is to reduce the tax liability of taxpayments. liabilitiesthe second goal, which in practice is pursued relatively less frequently, is a delay or installment plan. of payment. However, the second goal should also be considered as a way to indirectly reduce tax liabilities, taxpaying obligations, only deferral or installment payment are actually loanprovided free of charge or on preferential terms.

Evaluation of the effectiveness of tax exemptions will be held in Finnish mines annually. Min Fin plans to develop a methodology for assessing the effectiveness of tax exemptions, taking into account, along with benefits the budget system of the Russian Federation the creation of favorable conditions for investment, as well as the results of the realization by the taxpayers of the benefits received. The assessment of the effectiveness of tax benefits is affected in the Main Directions of the tax politicians for 2013 and for planned 2014 and 2015 approved by the government RFTax agencies RossSredi among the main tax expenditures of budgets aimed at stimulating economic development, following the results of 2010, privileges are allocated in a number of areas. Among them are investment activity (354 billion rubles), innovation activity (12.2 billion rubles), industry development (252 billion rubles).

Tax benefits - this is

Tax breaks classification

Seizures - removal from taxation of individual items (objects) of taxation. In respect of taxes on profits and income exemptions are expressed in the fact that profit or the profit received by the payer from certain types of activity is removed from the structure of taxable income (income), that is, is not subject to taxation. For example, art. 251 NK incomenot taken into account when determining tax base". With regard to property taxes, exemptions are expressed in exemption from taxation of certain types of property. Example, and exemptions from taxation for certain categories of persons. For example, art. 333.35 NC RF “Benefits for certain categories of nat. individuals and organizations. " Exemptions from payment may be permanent or urgent (tax holidays).

Tax benefits - this is

Tax holidays (tax holiday) - exemption from payment income tax (or tax on part of the profit) for a certain periodThis incentive, as a rule, stimulates the development of new branches of production. clause 4.4 of the Instruction MNS №62 about income tax small enterprises and organizations businesses “tax holidays” for two years in tax payment are provided. But this privilege extended only to those small enterprises that were engaged in the production and at the same time processing of agricultural products, the production of food products, consumer goods, certain construction and repair and construction works, the production of building materials, food products, medical equipment, medicines and items. medical trade, if from these activities exceeded 70% of the total proceeds from sales of products (works, services).

Tax benefits - this is

Clause 4.5 of the said Instruction “tax holidays” for 5 years were provided businesses, received a loss in the previous year (with the exception of losses incurred on securities transactions), in terms of profits aimed at covering it, subject to the full use of reserve funds and other similarly designated funds for these purposes.

Tax price cuts - benefits aimed at reducing tax base. The payer has the right to reduce the taxable amount for the amount of costs on the goals encouraged by society and the state. For example, costs a taxpayer for an NGO for training on basic and additional professional educational programs, vocational training and retraining of taxpayer employees (clause 3 of Art. 264.1 of the Tax Code of the Russian Federation) or see sub. 38 p. 1 Art. 264

Tax benefits - this is

Release - concession aimed at reducing tax rate or salary tax amount (tax salary). Reducing the tax rate - for example, lowering the rate to 0% for large businesses that receive a profit in the form of dividends (subclause 1 of clause 3 of article 284 of the Tax Code of the Russian Federation). Reducing the tax wage is the most effective tax rebate, which directly reduces the amount (amount) of tax payable to c. See, for example, bonds of the Academy of the qualified zone in the United States (in fact, interest on the bond reduces the tax salary)

Tax benefits - this is

Deferral or installment payment of tax. Deferral or installment payment of tax is a form of change term tax payment established by law. The grounds, conditions and procedure for granting these benefits are regulated, see ch. 9 of the Tax Code. Here it is worth noting that some researchers distinguish the difference between deferral and installments. So, Bryzgalin considers deferment as a postponement of the deadline for paying the full amount of tax to a later date, and installments as the distribution of the amount of tax on certain parts with the establishment of deadlines for the payment of these parts. loan, as well as the deferral (or installment plan) of tax payment, is a form of changing the deadline for tax payment. There are differences, for example, in the procedures for granting these benefits: deferrals or installments are provided by a decision of the authorized body, and for granting a tax loan is. Tax credits are charged. interest, as well as for the provision of a delay or installment plan. See ch. 9 of the Tax Code, in which we are talking about the investment tax credit.

Tax benefits - this is

Return of previously paid tax (part of tax) or tax amnesty (not to be confused with the release of the taxpayer from financial sanctions) - for example, subparagraph 2 of paragraph 2 of Art. 151 provides that when exporting goods outside the customs territory of Russia in the customs mode of re-export, the amount of tax paid when importing into the customs territory of Russia is returned to the taxpayer in the order Payment of previously paid tax. This type of release is widely used to avoid double taxation (the so-called loan for foreign taxes) - see, for example, Art. 232 of the Tax Code of the Russian Federation (elimination of double taxation)

Total number of tax breaks in Russia

Tax systems in different countries are quite diverse, but the main thing that unites them, and in this respect taxation system Russian Federation corresponds to the systems of developed countries - this is an exception to the taxation of capital, operating in production, and export. The total number of tax incentives that we use when taxing profits is large enough. However, the bulk of tax exemptions by lawshould not reduce the actual amount of tax deducted without benefits, more than 50%. In developed countries, the number of benefits is much higher than in the Russian Federation. So in USA there are more than 100 of them, in England and Germany, up to 70-80.

Under the condition of their full and correct application, as experts note, it works normally organization with an average level of profitability, it may not at all show profit in its balance sheet and, thus, become fully exempted from taxes. For this reason, traditional systems income taxes have long been subjected to sharp criticism. An attempt to eliminate some of the disadvantages of levying income tax is introduced in Western Europe, and in 1992 and in the Russian Federation, the value-added tax (VAT). The number of benefits for this tax compared to income tax is limited. VAT has the advantage that businessmen’s wages are included in its base, which serves as an incentive for them to improve labor efficiency and use modern technology.

Tax benefits - this is

Exemption from this tax for export operations is actually the payment of large subsidies to domestic business. Immediate write-off of the cost of acquiring assets for organizations serves as a greater incentive to update production than the establishment of income tax incentives. Benefits are provided for payment land tax(local), property tax organizations, on the payment of VAT, for services in the field of culture, benefits for benefactors, benefits for participants in hostilities in Afghanistan, for small and medium businesses and others.

Tax benefits - this is

There are many problems in the field of the establishment and operation of benefits related to improving the effectiveness of this tool of state support. With the help of taxes, it is indeed capable of creating more or less favorable and competitive conditions for business areas. But at the same time there is a suppression of other spheres. Therefore, the state of the socio-economic value of some industries is unacceptable, because otherwise the freedom of competition and the principle of justice are inevitably violated. Consequently, the policy of granting preferences should facilitate the implementation of priorities established by the state in an objective manner (meaning there are clear criteria for granting tax exemptions that minimize the influence of special interest groups).

Example of preferential legislation for land tax

Tax RF secures tax benefits in various industries management, so, chapter 31, is devoted to the land tax, and article 395, characterizes, provided in this question, tax privileges.

