Calculation of tax on the site. Step-by-step instructions for calculating and paying land tax

Land tax for individuals defined in chapter 31 of the Tax Code Russian Federation and charged on land owned by the taxpayer on the right of ownership, on the right of unlimited use or lifelong inheritable possession. Payment procedure land taxas well as benefits and tax rates on it vary in different regions of Russia, since the land tax applies to local taxesand, accordingly, is regulated by local regulatory acts of municipalities, and for Moscow, St. Petersburg and Sevastopol, as subjects of the federation, by the laws of these cities (see clause 4 of article 12, clause 1 of article 15 and article 387 of the Tax Code RF).

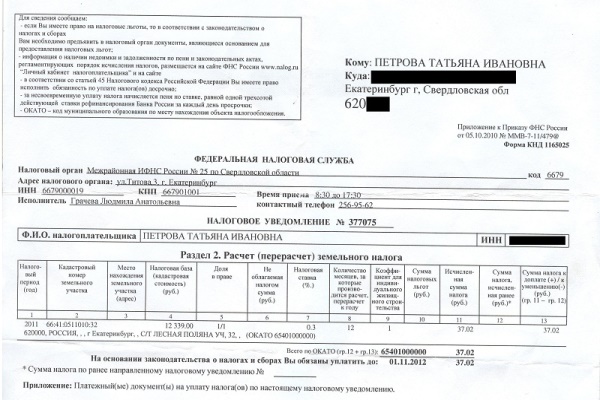

According to the law, the regional divisions of the Federal Tax Service (FTS) are engaged in the calculation of land tax for taxpayers of individuals. Each taxpayer receives from the FTS a tax notice, which indicates the amount of land tax payable, as well as the initial data for which it was calculated (clause 3 of article 396, paragraph 4 of article 397 of the Tax Code of the Russian Federation).

AT tax notice It includes such information as the tax rate, the year for which the tax is calculated, the cadastral number and address of the land plot for which the tax is paid, the cadastral value of this land plot (determines the size of the tax base), the amount of tax and the tax benefits available.

However, any taxpayer has the right to independently calculate the land tax for individuals and check whether the FTS has correctly determined the amount of tax on its land.

The formula for calculating land tax for individuals

Currently tax law Russian land tax is calculated by the formula:

Land tax = St x Kst x D x Sq

- St - tax rate

- Kst - cadastral value of the plot,

- D - share in the ownership of the land,

- Kv - land ownership ratio.

This land tenure ratio is used in the formula in the case when the owner owns a land plot less than one calendar year.

In this publication I will explain in detail how to calculate the land tax for individuals in just a few steps:

Step 1. Determine whether you are eligible for tax rebates?

Tax benefits exist federal and municipal. The privileges of federal significance of the Tax Code of the Russian Federation (clause 7 of Article 395) include benefits granted by the FTS to small indigenous peoples of the North, Siberia and the Far East. Benefits are granted to this category of persons to pay tax on such landwhich are traditionally used by these nations for the preservation and development of their way of life, traditional economy and folk crafts.

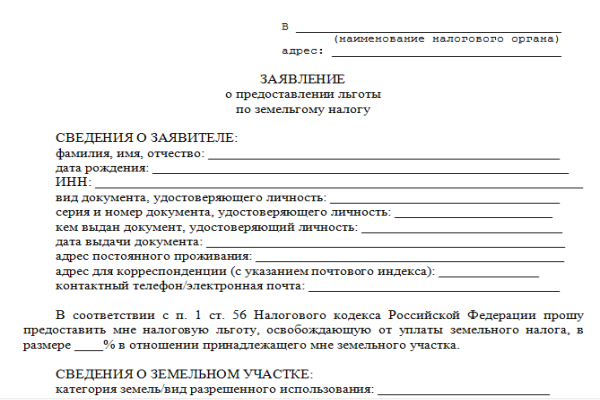

About municipal tax breaks You can find information directly in the legal act of the authority of your city, town or other municipality (paragraph 2 of article 387 of the Tax Code of the Russian Federation), as well as in the territorial body of the Federal Tax Service at the place of your land plot. If the taxpayer belongs to the preferential category of citizens on land tax, he sends a statement with the application confirming the right to the benefit of documents directly to the FTS Inspectorate (clause 10 of article 396 of the Tax Code of the Russian Federation).

