The procedure for calculating the income of un based on. Advance payments for unpu

- What incomes are taxed under the general system?

- Tax deductions

- Form 3 NDFL and its completion

- Form 4 PIT

If a businessman carries out his activities in the general taxation system, he should know the specifics of calculating personal income tax for individual entrepreneurs in the ESS.

If a Russian citizen is going to become an individual entrepreneur, he needs to decide in advance what tax system he will use. Much depends on what type of business activity is planned as a business. For some types of work and services it is allowed to use such convenient and profitable tax regimes as UTII, patent and simplified payment. However, they have one undeniable drawback, namely, restrictions on the type of activity, the number of employees and the amount of annual revenue. If the PI does not fall into the category of permissible, there is nothing left for him except how to use the ESS, that is, the general tax regime.

Moreover, it is this system that is installed by default in cases where the entrepreneur has not indicated the desired mode during registration. If a businessman loses his right to use a patent or other convenient system during a tax period, the individual entrepreneur is automatically transferred to the general tax system of personal income tax.

Most entrepreneurs do not like this tax system. And there are many reasons for this. The first of them can be called a very complex reporting to the regulatory authorities and a large number of various taxes, which must not only be paid on time, but also correctly calculated. Otherwise, you can get an impressive fine. However, some entrepreneurs simply have no choice, so you have to use all the pluses and minuses of the ESS.

Most entrepreneurs do not like this tax system. And there are many reasons for this. The first of them can be called a very complex reporting to the regulatory authorities and a large number of various taxes, which must not only be paid on time, but also correctly calculated. Otherwise, you can get an impressive fine. However, some entrepreneurs simply have no choice, so you have to use all the pluses and minuses of the ESS.

All the rules regarding the payment of personal income tax of IP on the OSNO are reflected in the Russian tax legislation, namely, in 23 and 227 Art. Often the most problems arise with taxes on the income of individuals, that is, with the calculation and payment of personal income tax.

What incomes are taxed under the general system?

The base value, which is taken when calculating the NDFL IP on the ESS, is any profit derived from doing business. When calculating the need to take into account a specific tax period. In the amount of income, you must include the proceeds from the sold goods, as well as mandatory means, which were identified as surplus during the inventory. The latter, in any case, without exception, must be registered, that is, credited.

Revenues are recorded for the day when they were actually received by the entrepreneur. This also applies to cash receipts, payment in kind, and receipts to the account of an individual entrepreneur or trustee. Many entrepreneurs do not know how to deal with advances. If the buyer has made a prepayment, it must be fixed on the day of receipt, as this money should be part of the base for calculating the tax.

The entrepreneur should be aware of the need to make the most accurate information in the accounting logs. For those who use the OSNO, this is especially important, since any miscalculations can result in serious trouble, including heavy fines.

Back to table of contents

Tax deductions

Despite the fact that most individual businessmen do not like the general tax regime, it still has certain advantages. We are talking about tax deductions that can significantly reduce the tax base and, consequently, save a lot of money to the entrepreneur. Types of tax deductions are divided into 4 groups, namely: standard, social, property and professional. The first 3 are calculated in the same way as this process occurs with individuals working for hire. There is nothing complicated in this, and everything is done according to a standard scheme known to every accountant.

Despite the fact that most individual businessmen do not like the general tax regime, it still has certain advantages. We are talking about tax deductions that can significantly reduce the tax base and, consequently, save a lot of money to the entrepreneur. Types of tax deductions are divided into 4 groups, namely: standard, social, property and professional. The first 3 are calculated in the same way as this process occurs with individuals working for hire. There is nothing complicated in this, and everything is done according to a standard scheme known to every accountant.

As for the professional deduction, this item is the actual expenses incurred by an individual entrepreneur in a certain tax period. Information about them must be documented. The rules on tax deductions for individual businessmen are governed by Russian tax legislation, namely, 252 Art.

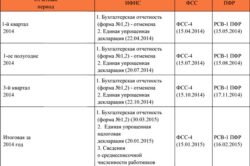

Regardless of whether the entrepreneur has employees or not, he is obliged to submit 2 types of reports to the regulatory authorities, it is a question of the third and fourth personal income tax forms.

There is also a second form, but it is necessary only for those entrepreneurs who work with the involvement of hired employees. This document should reflect the information regarding the wages of employees and other persons who received payments without income tax from a particular UI.