Exempt from tax: 1) of the company and institutions of the penitentiary system of the Ministry of Justice of Russia in relation to land plots allocated for the direct fulfillment of the functions entrusted to these firms and institutions; 2) companies in relation to land plots occupied by state public roads; 3) religious firms in relation to the land plots belonging to them, on which buildings, buildings and structures for religious and charitable purposes are located; 4) All-Russian public companies of disabled people (in including those created as unions of public organizations of persons with disabilities), among whose members disabled persons and their legal representatives constitute at least 80 percent, in respect of land used by them for the implementation of statutory activities;

Firms whose charter consists entirely of contributions from these all-Russian public organizations of persons with disabilities, if the average number of persons with disabilities among their employees is at least 50 percent, and their share in the wage fund is at least 25 percent, in respect of the land plots used by them for production and (or) the sale of goods (with the exception of excisable goods, mineral raw materials and other minerals, as well as other goods according to the list approved by the Government of Russia in coordination with the Russian Federation Kimi public organizations of persons with disabilities) of works and services (except for broker and other intermediary services);

institutions whose sole owners of property are the specified all-Russian public companies of disabled people - in respect of land plots used by them to achieve educational, cultural, health and fitness, physical education, sports, scientific, informational and other goals of social protection and rehabilitation of disabled people, as well as providing legal and other assistance to persons with disabilities, disabled children and their parents; 5) companies of folk arts and crafts - in respect of land plots located in places of existence of folk arts and crafts used for the production and sale items of trade folk arts and crafts;

Tax benefits - this is

6) individualsbelonging to the indigenous peoples of the North, Siberia and the Far East of Russia, as well as the communities of such peoples in relation to the land used for the preservation and development of their traditional way of life, economic management and crafts; 7) lost its force. - Federal law dated November 29, 2004 N 141-ФЗ; 8) resident companies of a special economic zone, with the exception of the organizations referred to in paragraph 11 of this article, in respect of land plots located in the special economic zone for a period of five years from the month when the right arose ownership of each land plot;

Tax benefits - this is

9) companies recognized by management companies in accordance with the Federal Law "On the Innovation Center Skolkovo" - in respect of land plots that are part of the territory of the Innovation Center Skolkovo and provided (acquired) to directly perform the functions assigned to these firms in accordance with with the Federal Law; 10) shipbuilding companies with the status resident industrial production special economic zone, - in respect of land plots occupied by the property owned by them and used for the construction and repair of ships by buildings, structures, industrial facilities, from the date of registration of such organizations as resident special economic zone for a period of ten years.

Tax benefits - this is

Tax Credit - Tax Relief

The most difficult element in the system of tax benefits is tax loan. Article 65 of the Tax Code of the Russian Federation determines the procedure and conditions for granting a tax loan, as well as the timing and availability of grounds. The grounds for granting a tax loan are provided for by the norms of Article 64 (paragraphs 1 - 3, paragraph 2). However, the tax loan in the tax codex The Russian Federation is generally cut off from tax exemptions and is unilaterally defined as a change in the period for which the tax obligation is fulfilled for a period of three months to one year with a phased payment by the taxpayer of the loan amount, and the delay (installment plan) of the tax payment is detached from the general liabilities of the tax loan.

Tax benefits - this is

Investment tax loan is the most promising form of tax regulation. This is an independent type of targeted tax loan, associated exclusively with the promotion of investment and innovation activities of enterprises. The concept, procedure and conditions for granting an investment tax loan are governed by Art.66 and Art. 67 of the Tax Code of the Russian Federation. Investment tax loan is such a change in the tax payment term, in which the company, if there are grounds, is given the opportunity, within a certain period and within certain limits, to reduce its tax payments with subsequent stage-by-stage payment of the loan amount and accrued interest.

Tax benefits - this is

Special tax regimes

Tax by code Russia introduced a new concept of “special tax regimes” (Article 18 of the Tax Code of the Russian Federation). A special tax regime is recognized as a special procedure for calculating and paying taxes and fees for a certain period of time, applied in cases and in accordance with the procedure established by legislation on taxes and fees. Special tax regimes include the simplified taxation system for small businesses, the tax system in free economic zones system of taxation in closed administrative-territorial entities, the system of taxation in the performance of the contract of agreement and product sharing announcements.

Tax benefits - this is

These regimes may not impose more stringent taxation conditions due to agreementsit should be noted that special tax regimes are based on the need for legal regulation of the activities of economic entities in certain territories of Russia. One of the mechanisms to stimulate economic development, tax debt, expansion tax base and income growth should be a restructuring of tax arrears. In a broad sense, restructuring is one of the ways to resolve the problem of non-payment in budget system and creating prerequisites for improving the economic situation.

Tax benefits - this is

In a more narrow, specific, understanding - this is a postponement of the payment of tax payments and the freezing of financial sanctions for a certain time period, that is, the transfer of enterprises' obligations to the budget from current to long-term ones. The restructuring started in 1999 was delayed, and this is due, primarily, to the insufficient development of the mechanism for the commitment of payables to federal budgetIn general, the tax benefits of an individual or group nature should be focused primarily on producers (industries, types of production), ensuring the production of products competitive on the world market that can give an economic and fiscal effect.

Changes in tax incentives 2013

From January 1, 2013 is not taxed movable property regardless of the type of activity of the organization. Law of November 29, 2012 N 202-FZ amended chapter 30 of the Tax Code “property tax”. If you purchased the property in December 2012, and put it into operation after January 1, 2013, then in this case, you can take advantage of the property tax rebate this year. For example, if you bought a car on December 20 and put it into operation on January 9, we no longer pay property tax on it. Also in case

Plan

4.1. The concept of tax benefits

4.2. Tax rebate system

4.3. Types and forms of tax benefits

4.4 Legal regulation of territorial tax benefits

4.1 Despite the fact that tax benefits are related to additional elements of the tax, this problem is one of the most debatable. The main purpose of benefits is to reduce the tax pressure on the payer. The benefit can be realized by reducing the object, the base, the amount of tax, deferment of tax liability. Through the mechanism of benefits taxes carry out regulatory and incentive functions, creating the interest of taxpayers.

The exemption is the exemption (full or partial) of the taxpayer, taking into account its features, from paying the tax. Here it is necessary to emphasize three circumstances.

Firstly, a privilege is an exemption from payment, and not from a tax obligation, since when the obligation is deferred, the tax payment remains, and the exemption (for a certain period) only applies to tax recalculation, and upon expiration of a certain period, the obligation is subject to sale (tax credit ). In addition, the tax liability includes several components: tax accounting; tax payment; tax returns. And if the taxpayer can be exempt from paying tax, then he will have the responsibility for accounting and reporting.

Secondly, the exemption is possible in two volumes: full - when the taxpayer is fully exempted from payment, and partial - when the tax pressure is reduced by reducing the object (object, etc.) or deferring the payment of tax.

Thus, the tax benefit is recognized as the exemption of the taxpayer from the accrual and payment of tax or the payment of tax in a smaller amount if there are grounds specified by the legislation of Ukraine.

Exemption from tax is possible in full or in part.

When fully exempted, the taxpayer is fully exempt from tax accrual and payment.

In case of partial exemption, the taxpayer is exempted from paying tax only in a certain part of his tax liability. The grounds for granting tax exemptions are the features that characterize a certain group of taxpayers; type of their activity and object of taxation.