Step 2. Determine whether the cadastral value of your land is correct

The tax base is the cadastral value of your land, which is taken as of January 1 of the year for which the land tax is calculated. According to Clause 1, 4 of Art. 391 of the Tax Code, cadastral value land plots FTS takes in the USR Rosreestra. Correctness of determining the tax base, respectively, can be checked only in one way: take an extract about the cadastral value of your memory in the Federal Registration Service. To do this, you must send a written request to the Rosreestr authority or cadastral chamber at the location of your storage device. Important: in the request you need to specify the date on which you need to know the cadastral value. If you do not specify this time, you will receive a document with the cadastral value on the date of the filing of your application. The order of Rosreestra No. P / 0515 of October 18, 2016 (paragraph 1.4) and Law No. 218-FZ of July 13, 2015 (Part 4 of Article 63) determine that the extract on the cadastral value of the memory is issued to citizens free of charge.

If in the current year the cadastral value of the plot has increased, this change will affect the tax calculation only next year. Tax for the current, and even more so for the past year will be calculated on the basis of the previous cadastral value of the memory. But if a cadastral registration body made a technical error in the cadastral value of a plot, then after correcting the error, the corrected cadastral value is taken into account in the calculation of the tax base immediately, starting with the year when the mistake was made.

Please note that by the decision of the court or the decision of the dispute resolution commission on the results of determining the cadastral value. In this case, changes in the cadastral value should be taken into account when calculating the land tax from the year in which the application for the revision of the cadastral value was submitted. However, the change in the cadastral value starts to be taken into account no earlier than the moment of making a record of the cost of the charger in the Register (paragraph 1 of Art. 391 of the RF Tax Code, Letter of the RF Federal Tax Service No. BS-4-21 / [email protected] from November 07, 2016).

In the letter of the Federal Tax Service of the Russian Federation No. BS-4-21 / [email protected] dated November 16, 2016, it is indicated that during tax period the change of the cadastral value of a plot of land due to the correction of an error in the register value of the object is not allowed.

What is a registry error and a technical error?

A registry error is an error made in the USRN in the map-plan of the territory, or a technical plan or inspection report. The reasons for such an error may be erroneous data submitted in the documentation sent to the Rosreestr by other bodies in the order of information interaction or other persons, as well as errors of the cadastral authority in its implementation and the state. registration of ownership (see part 1 of article 3 of article 61 of Law No. 218-ФЗ).

Technical errors, which include any typos, clerical errors, grammatical errors or errors in arithmetic. A technical error may be made by an authorized person of the cadastral authority when committing such actions as state registration of rights or cadastral registration. The result of such an error is a discrepancy between the data from the documents submitted to the Rosreestr body for entering information into the Register and the data entered into the Register.

Certain categories of citizens have the right to decrease the cadastral value of one of their land plots in the territory of one municipal entity by 10,000 rubles. Such categories, in particular, include disabled children, disabled people of groups I and II, disabled people and combat veterans. In order to exercise this right, these citizens must submit documents to the FTS (see Tax Code of the Russian Federation, clauses 5 and 6 of Article 391).

A land plot may belong to several owners as joint ownership or joint ownership. In the first case, the tax base is calculated for each owner in proportion to the size of his share. If the plot is owned by several owners on the basis of common ownership, the tax base is divided equally for each owner (clause 1, 2, article 392 of the Tax Code of the Russian Federation).

Step 3. Clarify the correct tax rate in your case.

In accordance with Art. 394 of the Tax Code, the tax rate, depending on the category of land to which the plot belongs, is established by local legislation. Land tax rates are published on the official website of the municipality in the relevant legal act. So, for Moscow, tax rates are defined in the Law of Moscow No. 74 dated November 24, 2004.