Back to table of contents

Form 3 NDFL and its completion

This document is a declaration in which taxes on income of individuals will be prescribed. This should fully reflect the tax base for a specific period. In this case, we are talking not only about the profit that was received by the businessman from his commercial activities, but also about the expenses of the individual entrepreneur for the income tax on personal income tax

This document is a declaration in which taxes on income of individuals will be prescribed. This should fully reflect the tax base for a specific period. In this case, we are talking not only about the profit that was received by the businessman from his commercial activities, but also about the expenses of the individual entrepreneur for the income tax on personal income tax

The entrepreneur should remember that this document is very important, therefore, it is necessary to treat it as responsibly as possible. It is also necessary to calculate everything correctly in order to fill in the form with correct data on income. It is necessary to submit the document once per reporting period, that is, per year. Terms of delivery are limited. 3 NDFL must be filed with the tax inspectorate no later than May 1 of the year following the reporting year.

As for how to calculate the personal income tax for the IP on the OSNO, it can be done according to the data from the account book, where all profits received in the reporting period and subject to taxation should be recorded. Further, all tax deductions are taken into account. An exception are not professional. The resulting difference will be the tax base from which the individual businessman is obliged to pay the sum of money to the state treasury. By law, the interest rate on personal income tax is 13%.

(Total profit - tax deductions) * 13% = NDFL for IP on the ESS

If there is such a situation that the amount of tax deductions was less than the total profit, the tax base is recognized as zero. Accordingly, taxes for this reporting period will not have to be paid. You cannot transfer your loss to another year, since everything has been reset to zero since the beginning of the tax period.

In cases where a businessman has not conducted business activities throughout the reporting year, he is still obliged to provide tax inspectorate employees with a 3NDFL form, but with zero data. Only lines are filled in which general information about the entrepreneur is indicated. Pay nothing in this case.

CIP costs for OSNL otherwise referred to as professional tax deduction. Their correct accounting allows the entrepreneur to reduce the amount of tax payable. In this article, we present the rules, respecting which the IE can take into account occupational expenditures when calculating personal income tax. And also we will tell, due to what else reduction of tax burden on the income is possible.

What costs reduce personal income tax from the activities of PI

According to paragraph 2 of Art. 54 of the Tax Code of the Russian Federation, individual entrepreneurs keep track of expenses in the manner determined by the Ministry of Finance of the Russian Federation.

The expenses that an individual entrepreneur generates as a result of their business activities are called professional deductions for the purposes of calculating personal income tax.

In accordance with Art. 221 of the Tax Code of the composition of the expenses of the IP is determined by Chapter. 25 of the Tax Code.

These include:

- Material costs.

- The cost of labor.

- Depreciation.

- Other expenses related to business activities.

- The amounts of insurance premiums for pension and social insurance.

- The amount of taxes, with the exception of personal income tax and VAT.

The taxes that are included in the composition of the professional deductions for individual entrepreneurs also include fixed fees for GPT and OMS.

Tax on property of individuals is included in the deduction if the property is used in business.

Accounting for expenses

There are 3 conditions under which the PI can take into account the costs for calculating the personal income tax:

- they must be paid;

- used in the professional activity of IP;

- the purchase of materials, goods, works, services must be supported by documents (invoices, acts, invoices).

If for some reason an entrepreneur cannot provide documentary evidence of his expenses, then he can use a professional deduction in the amount of 20% of the amount of income received.

However, it is impossible to take into account both documented expenses and a standard of 20%.

IP expenses have recognition criteria, which are reflected in the Order of Accounting for income and expenses and business transactions for individual entrepreneurs adopted by the Ministry of Finance of the Russian Federation (order No. 86n of August 13, 2002):

1. There is a connection between income and expenses of an entrepreneur, i.e. expenses can be included in the personal income tax deduction only in the current or subsequent period in which revenues are received (letter of the Ministry of Finance of the Russian Federation of 05.09.2015 No. 03-04-05 / 8 -1063).

2. Expenses for the purchase of raw materials, materials, goods can be included in the professional deduction of individual entrepreneurs only if they are written off for production, sales, because the relationship between income and expenses must be observed.

Example

In November 2016, the company acquired 100 sets of bed linen for the price of 2,500 rubles. without VAT for subsequent sale.