When describing a tax, it is necessary to pay attention to the regulation of tax benefits. Moreover, this provision should contain not a complete (which is hardly possible for the long term), but a rather wide list of exceptions, which would then be specified, with the inclusion of a detailed application mechanism in specific regulations relating to certain types of taxes. The system of privileges and privileges is a peculiar reference point for legal and individuals when choosing areas of activity, forms of income.

It is important to take into account that benefits are an alternative to subsidies, personal grants and separate leverage of tax credits. That is why a systematic approach is needed here, linking these levers in one complex. Analysis and their regulation should be carried out in close relationship, as if complementing each other.

The legal regulation of tax benefits is carried out on two levels.

The first one is tax laws, which fix principle exceptions for certain categories of payers or industries.

The second is bylaws that accomplish tactical goals in relation to specific subjects and solve narrower goals.

Controversial is the issue of sectoral benefits.

Often created a number of benefits:

in the field of budgetary regulation (through subsidized payments, etc.);

tax exemptions;

allocation of tax credits.

The taxpayer has the right to use tax relief from the moment of the occurrence of the relevant grounds for its use and during the whole period of its validity independently, without prior notification of the tax authorities.

4.2. The system of tax incentives must be divided into two groups.

Firstincludes relatively traditional and stable tax exemptions, regardless of changing circumstances and even government.

The secondthe group of benefits is characterized by a certain short duration in relation to specific objects

The characteristic of tax benefits should be based on equality in the field of taxation, and when granting benefits, the criterion should be the financial situation of the taxable subject. The grounds for granting privileges are hardly legitimate if they are not related to property status. Classification of tax benefits can be carried out according to various principles.

More often tax rebate determined by:

1) tax deduction, reducing the tax base when calculating the tax;

2) reduction of tax liability after tax accrual;

3) establishing a reduced tax rate.

1. Deduction (withdrawal) - the type of tax benefits, in which the separation of individual components from common object taxation in order to reduce the value of their object in the calculation and payment of tax.

This type of benefit is characterized by the fact that the mechanism of granting benefits is projected on the taxable object, which is directly reduced. Similar object reductions for taxation purposes can be classified:

but) by types of payers:

full - provided to all payers;

partial - provided to certain categories of payers;

b) on time:

permanent - acting continuously for a long period of time;

temporary - valid for a certain, pre-limited period (enterprises with foreign investments);

emergency - are provided in connection with the appearance of certain sudden circumstances;

at) by object elements:

property - the deduction of a certain part of the taxable property;

profitable deductions - are applied to the part of the income of the payer., depending on the type of activity.

2. A discount - type of tax breaks, reducing the amount of tax on certain values. The totality of these values, which form the basis of the discount, is determined by the amount of expenses of the payer, which the legislator derives from taxation by reducing the equivalent amount of the tax base. Thus, the public interest in a certain activity of the payer is realized, its expenses are stimulated in a certain direction.

Here you can apply the classification of deductions (exemptions) in the field of taxation (by type of payer; by date; by elements of the tax base):

a) limited discounts, the size of which is limited directly or indirectly;

b) non-limited - discounts at which the tax base can be reduced by the full amount of the taxpayer's expenses.

Personal discounts entitle the payer to exclude from taxable income expenditures aimed at personal arrangement. In Canada, such costs include savings for the purchase of your own home. In the US, a taxpayer can replace personal deductions with a standard discount of 10% of the amount of taxable income, but not more than $ 1,000 per couple. In this case, family discounts depend on the composition of the family. The basis is the regulatory function of taxes, and such discounts are of particular importance for low-income segments of the population. Thus, the Algerian Direct Tax Code (Art. 96) determines the amount of tax reduction of 1,200 dinars for the first child and for each following child 800 dinars, provided that the total amount of these reductions does not exceed 3,600 dinars.

3. Tax credit - type of tax benefit, in which the exemption relates to the total amount of tax payment accrued for payment. Such a formulation of this benefit is to some extent conditional, since the “tax credit” is on a kind of border between the concept of “lending” and “financing”. So, if an ordinary tax credit implements the basic principles of lending (urgency, payment, repayment, target character), then the investment tax credit is implemented on the principles of financing.

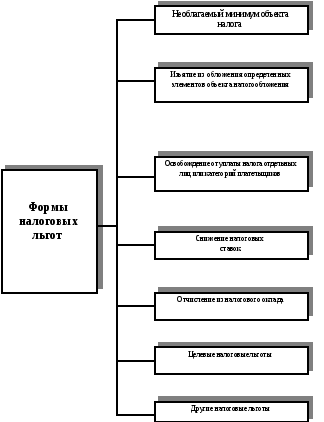

Tax exemptions are exceptions from the general accrual scheme of a specific type of tax, are enshrined in the regulatory act and take into account the features that characterize the payer, the object, the rate or other conditions. In this case, the benefits are often full or partial tax exemption. The set of benefits that claims to be fixed in the main law governing the tax system may contain the following forms:

1. Free object tax minimum.To bind to the absolute value of the monetary amount in terms of inflation does not make sense. That is why the legislator allocates a multiple of the minimum wage, which is approved by the Verkhovna Rada of Ukraine and automatically increases when the minimum wage changes.

2. Withdrawal from taxation of certain elements of the objecttaxation.Most often it is a part of income or other objects of tax that is directed to goals in the implementation of which the state or local self-government bodies are interested: environmental protection measures, development of new technologies.

3. Exemption from the tax of individuals or categoriespayers.Thus, the legislator opens up great opportunities for real income while reducing tax exemptions, since quite often funds for the maintenance of these subjects are allocated from the budget, and this channel somewhat simplifies the movement of funds from taxpayers to the budget, and then in the opposite direction, to the people they are are required. A sufficiently developed system of benefits of a similar type is provided for by the Law of Ukraine “On the status of war veterans, guarantees of their social protection”, which entered into force on January 1, 1994 (paragraph 18 of article 12; paragraph 23 of article 13; paragraph 17 of article 14; Clause 19 of Article 15 of the Law). According to them, the most protected in this regard is the category of war invalids, who are fully exempted from paying taxes, fees and customs duties of all kinds.

4. Tax cuts.This type of benefits reflects both the state and regional significance of the type of activity subject to a reduced rate.

5. Deduction from the tax salary.It primarily provides for exemption from the tax salary, which is carried out for a certain settlement period.

6. Targeted tax breaks. May include various forms of deferred tax collection. As a most typical example, one can single out a mechanism for using a tax credit.

7. Other tax breaks (tax holidays, etc.).

4.3. If we consider tax privileges as a definite exemption of taxpayers (and this is exactly how the Russian legislator, Article 56 of the Tax Code of the Russian Federation, is suitable), then it seems reasonable to single out certain territories in which preferential tax treatment is established.

Such territories can exist on two levels:

1) lowest level -territories characterized by exemptions from the use of local taxes and fees. Thus, in accordance with Art. 15 of the Law of Ukraine "On the tax system" local governments at their own discretion may establish part of local taxes and fees and due to this form a more favorable tax regime in the respective territories;

2) highest level -territories of special zones characterized by specific preferential taxation, regulated by special legislation.