The maximum amount of the land tax rate, within which the rate can be established by local legislation, is set out in Clause 1, Article. 394 of the Tax Code of the Russian Federation. So, for agricultural land, cottage and farms set maximum rate - 0.3%. Tax rate for all other categories of memory is 1.5% (see paragraphs 1, 2, paragraph 1 of article 394 of the Tax Code of the Russian Federation).

If the municipality does not set the land tax rate in local regulations, the tax will be calculated at the rates established in paragraph 1 of Art. 394 and in paragraph 3 of Art. 394 of the Tax Code of the Russian Federation.

Step 4. Independently calculate the amount of land tax

Land tax is calculated as the product of the tax base and the tax rate (see section 1 of article 396 of the Tax Code of the Russian Federation). Land tax in respect of acquired by an individual or provided in the property for the construction of housing plots of land in some cases, a raising factor is applied in accordance with Clause 15 and 16 of Art. 396 of the Tax Code of the Russian Federation.

Thus, the coefficient that increases the land tax by 2 times, begins to apply 10 years after the date of registration of ownership of a plot of land for individual housing construction and until the moment of state registration of ownership of a property built on the plot (clause 16 of article 396 of the RF Tax Code) .

The land tax in the year of the acquisition or sale of the memory is calculated from the number of full months in which the memory was owned by this person. To calculate the land tax, the month of ownership of a plot is taken for a full month if the purchase of a land plot occurred before the 15th day of the month (inclusive) or its sale occurred after the 15th day. Otherwise, when the purchase of the memory occurred after the 15th of the month or its sale - before the 15th day inclusive, this month is not taken into account when calculating the tax.

Do not forget to take into account when calculating the tax benefits or the right to a non-taxable amount in the presence of such rights. If the taxpayer receives a land plot as an inheritance, then in accordance with paragraphs 7 and 8 of Art. 396 of the Tax Code of the Russian Federation the tax starts to be calculated from the month of opening the inheritance.

Example of calculating land tax for individuals

Baseline: The plot for the management of private farms (personal subsidiary farms) is within the boundaries of the city of Moscow and belongs to the pensioner individually, starting from August 16, 2016, that is, for 2016 the site is owned for four full months (August is not taken into account, since the property hit already after the 15th). The cadastral value of the plot is 1,350,000 rubles. According to the Law of Moscow No. 74 of November 24, 2004, the tax rate is 0.025 percent of the cadastral value of the land plot.

The land tax for the year will be calculated according to the formula:

1 350 000 rub. x 0,025% x 4/12 = 113 rub.

If the taxpayer wants to check his calculations with the calculations of the FTS, he has the opportunity to do so on the FTS website, where the service of preliminary calculation of the land tax for individuals operates. The only thing that you need to enter into this calculator is the cadastral number of your storage device. The remaining data (cadastral value and land category) are entered and taken into account automatically by the service from the data of the Rosreestr.

Also on the website of the Federal Tax Service in the section "Taxes and fees in force in the Russian Federation" - "Land tax" provides background information revealing the details of the methodology for calculating land tax. The correctness of the cadastral value of the memory can be checked on the site Rosreestra - section "Cadastral valuation." In Rosreestre, you also need to clarify information about the characteristics of your storage device and resolve issues disputing the cadastral value if you disagree with it (see the Information of the Federal Tax Service "On calculating the land tax on the FNM of Russia website" dated March 4, 2016).

As a result of all the above steps, you should receive a land tax. If he coincided with the calculations tax inspection, questions are removed. If there is a difference, and you suspect that this error was made on the side of the FTS, we recommend that you write a statement to the FTS with attached supporting documents. When submitting an application to fix the date of admission, the FTS official must put a list on the second copy of the application, which remains with the applicant.

According to the legislation of the Russian Federation, land owners are obliged to pay tax on this type of property. How is it calculated based on the fact that a cadastral value is determined for a particular plot? What nuances characterize the calculation of the corresponding tax?

What are the principles for calculating land tax?