In December 2016, the PI sold 25 sets. At the end of 2016, he can include in the composition of professional deductions 2 500 rubles. × 25 sets = 62 500 rub.

The rest of the product was sold in January 2017.

The individual entrepreneur will be able to include in the professional deductions the cost of purchasing goods in 2017 in the amount of 2 500 rubles. × 75 sets = 187 500 rubles.

3. Amounts of accrued depreciation can be included in the composition of professional deductions only for property and intellectual property that are held by individual entrepreneurs and used by individual entrepreneurs when conducting business. Even if the property is jointly owned by the spouses, one of whom is an individual entrepreneur, the accumulated depreciation can also be used to reduce the individual entrepreneur’s income (letter of the Ministry of Finance of the Russian Federation of 07.12.2012 No. 03-04-05 / 3-1377).

4. With the seasonal nature of the work, it is also necessary to observe the principle of the connection between the income received and expenses incurred.

An individual entrepreneur is exempt from the obligation of accounting, however, when accounting for labor costs of employees, an individual entrepreneur may also include the labor costs of an accountant as part of professional deductions, since, according to clause 23 of the procedure for recording income and expenses, an individual may reduce his income for any accruals remuneration of employees who work under labor contracts.

If the PI applies several tax regimes, for example, OSNO and UTII, then it should keep separate records of income and expenses for these regimes. An individual entrepreneur may accept only documented expenses associated with the general tax regime for calculating personal income tax.

"Non-entrepreneurial" ways to reduce personal income tax

In addition to the considered occupational offset, which occurs in individual entrepreneurs as a result of business activities, an entrepreneur can also reduce his personal income tax due to standard, social and property deductions. Their list is given in Art. 218-220 Tax Code.

Consider the features of the use of deductions on the example of the cost of training.

Thus, the right to receive a deduction on the cost of educating children remains until they reach 24 years of age. When calculating the deduction for the education of children, the amount of expenses for each child of 50,000 rubles can be taken into account.

Example

The businessman Mikhailov D. B. has two children.

The son attends the preschool department of school number 2025 in Moscow. The cost for the year for his maintenance at the school amounted to 30,000 rubles.

He also attends an art school, with an annual tuition of 25,000 rubles.

The daughter attends the State Sports Educational Institution “Sports School No. 7”, where the cost of classes per year is set at 54,000 rubles.

Due to the expenses incurred by the individual entrepreneur Mikhailov D. B. intends to declare a deduction of 13,000 rubles. (50,000 rubles. × 2 × 13%).

The total amount of expenses for which a social deduction can be granted to an entrepreneur, with the exception of the costs incurred for expensive treatment and education for children, cannot exceed 120,000 rubles.

Example

In 2015, IP Mikhailov D. B. paid for his studies in the MBA program in the amount of 60,000 rubles. and the annual maintenance program in the medical clinic in the amount of 80,000 rubles.

Total produced by IP Mikhailov D. B. social expenditures: 140,000 rubles. (60,000 + 80,000).

However, due to the existing restrictions in the composition of social deductions from 140,000, only 120,000 rubles can be taken into account.

Is the 2016-2017 PIT for the employees in the OSNO and USN "income minus expenses" included in the expenses?

NDLF entrepreneur pays not only for himself. When income is paid to employees, he becomes a tax agent for a payroll tax and is obliged to calculate, retain the workers and pay this tax to the budget.

With both the OSNO and the USN with the object “income reduced by the amount of expenses”, an IP can take into account the amount of the transferred personal income tax — not as an independent expense, but as part of the labor costs of employees with whom a labor or civil law contract is concluded. In other words, the salary is taken as an expense without reducing it to the withheld personal income tax. This is confirmed by the Ministry of Finance (letter dated 12.15.2015 No. 03-11-06 / 2/5880, dated 12.19.2008 No. 03-04-05-01 / 464).

Results

In order to correctly calculate the tax base for personal income tax, an individual entrepreneur must take into account the peculiarities of recognizing expenses set forth in the Tax Code of the Russian Federation, as well as in the Procedure for recording income and expenses and business transactions for individual entrepreneurs approved by the Ministry of Finance.

Photo from susanin.udm.ru

Photo from susanin.udm.ru

Throughout the year, the entrepreneur pays the so-called advance payments. Details can be found in the Tax Code in the seventh paragraph of Article 227.