At the same time, such territories are divided into two subspecies:

a) territories providing preferential tax treatment for tax residents of Ukraine and located outside the territory of Ukraine (these include primarily offshore zones);

b) territories located in Ukraine and providing preferential tax treatment for tax residents and non-residents of Ukraine (free economic zones).

For individuals with high incomes, one of the ways to reduce taxation is to change the status and lawfully reduce the tax. For legal entities - reducing tax pressure outside the territory of their own state.

To carry out activities on the territory of Ukraine or Russia, registration (acceptance) is required in tax authorities. In this case, you must provide a document confirming the registration of the company in the country of its permanent location; legalized extracts from the trade register or statutory legalized documents; a document confirming the solvency of the company (certificate from the bank about opening a company account abroad); order for the chairman of the representative office. All the above documents must be translated into the state language and notarized.

The system of offshore zones received certain legislative support in 2000. On February 21, 2000, the President of Ukraine, by order No. 90/2000 / RP, instructed the Cabinet of Ministers of Ukraine to determine and publish the list of offshore zones and to ensure its annual publication in the future. The main reason that pushed to consolidate this list was paragraph 18 of the Law of Ukraine “On taxation of enterprises' profits”, which regulates the procedure for working with taxpayers who trade with firms registered in offshore zones. Namely: when transferring money to such firms for purchases, it is allowed to charge only 85% of the actual value of the goods. The remaining 15% is from net profit. For non-compliance with this standard, high penalties are provided. There is no concept of offshore zones. Therefore, the legislator went along a somewhat simplified path - consolidate an exhaustive list of offshore zones, and not explain what their nature is.

Thus, on March 1, 2000, the Cabinet of Ministers approved their list, which included: British island regions: Gibraltar, Alderney, Guernsey, Jersey, Man. Middle East: Bahrain, Damascus. Central and South America: Belize, Costa Rica, Panama. Europe: Andorra, Ireland, Campione, Cyprus, Liechtenstein, Madeira, Malta, Monaco, Montenegro. Caribbean regions: Anguilla, Antigua, Antilles, Aruba, Bahamas, Barbados, Virgin Islands, Grand Cayman, Grenada, Bermuda, Nevis, Gyurks and Caicors Islands, Turke Islands and Caicos Islands. Africa: Liberia, Mauritius, Seychelles. Pacific region: Vanuatu, Hong Kong, Western Samoa, Labuan, Marshall Islands, Nauru, Niue, Cook Islands, Singapore.

In general, all free economic zones are divided into two categories:

1) transit transport - zones located along the perimeter of the borders of Ukraine, ensuring the attraction of goods to the territory of Ukraine and the flow of transit goods through the territory of Ukraine. They are created in order to simplify the procedure for moving these goods;

2) industrial- Zones located on the territory of Ukraine, enshrined in legislation, in which the investment is made and in which preferential tax treatment is established. Such a preferential treatment applies mainly to preferences for import VAT, customs duty, income tax, contributions to the employment fund and the State Innovation Fund. The system of free economic zones in Ukraine is relatively developed, but not all created zones are already fully operational.

The basis of territorial tax benefits is the principle of tax sovereignty of the state, on the basis of which the national tax system is formed, which differs from others in its specific approaches. Along with a large number of other features (registration conditions, regulation of currency relations), taxation mechanisms play a major role.

There are two groups of countries that are considered as tax havens.

1. Developing countries. They pursue a policy of attracting foreign capital and set low rates for foreign entities (Antilles, Hong Kong), or completely abolish the taxation of imported capital (Bahamas, Bermuda). This group of countries does not have tax agreements with other countries, which ensures the confidentiality of financial information, the absence of legal obligations to pay tax in their country of residence.

2. Countries that provide relative tax benefits in relation to certain types of income, due to the specifics of domestic tax legislation and tax agreements (Luxembourg, Switzerland, etc.) "

The preferential tax treatment in certain regions of the country should stimulate entrepreneurial activity and attract investment in the national economy.

Structural logic modules

Scheme 4.1.- Types of tax benefits

Scheme 4.2.-Forms of tax benefits

Questions and tests on the topic

Give a definition of tax benefits.

Specify the levels of legal regulation of tax benefits.

Ways to determine the tax benefits.

Classification of deductions (withdrawals) by types of payers, by dates, by object elements.

Types of tax benefits.

List the forms of tax benefits.

Describe the levels at which the preferential tax regime is established.

Give a classification of free economic zones.

The taxpayer’s exemption from tax accrual and payment (or tax payment in a smaller amount if there are grounds specified by the legislation of Ukraine is:

a) discount;

b) deduction;

c) tax relief;

d) tax credit.

The type of tax relief in the field of taxation, in which the separate components are separated from the common taxable object in order to reduce the value of their object when calculating and paying the tax:

a) tax credit;

b) discount;

c) deduction;

d) tax benefit.

Benefit type, reducing the amount of tax on certain values:

a) tax credit;

b) discount;

c) deduction.

A type of exemption where the exemption relates to the total amount of tax payment accrued for payment:

a) tax credit;

b) discount;

c) deduction.

By type of payer deductions (withdrawals) are classified:

a) complete;

b) partial;

c) medium;

d) temporary.

The timing of deductions (exemptions) are classified:

a) temporary;

b) complete;

c) permanent;

d) emergency;

According to the elements of the object of deduction (withdrawal) are classified:

a) property;

b) real;

c) profitable;

d) non-profitable.

Free economic zones are divided into:

a) transport;

b) transport and transit;

c) industrial;

|

№ tasks |

possible answer |

All tax benefits have one common goal - reducing the amount of tax liability of the taxpayer. Less often, another goal is pursued - deferral or installment payment, which ultimately (given that deferral or installment payment is in fact a loan provided free of charge or on preferential terms) also indirectly leads to a reduction in the tax obligations of the taxpayer.

However, the mechanism of its action tax benefits have significant differences.

Depending on the change in which element of the tax structure - the object (object) of taxation, the tax base or the salary amount is used, the benefit can be divided into three groups:

Seizures;

Liberation (Scheme 1-16).

Withdrawals are a tax rebate aimed at removing individual items (objects) of taxation from taxation.

With regard to taxes on profits and income exemptions are expressed in the fact that the profit or income received by the payer from certain types of activities is removed from the structure of taxable income (income), i.e. not taxable.

The law on corporate income tax provides for a significant number of exemptions. For example, profits from the production of baby food, from the production of technical means for the prevention of disability and the rehabilitation of disabled people, etc., are not subject to taxation.

Withdrawals are provided for and the Law of income tax from individuals. So, in order to give competitiveness to government loans, winnings and amounts received in their repayment are not included in the total taxable income, i.e. not taxable.

With regard to property taxes, exemptions are expressed in exemption from taxation of certain types of property.

Indirect taxes also use this type of benefits.

According to Art. 5 of the Law of the Russian Federation "On Value Added Tax", for example, insurance and reinsurance operations, banking operations, with the exception of collection operations, etc., are exempt from taxation.

Withdrawals may be permanent or granted for a limited period.

For example, the Law on the Profit Tax of Enterprises and Organizations provides for exemption from taxation of profits derived from newly created production (with the exception of industries created in the framework of trade, supply and marketing, and intermediary activities of organizations) for a period of its payback, but not more than three years. (Clause 6, Article 6).

Withdrawals may be granted to all tax payers, as well as their separate category.