Calculation of land tax at the cadastral value is carried out regardless of the category of the taxpayer - whether it is a natural person or an organization. Moreover, for these purposes the same formulas are applied (which may include, however, different indicators, based on the status of taxpayers).

The main feature of land tax is that it is local. That is, the rules of its calculation are regulated not only federal lawsbut also the sources of law adopted at the level of municipalities. The rules adopted by local authorities in one city or district may differ significantly from those in the other in terms of tax rates, application of benefits, determining the timing of its payment, etc.

The duty of self-calculation of land tax is imposed only on legal entities. Tax on plots of private entrepreneurs and citizens is calculated by the FTS. But, nevertheless, it is useful for an individual to know the basic principles of calculating the payment for property represented by a land plot.

The formula for calculating the tax payment in question is fairly simple. To determine this indicator, you need to multiply the amount of the tax base (which depends to a decisive extent on the cadastral price of a plot) by the rate established in regulatory acts.

How to find out the cadastral value of the plot?

So, the main component of the tax base is the cadastral value of the plot.

Information about the cadastral value of the plots can be obtained by the interested person:

- from the cadastral map, which is posted on the Rosreestr website;

- through personal contact with the agency;

- from title documents (for example, certificates for acquiring rights to a plot, if it was issued after the cadastral value was established for the plot).

In general, the tax base for calculating the payment in question corresponds to the full cadastral value of the plot. However, if the period during which it is owned by the taxpayer for less than a year, the base is reduced relative to the proportion of 12 to the number of full months of ownership of the site. However, if the land is purchased after the 15th of the month, then it is not considered complete.

The cadastral value of the land plot owned by Ivanov, who bought it on November 20, 2016, is 12,000,000 rubles. The base for calculating the land tax in this case will be 1,000,000 rubles (12,000,000 rubles / 12 months per year) * 1 full month of ownership of the plot (December).

The next task after establishing the tax base is to determine the rate.

Calculation of land tax: how to determine the rate?

Above, we noted that the tax in question is local. Specific rates for it are set by municipal authorities or regional authorities in cities of federal significance. At the same time, they cannot exceed those indicators that are defined in Tax Code Russia, namely:

1. Rates in the amount of 0.3% for taxation of areas that:

- used in agriculture;

- used within the housing stock or housing and utilities infrastructure;

- purchased by the taxpayer for personal business, country housekeeping;

- have limitations in use based on the fact that they are provided for the security needs of the state.

2. Rates in the amount of 1.5% when taxing other areas.

At the same time, municipal authorities can accept differentiated rates in relation to the category of plots, their permitted use, and the location of the plot.

If the land plot owned by the taxpayer is located simultaneously on the territory of 2 different municipalities, then when calculating the tax for each of the land shares, the rates established by the respective municipalities are applied (they may, however, not coincide). The tax base in this case, is determined in proportion to the size of each share to the total area of the site.

Plot Petrov worth 12 million rubles has an area of 100 square meters. meters Of these, 30 square meters. meters falls on the territory of the municipal district A, while the other 70 square meters. m - to the territory of the municipal district B. Thus, a tax calculated on the basis of 3,600,000 rubles (30% of 12,000,000) will go to the budget of district A, and a tax calculated on the basis of 8,400,000 will go to the budget of district B. rubles (70% from 12 000 000).

Let us now consider how the actual land tax is calculated in practice.

Actual land tax: calculation features

Let us calculate what Petrov’s land tax should pay, on the basis of the fact that the rate established in municipality A is 0.1%, in municipality B it is 0.2%.

First, we determine the amount of tax payable by Petrov in the municipality A. It will be 3,600 rubles (0.1% of 3,600,000 rubles).

Then - a tax that is paid to the municipality B. It will be 16,800 rubles (0.2% of 8,400,000 rubles).

Thus, in total, Petrov will pay tax in the amount of 20,400 rubles (however, not in a single payment, but in these amounts separately to the budgets of the municipalities A and B).