Advance payments of income tax are made on the basis of tax notices. So, during the year in the process of entrepreneurial activity income arose. As an individual entrepreneur, you must submit to the tax inspectorate a corresponding declaration indicating the amount of the estimated income from business activities in the current tax period.

The declaration is made five days after a month has passed, from the day the income appeared. This applies to those entrepreneurs who received income for the first time.

The tax officers themselves will calculate the amount of advance payments for the current tax period. They do this on the basis of the estimated income indicated in the tax return or on the basis of the factual income received in the previous tax period. In this case, the relevant tax deductions are taken into account. Then the tax writes the corresponding notice for the payment of advance payments on personal income tax. Terms can be found in article 227 of the Tax Code of the Russian Federation.

Today, the following terms are valid:

1) for the period January-June, not less than July 15 of the current year in the amount of half of the annual amount of advance payments;

2) for the period July-September - no later than October 15 of the current year (in the amount of a quarter of the amount of av. Payments);

3) for the period October-December - no later than January 15 of the following year in the amount of the fourth part of the amount of advance payments.

If the actual income will differ by more than 50% from that expected in one direction or another, then you need to fill out a new tax return.

And the total tax amount for the year is calculated in accordance with the annual tax return. It takes into account taxes withheld by tax agents who paid NTFP for you (as employers usually do). It also takes into account the amount of advance payments that you made during the year. As I understood from the muddy tax codeThe total amount of personal income tax is paid no later than July 15 of the year following the end of the tax period. But it still needs to be clarified.

I remind you that the IE pays personal income tax if it is on the general taxation system (DOS). As I understand it, you do not need to pay for personal income tax.

Also, if you yourself are an employer, then before you pay your salary, you yourself are obliged to withhold from it the personal income tax (PIT).

In general, the personal income tax rate is 13% and is one of the lowest income taxes in Europe. On the other hand, it is compensated

An individual entrepreneur who is engaged in an activity in respect of which he applies the general tax regime is obliged to submit to the tax office a personal income tax declaration in accordance with paragraph 5 of article 227 of the Tax Code. This income declaration for 2011 is submitted by individual entrepreneurs according to the form approved by the order of the Federal Tax Service of the Russian Federation No. MMB-7-3 / 25.112010 [email protected] Consider the procedure for the presentation of the 3-NDFL IP on the OSNO, as well as the timing of payment of tax payments.

Declaration 3-NDFL

The personal income tax declaration must be submitted to the tax authority no later than April 30 of the year following the last tax period.

The declaration must be submitted not only if the activity is conducted, but also:

- if business activity is not carried out;

- there is no amount of tax payable or income from business activities.

The declaration is accompanied by documents confirming the tax deductions provided.

What will happen if the 3-NDFL IP on the ECHO does not file on time? Failure to submit a declaration provides for a penalty of 5% of the unpaid tax amount per month, starting from the day fixed for its submission. The maximum amount of the fine is 30% of the tax amount, the minimum is 1000 rubles. Therefore, the filling of 3-NDFL and its submission should be carried out in a timely manner.

The amounts and terms of payment of advance payments on personal income tax

The amount of advance payments is calculated at the tax inspectorate for 4-NDFL declarations for newly starting entrepreneurs, data of the 3-NDFL form for the previous year or refined 4-NDFL declarations in the event of a significant change in the level of expected income (more than 50%). After calculation, the inspectorate sends a notice to the entrepreneur, in which the amounts and terms of advance payments are indicated.

Deadlines for payment of advance payments:

- for January-June - no later than July 15 of the current year in total? annual value of advance payments;

- for July-September - no later than October 15 of the current year in total? annual value of advance payments;

- for October-December - no later than January 15 of the next year in total? annual value of advance payments.

Failure to pay an advance

What will happen if for some reason the UI does not pay the advance payment on time? Court decisions indicate that the accrual of penalties and fines in this case is illegal. This is due to the fact that the advance payment is not calculated on the basis of real financial results, but is based on the results of previous periods or estimated in the current year. If the advance payment is not paid, there will be no tax arrears.

However, the payment of advance payments is usually in the interests of the entrepreneur himself, since the payment of the tax amount in several stages with a smaller amount of payment creates a smaller burden for the business than a single payment of a large amount of tax.