In accordance with Art. 4 of the Law of the Russian Federation "On tax on property transferred in the order of inheritance or donation" tax is not charged on the cost of residential buildings and vehicles, passing in order of inheritance to disabled people of groups 1 and II.

Discounts are privileges that are aimed at reducing the tax base.

In respect of taxes on profits and income discounts are not associated with income, but with the costs of the taxpayer. In other words, the payer has the right to reduce the income subject to taxation by the amount of expenses incurred by him on goals encouraged by society and the state: transfers to charitable foundations, educational, health care, cultural institutions, costs of environmental protection measures, etc.

Depending on the impact on the results of taxation, discounts can be divided into limited (the amount of discounts is limited directly or indirectly) and unlimited (the tax base can be reduced by the full amount of the taxpayer's expenses).

As well as exemptions, depending on the absence or presence of restrictions on the subjects, the benefits of this group can be general, which are used by taxpayers regardless of subjective signs, and special, the use of which is allowed only to certain categories of subjects.

Under the exemptions understand the benefits aimed at reducing the tax rate or salary amount. The salary amount (gross tax) is the result of multiplying the number of units of taxation included in the tax base by the tax rate (s). In taxes, the amount of which is determined by the layout between the taxpayers of the total amount to be received (folding taxes), the salary amount exists as a predetermined amount.

Exemptions are a direct reduction of the tax liability of the taxpayer. Benefit here is provided directly in contrast to the benefits provided by withdrawals and discounts, which reduce the salary amount indirectly. Exemptions more than other types of benefits are able to take into account the property status of the taxpayer.

If the benefits of the first two types receive the greater benefit to the payer, whose incomes are taxed at a high rate, the same quantitative exemption retains a larger share of income to the payer with low incomes.

For example, one taxpayer has an annual income of 50 thousand rubles, and another - 100 thousand rubles. Both are entitled to discounts in the amount of 5 thousand rubles. If progressive taxation of these income fall into different tax categories, the benefit is more effective for the second taxpayer. So, if the income is up to 50 thousand rubles. are taxed at the rate of 10%, and in excess of this amount - at the rate of 20%, the first taxpayer would pay without allowance for the benefit of 5 thousand rubles. (50 thousand rubles. X 10%), and the second - 15 thousand rubles. (50 thousand rubles x 10% 50 thousand rubles x 20%). If taxpayers apply a benefit, then the first will pay a tax of 4.5 thousand rubles. [(50 thousand rubles. - - 5 thousand rubles.) X 10%], and the second - 14 thousand rubles. . It is easy to see that the quantitatively equal privilege saves the first payer 0.5 thousand rubles, and the second - 1 thousand rubles.

If taxpayers are granted tax exemption in the same amount, then the first taxpayer will not receive a tax liability at all (50 thousand rubles x 10% - 5 thousand rubles = 0 rubles), and the second will have to pay 10 thousand . rub. [(50 thousand rubles x 10% 50 thousand rubles x 20%) - - 5 thousand rubles = 10 thousand rubles.]. In this case, the first payer saves 10% of their income, and the second only 5%.

Exemptions from tax payment can be divided into types according to the forms of granting benefits.

Reduced tax rate. For example, according to the Law on the Profit Tax of Enterprises and Organizations, the tax rate is reduced by 50% for enterprises whose staff includes 50% and more are pensioners and people with disabilities.

Reducing the salary amount (gross tax). The salary can be reduced in part or in full, for a certain time or indefinitely.

Full exemption from tax for a certain period was called the tax holidays.

Exemption from tax should not be confused with the addition of arrears, i.e. writing off bad debts on taxes and fees, which is carried out in exceptional situations of an economic, social or legal nature, which made it impossible to recover the tax (Article 59 of the first part of the Tax Code of the Russian Federation).

Deferral or installment payment of tax. Deferral or installment payment of tax is a form of changing the deadline for tax payment, established by law. The grounds, conditions and procedure for granting these benefits are regulated by Art. 61-64.68 parts of the first Tax Code of the Russian Federation.

Tax credit. Tax credit, as well as deferral or installment payment tax - form changes in the tax payment term. The differences are that the maximum period of deferral or installments in accordance with the Tax Code of the Russian Federation is six months, and a loan can be granted for up to one year. There are differences in the procedures for granting these benefits: deferrals or installments are provided by the decision of the authorized body, and for granting tax credit is a contract. For using a tax credit interest is charged, as well as for granting a deferment or installment plan. However, if the need to obtain benefits is caused by causing damage to a person as a result of a natural disaster, a technological catastrophe or other force majeure circumstances or a delay in budget financing, payment of a state order, then interest is not charged.

The grounds, conditions and procedure for granting a tax credit are set out in Art. 65.68 parts of the first tax code of the Russian Federation.

Investment tax credit. This privilege consists in providing organizations that invest in research and development, production re-equipment, the creation of new technologies, as well as performing particularly important orders for the socio-economic development of regions, the right to reduce their tax payments with subsequent stage-by-stage payment. of these amounts and accrued interest.

If the maximum tax credit period is one year, then an investment tax credit is granted for a period of one to five years. The investment tax credit agreement defines the type of tax, the loan amount, the contract validity period, the interest rate, the repayment procedure, measures to ensure the fulfillment of the contract terms (pledge, surety), the liability of the parties.

Target tax credit. Target tax credit is the replacement of the payment of tax (part of the tax) in monetary terms with natural execution. Instead of depositing a monetary amount in the budget, the taxpayer delivers its products in favor of budget organizations or institutions, provides them with services, and works.

The provision of such benefits was provided for by the Law of the Russian Federation No. 2071-1 of December 20, 1991 “On Investment Tax Credit” (Art. 11-14). According to the Law, the privilege was granted to the taxpayer by local authorities within the limits of the amount of tax credited to local budgets if he fulfills a particularly important order for the socio-economic development of the territory or the provision of especially important services to the population of this territory.

If the payer wanted such a benefit, he entered into a tax agreement with the local administration. This agreement was subsequently subject to approval by the local authority when considering the relevant budget.

In the event of an enterprise violating a tax agreement, the entire amount due for payment to the budget in the absence of such an agreement, as well as 25% of this amount in the form of a fine, was levied from it to the appropriate local budget. The decision was taken by the administration that entered into the agreement. The decision could be appealed by the enterprise in court.

Such natural taxation is characteristic of the crisis stages of economic development, accompanied by a decrease in solvency, an increase in the mutual indebtedness of market participants and the state, etc.

The tax code of the Russian Federation establishes that taxes can be paid only in cash - cash or non-cash (Art. 58 of the first part of the Tax Code of the Russian Federation). The possibility of providing a targeted tax credit Code is not provided.

Return of previously paid tax (part of the tax). This type of exemption also has the name of a tax amnesty (the term “tax amnesty” is also used in connection with the release of the taxpayer from financial sanctions).

An example of a tax amnesty is a concession provided for by the mean. "A" n. 1 art. 5 of the Law of the Russian Federation "On Value Added Tax": when exporting goods purchased with a value added tax from the territory of the Russian Federation, the amount of tax is returned to exporting enterprises.