Important nuance: municipalities may establish various exemptions for the tax in question. If the grounds for benefits are only partially applicable to the plots, then the tax is calculated in proportion to the taxable share of the plot.

Municipality A introduces a zero land tax rate for labor veterans. Petrov, having the appropriate status, has the right not to pay this tax to the budget of the municipality. Therefore, all he needs to do is transfer 16,800 rubles to the B. municipality.

This tax is faced by individuals and various organizations that have areas in their possession. This type of deductions for legal entities has its own characteristics, which will be described below. If your business is directly related to land sales transactions, then you must know what the land tax declaration is. This document reflects all amounts that will be paid. The land tax declaration is necessary document for any persons. In general, the land tax declaration is fairly simple to understand, and later in the article it will be described how calculations and other features are made. Knowledge of the features of the calculation will allow to properly dispose of possessions: they can be for sale or for construction. If the territory is for sale, then you should additionally familiarize yourself with the corresponding principal in the code, where the rules of sale are written.

Who should pay land tax in 2016?

In this case, taxpayers will be individuals and organizations. Sometimes this object is initially a part of a mutual investment fund, which was created by several legal entities. Then everyone pays land tax and uses for this purpose property that is part of this fund. Individuals are also required to pay these funds, but for pensioners and some other individuals there are benefits.

Term of payment of land tax

The calculation is made using the cadastral value of the site for the first of January of the year for which the amount should be accrued.

In this case, the calculations for individuals and legal entities will be made equally.

When the deductions will be paid for the first time, the land tax is paid immediately after the purchase, and the accrual is made at an estimated value. Land tax for individuals most often does not cause problems, and they do not encounter errors in the charges, as they receive a special receipt with the details and the already calculated amount from the local FTS service. It is more correct to contact the territorial FTS body and find out the coefficient, since they have the full right to change the coefficient, and the rate is a non-permanent parameter.

Most accountants already have a standard form for such calculations, but sometimes the following data is multiplied:

- Cadastral value of the plot for 1 square meter;

- The fixed rate factor for your region;

- The area of the object.

How to get a break

The maximum amount of benefits for businesses and individuals is not more than 10,000 rubles. Taking into account privileges, the payment of land tax becomes affordable even for pensioners and other citizens, whose income is below average. For pensioners, the payment of the full amount will be an impossible task, therefore the benefits for them are most welcome.

Some individuals have benefits for this type of deduction:

- Persons who are Heroes of the Soviet Union or Russia;

- Persons with disabilities of the first and second degree;

- Persons who have tested nuclear weapons;

- Persons who have eliminated the accident at the Chernobyl nuclear power plant or those who are sick with radiation sickness;

- Persons with disabilities since birth.

It should be remembered that the presence of any of these statuses will allow you to pay less or not to pay only when the right to preferential payment is issued. It is necessary to collect and submit documents to the Federal Tax Service, but for any legal entities there will be no land tax only if there is no business activity in this territory.

Thus, land tax benefits must be confirmed, otherwise you will be required to pay on a par with everyone.

Sum calculation examples

Declaration of land tax for the year

Example 1. Calculation of land tax for the whole year (12 months)

Ivanov KI has land in the Moscow region. This territory was put up for sale, and for it the cadastral value in 2016 will be at least 3,500,000 rubles. Calculations are made taking into account what the rate is, which for land in the Moscow region is set at 0.3%. Then the amount will be: 10 500 rubles. (3500 000 x 0.3 / 100). It is in this volume that land tax should be paid.

Example 2. Calculation for a certain number of months

Ivanov KI decided to register land in July 2015. Prior to this, the property was intended for sale and registered to another owner in the Moscow region. The cadastral value was 3 500 000 rubles. The calculation of deductions will be made as follows: for the Moscow region the rate is not less than 0.3%, then the deductions for the four months of 2015 are: 5,250 rubles. (3 500 000 x 0.3 / 100 x 0.5), where 0.5 is the time ratio when Ivanov KI was the owner of the site (6 months. / 12 months.)