Offset previously paid tax. This type of exemption is widely used to avoid double taxation (the so-called loan for foreign taxes). The amount of income tax paid by a Russian enterprise abroad in accordance with the laws of other countries is counted when paying tax in the Russian Federation. At the same time, the amount of the credited amount may not exceed the amount of income tax payable in the Russian Federation on the profit received abroad.

Sometimes in the payment of one tax can be counted another.

In accordance with paragraph 4 of Art. 5 of the Law of the Russian Federation "On tax on property transferred in the order of inheritance or donation" the amount of the calculated tax on property transferred into the ownership of citizens in the order of inheritance, in the presence of residential buildings (apartments), cottages and garden houses * in this property gardening partnerships, reduced by the amount of property tax of individuals, payable by these persons for the specified objects.

Send your good work in the knowledge base is simple. Use the form below.

Students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

Federal Education Agency

State educational institution of higher vocational education

Test

under tax law

theme:« Preferential taxation»

Plan

Introduction

2. Provision of benefits

Conclusion

Literature

Introduction

In the Russian legal system, tax legal relations acquired constitutional status only in 1993, i.e. after the adoption by universal suffrage of the new Constitution of the Russian Federation. The imposition of a constitutional nature on tax relations reflected not only the needs of law enforcement practice, but also the level of development of legal thought and the legal culture of Russian society. The norms of the Constitution of the Russian Federation not only enshrined the universal obligation to pay legally established taxes and fees (article 57), but also provided for a system of legal guarantees that ensure a compromise between respecting the rights of taxpayers and the fiscal interests of the state.

Paragraph 2 of Art. 56 of the RF Tax Code stipulates that tax benefits are a right, and not an obligation of taxpayers. This means that in some cases the taxpayer has the right to refuse to use tax exemptions on a legal basis, as well as to suspend their use for one or several tax periods. Tax privileges can be established only by the legislation on taxes and fees, therefore the norms of other “non-tax laws”, which provide any tax advantages to individual subjects, have no legal force and are not applicable.

1. Benefits

Privileges for taxes and fees are recognized for certain categories of taxpayers and payers of fees provided by the legislation on taxes and fees benefits compared with other taxpayers or payers of fees, including the possibility not to pay tax or levy or pay them in a smaller amount.

Tax benefits have the following characteristics:

a) they represent the advantages of certain categories of taxpayers, in particular:

lower tax rate;

postponement of taxes and fees;

other frequency of fulfillment of the obligation to pay taxes and fees;

the right to exercise various tax deductionsreducing the taxable base;

the right to accelerated depreciation of fixed assets or the inclusion in the cost of goods (works, services), costs, which are usually not included in it, etc .;

b) the advantages mentioned above can be expressed in complete exemption from taxes and fees. At the same time, there are cases when such a privilege is granted both for one and all types of taxes and fees;

c) they can be provided only in the case when it is provided for in the regulatory legal acts on taxes and fees. In other words, privileges on taxes and fees, the provision of which is quite often provided for in other acts of current legislation, including some federal laws, can be used by payers only to the extent that the corresponding amendments and additions are made specifically to acts of legislation on taxes and fees;

d) they are provided to certain categories of taxpayers (for example, small business entities, individuals with disabilities of the Great Patriotic War, Heroes of the Soviet Union, etc.). Tax exemption cannot be individualized, i.e. they cannot be provided to a specific organization, a specific individual;

e) the norms of the legislation on taxes and fees themselves cannot be individual if they define:

the grounds for applying benefits (circumstances that allow the taxpayer to provide benefits on taxes and fees);

the procedure for granting privileges (the procedure for granting the taxpayer the mentioned privileges, registration, determining the circle of tax authorities and their officials who are entitled to provide taxpayer benefits to the taxpayer, etc.);

conditions for the application of tax and levies privileges (i.e., the obligation to comply with the taxpayer, who has been granted tax and levies benefits, certain requirements or the performance of certain actions as necessary prerequisites for the actual use of benefits).

Paragraph 2 of Art. 56 of the Tax Code contains very important rules for the practical implementation of benefits on taxes and fees. At the same time, it is necessary to pay attention to the fact that any benefits on taxes and fees are meant here and the taxpayer is entitled to:

Or to completely abandon the use of benefits on taxes and fees;

Or suspend the use of tax and levies for one or several tax periods. Unlike a complete refusal, this means that at the end of the tax period (during which the privilege was not applied) the payer has the right to use this privilege (for the next period). However, he is obliged to notify in writing tax authority about refusal (suspension) to use the privilege. If disputes arise as to whether the taxpayer refused to use the privilege, it should be assumed that the fact that the taxpayer does not take into account the tax benefit when drawing up a declaration for a specific tax period does not in itself mean that he will refuse to use the corresponding tax benefit in this period;

The rules of paragraph 2 of Art. 56 of the Tax Code have a general character: they are used, unless otherwise provided in the code.

Federal Law No. 95 of July 29, 2004 Art. 56 of the Tax Code is supplemented with paragraph 3. Its rules provide that the benefits:

By federal taxes set exclusively by yourself Tax Code;

By regional taxes - can be established (canceled) along with the Tax Code also by the laws of the constituent entities of the Russian Federation;

For local taxes, they are established (canceled) along with the Tax Code, as well as the regulatory legal acts of municipalities (and in Moscow and St. Petersburg - the laws of these entities);

The rules of paragraph 3 of Art. 56 also assume that the privileges provided for by the laws of the constituent entities of the Russian Federation (acts of representative bodies of local self-government) are in addition to the privileges established by the norms of the NK itself.

2. Provision of benefits

Organizations and individual entrepreneurs are exempted from VAT if, during the three previous consecutive tax periods, the amount of revenue from the sale of goods of these organizations or individual entrepreneurs did not exceed 1 million rubles. The specified exemption from tax payment does not apply to tax duties arising from the importation of goods into the customs territory of the Russian Federation.

The exemption of organizations and individual entrepreneurs from VAT is made for a period of twelve consecutive tax periods. Upon expiration of the specified period, the exemption from tax liability may be extended on the basis of a written application of the taxpayer and relevant documents.

Provision by a lessor for rent in the territory of the Russian Federation of premises to foreign citizens or organizations accredited in the Russian Federation is not subject to taxation. This benefit applies in cases where the legislation of the relevant foreign state establishes a similar procedure for citizens of the Russian Federation and russian organizationsaccredited in this foreign country.

A special legal regime for exemption from excise taxation is established with respect to operations for the sale of excisable goods outside the Russian Federation. Exemptions from taxation of transactions placed under the export customs regime are carried out only if the taxpayer complies with a number of statutory conditions. First, the export of goods outside Russia must be carried out directly by their manufacturer or owner. Secondly, exemption from excise tax payment is possible only when a guarantee is submitted to the tax authority by an authorized bank. At the same time, the form and content of the guarantee are subject to special requirements in the form of the bank's obligation to pay the full amount of the excise tax and the corresponding penalty in case the taxpayer fails to submit documents evidencing the export of excisable goods.

The taxpayer has the right to make, in some cases, a reduction in the total amount of excise tax paid, i.e. implement tax deductions. Tax deductions are applied for imported excisable goods into the territory of the Russian Federation released for free circulation and subsequently used as raw materials for the production of excisable goods. The amount of tax for the transfer of excisable goods made from customer-supplied raw materials is reduced. There are tax deductions if the buyer returns paid excisable goods or if they are refused. Regarding alcohol products, advance payments paid by the taxpayer when acquiring excise stamps or special regional stamps. It also reduces the amount of excise tax charged on ethyl alcohol made from food raw materials and used for the production of alcoholic beverages.

As for taxes on personal incomes, here legislation establishes standard, social, property and professional tax deductions - amounts of money in a fixed amount, deducted from the tax base of certain categories of taxpayers.

Standard tax deductions are applied on a monthly basis for any particular group of taxpayers. Standard deductions include:

3 thousand rubles from the monthly income - the persons who received or had radiation sickness as a result of the Chernobyl NPP; participated in the testing of nuclear weapons, carrying out and ensuring the work on the collection and disposal of radioactive substances; invalids of the Great Patriotic War; persons with disabilities, contusions, injuries or injuries while defending the Fatherland, as well as other categories of citizens.

500 rubles a month - Heroes of the Soviet Union and Heroes of the Russian Federation, persons who have suffered the blockade of Leningrad; prisoners of concentration camps; persons with disabilities since childhood, as well as persons with disabilities I and II groups; citizens who performed international duty in the Republic of Afghanistan and other countries in which military operations were conducted.

300 rubles a month - to taxpayers who are supported by a child under the age of 18 or a full-time student under the age of 24.

Social tax deductions are used to reduce the tax base of individuals in the event they carry out certain socially significant actions. This type of deduction includes amounts: income transferred by the taxpayer to charitable purposes; paid by the taxpayer for their training; spent on treatment in a medical institution or for the purchase of medicines.

Property tax deductions include amounts received by the taxpayer from the sale of their own residential houses, apartments, cottages, garden houses or land plots, as well as amounts spent by the taxpayer for new construction or the acquisition in Russia of a dwelling house or apartment or directed to repay interest on mortgage loans.

Professional tax deductions are expenses associated with a particular taxpayer activity. The following are entitled to receive this deduction: citizens-entrepreneurs carrying out business activity without education legal entity; private notaries and other private practitioners; taxpayers who receive income from the performance of work (provision of services) under civil law contracts, as well as persons who receive royalties or remuneration for the creation, publication, execution or other use of a work of science, literature and art.

Benefits on a single social tax are divided into general, i.e. applicable to all taxpayers, and on individual, i.e. applied to certain categories of taxpayers. As a general rule, any organization is exempted from the payment of this tax with the amount of income not exceeding 100 thousand rubles accrued during calendar year disabled workers. With the amount of income not exceeding 100 thousand rubles, public organizations of persons with disabilities do not pay tax; organizations whose authorized capital consists entirely of contributions from public organizations of persons with disabilities; institutions whose property is owned by public organizations of persons with disabilities and which are created to achieve educational, cultural, health and medical, scientific and other social goals, as well as to provide legal and other assistance to the disabled person and their parents.

Foreign citizens and stateless persons who carry out entrepreneurial activities on the territory of Russia are exempted from the payment of a unified social tax, provided that they are not entitled to state pension, social security and medical assistance at the expense of state funds of the Russian Federation.

A feature of the legal regime of tax on property of organizations is the presence of a large number of benefits under Art. 381 of the Tax Code of the Russian Federation. So, they are exempted from taxation: organizations and institutions of the penitentiary system of the Ministry of Justice of the Russian Federation; religious organizations; All-Russian public organizations of persons with disabilities; organizations whose main activity is the production of pharmaceutical products. The following are not included in the number of objects of property tax: historical and cultural monuments of federal significance, social and cultural objects used for the needs of culture and art, education, physical culture and sports, health care and social security; the property of specialized prosthetic and orthopedic enterprises, bar associations, law offices and legal advicestate research centers, etc.

For local taxes, the legislative authorities of the constituent entities of the Russian Federation have the right to establish land tax benefits, but only within the amount of tax credited to the regional budget. Provide privileges on land tax have the right and local governments, but also within the limits credited from this tax to the municipal budget. Regarding tax exemptions for this tax, federal legislation establishes that local governments provide privileges in the form of partial exemption for a certain period, postponement of payment, or lowering the tax rate.

Under the tax on property of individuals, federal legislation provides for a wide list of benefits. So, Heroes of the Soviet Union and Russia are fully exempt from paying the tax in question; persons awarded the Order of Glory of three degrees; participants of the Civil and Great Patriotic Wars, as well as persons equated to them; disabled people of I and II groups; persons who received benefits in accordance with the Law of the Russian Federation of May 15, 1991 "On the social protection of citizens exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant", and others.

Pensioners, soldiers, sailors, sergeants, foremen, warrant officers for the period of active military service are exempt from paying tax on buildings, premises and facilities.

Citizens who have motor boats with a motor with a power not exceeding 10 hp are exempt from paying vehicle tax.

In addition to the benefits defined by federal law, representative (legislative) bodies state authority subjects of the Russian Federation and local governments (except for local governments of cities of regional subordination) have the right to reduce the size of rates and to establish additional benefits for this tax. The tax competence of local governments in the cities of district subordination, villages and settlements has a truncated amount, since the law establishes a limit on the provision of tax benefits for individuals' property taxation. The representative bodies of these municipalities may provide tax benefits only to individual payers.

Conclusion

For quite a long time, tax concessions were established not only by laws entirely devoted to this or that tax, but also by other legislative acts that are not related to taxation at all, and often the procedure for applying concessions was not prescribed. This was done by the tax authorities, issuing a huge number of instructions, recommendations and letters.

The legislation on taxes and fees consists of the Tax Code and laws on taxes and fees adopted in accordance with it (Article 1 of the Tax Code of the Russian Federation).

At the same time, Article 56 of the Tax Code of the Russian Federation states that tax privileges, that is, certain advantages of certain taxpayers, can be stated only in the legislation on taxes and fees. That is why the tax authorities penalize those organizations that use the benefits contained in non-tax laws. However, their position is wrong, and here's why.

According to article 76 of the Constitution of the Russian Federation, all federal laws on the territory of Russia have a direct effect. They are obliged to comply with state authorities, officials, citizens and organizations (Article 15 of the Constitution of the Russian Federation).

The norms of non-tax laws, establishing benefits for organizations, regulate tax legal relations, that is, in essence, they are norms of legislation on taxes and fees. The fact that they are contained in non-tax laws is undoubtedly a mistake of the legislator. After all, these benefits were introduced at a time when the tax system was just being formed.

But the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 5 of February 28, 2001 states that before the relevant chapters of Part Two of the Tax Code of the Russian Federation come into force, the courts must apply the rules concerning tax incentives, and this does not depend on which law they are included.

Now there are more than a hundred non-tax laws that establish the right of certain organizations to preferential taxation terms. However, in most cases, the payer is sent to tax lawwhich supposedly should regulate the procedure for granting this or that benefit. However, there is no such order, which means that it is impossible to use benefits.

On the other hand, there are laws in which it is clearly defined that it is possible not to pay VAT or income tax, while observing certain conditions. Such benefits you are entitled to apply. And if the tax authorities try to hold you accountable, then any arbitration court will recognize that they are wrong.