Example 3. Calculation for the share of land when it is owned by several persons

When the plot was intended for sale, Ivanov and his friend divided the amount in half. For him, the cadastral value in 2016 is equal to 3,500,000 rubles. The rate will be 0.3%, and deductions are: 5,250 rubles. (3,500,000 x 0.5 x 0.3 / 100).

Example 4. Calculation with benefits

Grandchildren of the participant of the Great Patriotic War Ivanov KI they saw that the plot was for sale, and they suggested that the grandfather buy it. The cadastral value of land in 2016 is 3,500,000 rubles. The rate does not change and will be 0.3%. Deductions taking into account benefits will be equal to: 10,470 rubles. ((3 500 000 - 10 000) x 0.3 / 100), where 10 000 rubles. - privilege for Ivanov KI, as he is a member of the Second World War.

Tax notice

Individuals receive a document from the Federal Tax Service, which determines what the land tax will be, in these notifications the amount will be based on which cadastral value and what rate is applied in a particular area.

It is the Federal Tax Service that monitors for what purposes the land is used: for sale or there is some kind of activity on it.

If for sale, then there should be documentation about who the plot will be sold to. In 2016, notifications must be received from April to September. To find out more accurate deadlines for receiving a notification, you should contact the appropriate authority in your city. If the calculations are done incorrectly, you have the full right to file an application and wait for the recalculation. Everyone can use this right, so that the calculation will be made, both for businessmen or companies, and for all pensioners.

Payment term

In 2016, for all regions of Russia, one-time deadlines were set for the payment of property deductions - no later than October 1, 2016, and it is strongly not recommended to pay land tax later.

It should be remembered that in case of overdue payment, you will be required to pay a penalty of approximately 20% of unpaid amount, as in addition to it, penalties are charged for each day of the calendar from October 1st until the moment of payment.

So it is more convenient to meet the deadline for payment.

Indexation coefficient of standard monetary value

The most popular or convenient to pay through the online service. This method is suitable for businessmen and retirees, if the former can independently deal with the system, then retirees have children or grandchildren who will help make the first payment. The second option is to come to the Federal Tax Service, fill out the necessary receipts and deposit the required amount of money.

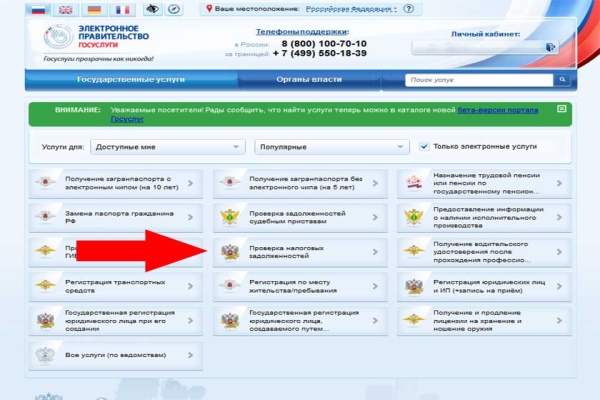

How to find out your debt in 2016

Tax Debt Verification

Debt can be learned in different ways: first - contact the FTS in your city in person or second - go to your personal Area on the FTS website. On the same site you can consult.

Video

You can watch the video, which tells in detail about the land tax.

If they have not done so, then total bet - 1.5%, and for some categories of land (including for agricultural land) - 0.3% clause 3 Art. 394 of the Tax Code.

The category of land (its purpose) can be indicated, for example, in an extract from the Unified State Register of Real Estate (USRN), a certificate of title to a land plot, a plot sale agreement, as well as in the state real estate cadastre section 2, Art. 8 of the Land Code of the Russian Federation.

For example, in Moscow, the stakes are established by the Law of November 24, 2004, N 74, and in St. Petersburg, by the Law of November 23, 2012, N 617-105.

How to find out the cadastral value of land for land tax

The tax base for land tax is the cadastral value of land as of January 1 of the year for which tax is paid. art. 390 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of 29.03.2017 N BS-4-21 / [email protected] .