Literature

1. Tax Code of the Russian Federation. - M .: Publishing house Eksmo, 2004 - 592 p.

2. Resolution of the Plenum of the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation “On some issues related to the introduction of part one of the Tax Code of the Russian Federation” of 11 June 1999 No. 41/9 // “ Russian newspaper"Dated July 6, 1999

3. Guev A.N. Article-by-article commentary to the Tax Code of the Russian Federation: Part One: Sections I-VII: Chapters 1-20. - M .: Publishing house "Exam", 2005.

4. Petrova G.V. Tax law. Textbook for universities. - 2nd ed., Stereotype. - M .: Publishing house NORMA (Publishing group NORMA - INFRA H M), 2000. - 271 p.

Similar documents

The basic concept and functions of tax benefits and preferential taxation in the Russian Federation. The procedure and conditions for granting preferential taxation. The problem and the effectiveness of the use of special tax regimes on the example of LLC "Arizona".

term paper, added 03/19/2015

Tax breaks as a tool for tax incentives to modernize the economy. Their essence and groups: (investment, business support and development, social; exemptions, discounts and loans). Inventory of benefits for regional and local taxes.

term paper added on 12/05/2014

Concept, classification, types of tax benefits. Theoretical and practical bases of application of privileges in the tax system of the Russian Federation. Disadvantages of the system of tax benefits in the Russian Federation and ways to reform it. Problems of applying VAT exemption. The procedure for calculating benefits.

term paper, added 02.12.2010

The concept of tax breaks and deductions. Assessing the tax burden and its impact on the welfare of taxpayers. Investment benefits as a way to stimulate economic activity. The system of investment tax incentives in foreign countries.

thesis, added 04/19/2015

Concept, classification and types of tax benefits. Significance of benefits for tax system RF. The mechanism of application of tax incentives for organizations and their impact on the economic development of the country. Evaluation of the effectiveness of investment tax benefits.

term paper added on 01/15/2015

Inventory of tax benefits aimed at supporting investments provided for by federal and regional legislation. Identification of benefits that will be most in demand in order to modernize production and support investment organizations.

thesis, added 09.03.2015

The procedure and conditions for granting tax benefits. Their role in stimulating small business. The mechanism of application of tax incentives for organizations and their impact on the economic development of the country. The main directions of their rational use.

term paper, added 02/26/2010

Analysis of the theoretical aspects of taxation on a single agricultural tax. The study of the tax base, rates, benefits and objects of taxation. Financial and economic characteristics of LLC "PZ Borgoysky". The composition and structure of assets of the enterprise.

term paper added on 10/27/2013

Organization of work of tax inspections. Functions and duties of tax authorities. Tax control powers, types and forms tax audits. Accounting for taxes and fees and debt. Powers to collect taxes, penalties and fines.

term paper added on 09/18/2010

Differentiation of spheres of domestic and international taxation. Types and forms of international tax agreements. Application of offshore taxation mechanisms. Consideration of the main types of benefits provided to offshore non-resident companies.

What are tax breaks? Privileges for taxes and fees are recognized advantages of some taxpayers compared with others. They are provided by law. Basically this is an opportunity not to pay tax or pay it in a smaller amount.

Privileges for federal taxes and fees are established and canceled by the Tax Code.

Privileges on regional taxes are established by the Tax Code and (or) laws of the subjects of the Russian Federation on taxes.

Privileges for local taxes are established by the Tax Code and (or) regulatory legal acts of the representative bodies of municipalities.

Who is exempt from payment transport tax? Individuals - Heroes of the Soviet Union, Heroes of the Russian Federation, holders of the Order of Glory, disabled people and legal representatives of disabled children. The privilege is granted for one unit. vehicle.

Land tax rebate. Representatives of indigenous minorities of the North, Siberia and the Far East are exempted from its payment. This is provided by the Tax Code of the Russian Federation.

In addition, the Resolution of the City Assembly of Deputies of Yakutsk dated October 25, 2005 of CBC N 37-5 “On Approval of the Regulation on the Establishment of Land Tax Rates, the Procedure and Deadlines for the Payment of Land Tax in the Territory of the Yakutsk City Municipality” is in force. for the following categories of the population:

- Families with four or more minor children;

- owners, landowners, land users of sites located in the flooded area. They are recognized as assigned to the flooded area by order of the mayor of Yakutsk. These orders are accepted annually;

- honorary citizens of Yakutsk - in respect of one plot;

- veterans of the Great Patriotic War, as well as citizens, on whom social guarantees and privileges of the participants of the Great Patriotic War are extended by law;

- invalids of 1 and 2 groups;

- citizens exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant and other radiation accidents at nuclear facilities for civilian and military purposes, as well as as a result of tests, exercises and other work related to any type of nuclear facilities, including nuclear weapons and space technology;

- Heroes of the Soviet Union, Heroes of the Russian Federation, Heroes of Socialist Labor and full holders of the Orders of Glory, Labor Glory and "For serving the Motherland in the Armed Forces of the USSR";

- veterans of hostilities - in the amount of 50 percent.

All benefits are provided for land used for purposes not related to business activities.

Tax on property of individuals. Exempt from its payment:

- Heroes of the USSR and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of three degrees;

- disabled people of I and II groups, disabled since childhood;

- participants in civil and World War II, other military operations for the defense of the USSR from among military personnel serving in military units, headquarters and institutions that were part of the active army, and former partisans;

- Persons of civilian personnel of SA, Navy, VD and state security bodies, who occupied full-time positions in military units, headquarters and institutions that were part of the active army during the Great Patriotic War, or persons who were in cities during this period, and whose participation in the defense counts as a service for granting pensions on preferential terms established for servicemen of units of the active army;

- citizens exposed to radiation due to the disaster at the Chernobyl nuclear power plant;

- citizens who have become disabled, have received or suffered radiation sickness and other diseases as a result of the accident in 1957 at the Mayak Production Association and the dumping of radioactive waste into the Techa River;

- military personnel, as well as citizens dismissed from military service upon reaching the age limit of being in military service, health condition or in connection with organizational and staff activities, having a total duration of military service of 20 years or more;

- persons who were directly involved in the composition of units of special risk in the testing of nuclear and thermonuclear weapons, the elimination of accidents of nuclear installations on weapons and military facilities;

- family members of servicemen who lost their breadwinner;

- pensioners receiving pensions appointed in accordance with the procedure established by the pension legislation of the Russian Federation;

- Citizens dismissed from military service or called for military training, performing international duty in Afghanistan and other countries in which hostilities were fought .;

- Parents and spouses of military personnel and civil servants who died while on duty;

- cultural workers, artists and craftsmen from specially equipped buildings, buildings, premises (including housing), owned by them and used exclusively as creative workshops, studios, studios, as well as from the living space used for organizing open to the public non-state museums, galleries, libraries and other cultural organizations - for the period of their use;

- Citizens from located in areas in horticultural and dacha non-profit associations of residential buildings with a living area of up to 50 square meters and household buildings and structures with a total area of up to 50 square meters.

Taxpayers who are eligible for benefits, independently submit a statement and supporting documents to the tax authorities. Residents of Yakutsk need to contact the city tax inspection to the address: 202 md., 23 building, operating room, window N 33.

Sometimes taxpayers apply for the provision of benefits for the payment of transport, land taxes, property tax individuals out of time. In this case, the tax authority recalculates the amount of taxes in no more than three years at the written request of the taxpayer.