If the land plot is formed during the year, then the cadastral value is taken on the day the information is entered in the Register, which are the basis for determining the cadastral value clause 1, Article. 391 NK RF.

The cadastral value of the site is approved by regional regulations Letter of the Ministry of Finance of 17.06.2015 N 03-05-06-02 / 34985. You can find out the cadastral value of your site, for example, by sending a request to Rosreestr via the website (https://rosreestr.ru/wps/portal/p/cc_present/EGRN_2) p. 2 of the Government Decree dated 07.02.2008 N 52, Information of the Federal Register of State Registration dated 02.10.2017, p. 30 of the Procedure for the provision of information.

The annual amount of tax (if the organization does not have) is calculated by the formula clause 1, Article. 396 NK RF:

If the ownership of the land plot has arisen or ceased during the year, then the amount of tax on such a plot is calculated based on the number of full months during which you owned it this year.

When calculating the tax for the full month is taken in which clause 7 of Art. 396 NK RF:

registered ownership of the plot, if it happened before the 15th day of the month inclusive. If the property right is registered after the 15th, then this month is not taken into account when calculating the tax. For example, if the ownership of a plot arose on November 15, then the number of full months of ownership is 2, and if on November 16, then 1;

registered termination of ownership of the plot, if it happened after the 15th of the month. If the ownership right has ceased until the 15th day inclusive, then this month is not taken into account when calculating the tax. For example, if the land is sold on November 15, then the number of full months of ownership is 10, and if November 16, then 11.

The amount of tax for an incomplete year is calculated by the formula pp 1, 7 tbsp. 396 NK RF:

If you do not have to pay advance tax payments, then the entire annual amount of tax must be paid to the budget.

If during the year you made advance payments, by the end of the year the tax should be transferred to the budget in the amount calculated using the formula section 5, Art. 396 NK RF:

Who should pay advance payments on land tax

The organization must advance payments on land tax for the results of 1, 2 and 3 quarters, if the normative act of local authorities, in whose jurisdiction is the area where the land is located, at the same time:

are set accounting periods land tax clause 3 Art. 393 NK RF;

there is no exemption from advance payments for taxpayers, including your organization. section 9 of Art. 396 NK RF.

If the organization does not have, then the amount of the advance payment of land tax for 1, 2 and 3 quarters is calculated equally according to the formula section 6 of Art. 396 NK RF:

If the ownership of the land plot has arisen or ceased during the year, the amount of the advance payment for such a plot is calculated taking into account the number of full months during which you owned it in the reporting period.

In this case, the full month is taken in which clause 7 of Art. 396 NK RF:

registered ownership of the plot, if it happened before the 15th day of the month inclusive. If the ownership is registered after the 15th, this month is not taken into account when calculating the advance payment. For example, if the ownership of a plot arose on November 15, then the number of full months of ownership of a land plot is 2, and if on November 16, then 1;

registered termination of ownership of the plot, if it happened after the 15th of the month. If the ownership right has ceased until the 15th day inclusively, then this month is not taken into account when calculating the advance payment. For example, if the plot is sold on November 15, then the number of full months of ownership of the land plot is 10, and if on November 16, then 11.

The organization has no land tax exemptions.

Calculation of land tax on the plot N 1.

Advance payments for 1, 2 and 3 quarters will amount to 16,026 rubles. (64,105,865 rubles x 0.1% x 1/4).

Calculation of land tax on the plot N 2.

The tax for the year (line 280, section 2 of the declaration) will be 72,471 rubles. (58,000,000 rubles x 1.5% x 1 months / 12 months).

The calculation of the total amount payable to the budget.

Advance payments (lines 023, 025, 027, section 1 of the declaration) for 1, 2 and 3 quarters will amount to 16,026 rubles each.

The calculated tax amount for the year (line 021, section 1 of the declaration) - 136,577 rubles. (64 106 rubles. + 72 471 rubles.).

The tax payable for the year (line 030 section. 1 of the declaration) will be 88,499 rubles. (136 577 rubles. - (16 026 rubles. + 16 026 rubles. + 16 026 rubles.)).