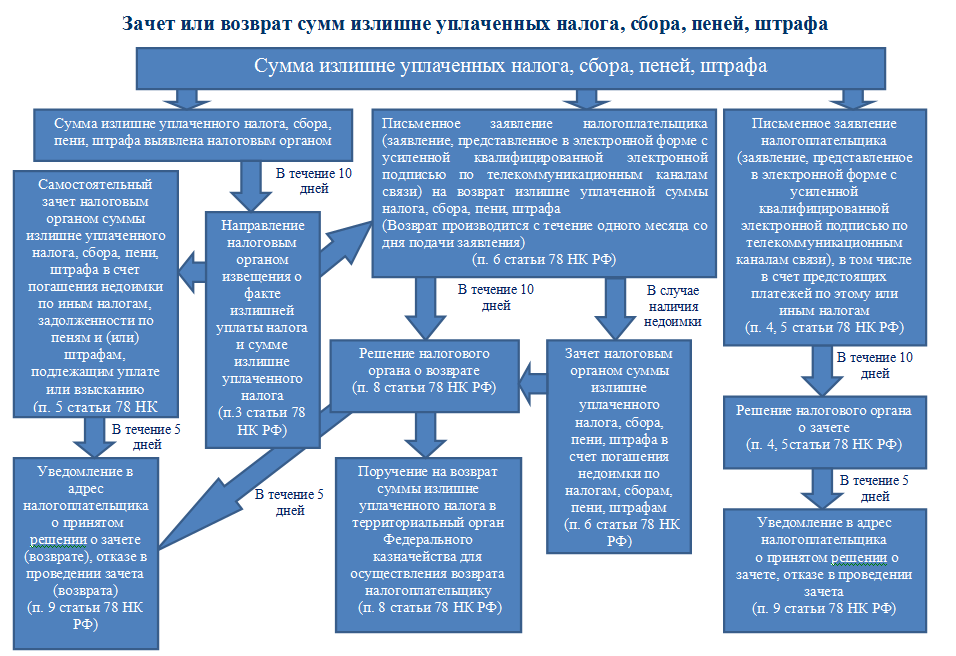

The amount of tax, penalties and fines. Statement of return or offsetting overpayment

From March 31, 2017, the application for the return and offset of overpaid taxes, fees, penalties and fines, approved by order of the Federal Tax Service dated 03.03.2015 No. ММВ-7-8 / [email protected], expire. Now these documents will need to be submitted in accordance with the new forms approved by the order of the Federal Tax Service of Russia of February 14, 2017 No. MMP-7-8 / [email protected]

If you want to return or reckon overpaid tax, then this information is for you.

There are several significant differences from the old forms.

The first is the number of pages of the application. The old forms consisted of 1 sheet, the new ones contain 3 pages (if this is a return request) and 2 pages (if this is an application for offset).

The second is the application form. The old forms were compiled in the form of a business letter; legal entities to the details of the organization will need to fill out the name of the head of the organization or its representative.

The third, and probably the most significant difference, is that you can return or redeem the overpayment not only on taxes, but also on contributions to compulsory pension insurance, compulsory medical insurance and on payments for temporary disability and in connection with maternity. This is due to the fact that from January 1, 2017, insurance premiums for compulsory pension and medical insurance, as well as for temporary disability and in connection with maternity, are regulated by the Tax Code of the Russian Federation and reports are filed with the tax authorities.

From 2017, you cannot read different types of insurance premiums. Settlement is allowed only within contributions of one type (clause 1.1.1 of Art. 78 of the Tax Code of the Russian Federation). For example, overpayment of pension contributions from 2017 can be credited only against future payments on them. To offset this overpayment on account of arrears on medical or social contributions, the organization since 2017 does not have the right.

You can file an application for offsetting or returning the amount of overpaid tax within 3 years from the date of payment of this amount. The decision on it is made by the tax authority within 10 days from the date of receipt. Within 5 days after the decision is made, the tax authority must inform you of its decision. The specified message is transmitted to the head of the organization, an individual, their representatives personally on receipt or by other means confirming the fact and date of receipt.

If the overpaid amounts are not refunded within the prescribed period of 1 month, then you can charge interest on their amount at the refinancing rate of the Central Bank of the Russian Federation for each calendar day of delay in return (Article 78 of the RF Tax Code). But if the taxpayer has debts on taxes, penalties, fines, the overpaid amounts go, first of all, to pay off such debts (clause 1 of article 79 of the RF Tax Code).

The inspectorate has the right to take the decision on offsetting overpaid tax within 10 days from the date of filing the application. And many organizations believe that the tax can be considered paid on the day of submission of the application for offsetting the overpayment of this tax. However, the authorities (letters of the Ministry of Finance of Russia dated August 02, 2011 No. 03-02-07 / 1-273, dated July 25, 2011 No. 03-02-07 / 1-260) have a different opinion. They believe that the tax should be considered paid only on the day of signing the decision on offsetting the overpayment, that is, when the tax is directly credited (subclause 4 of paragraph 3 of article 45 of the RF Tax Code).

It turns out that if the organization filed an application for offset on the last day of tax payment, then until the inspection made its decision (within 10 working days) the tax will be considered unpaid. So, for each calendar day of delay in tax payment, penalties are charged starting from the date of payment established by law and until the day of the decision on offsetting (clause 2 of article 57, clause 3 of article 75 of the RF Tax Code).

In addition, employees of the financial department previously indicated (letter of the Ministry of Finance of Russia dated February 12, 2010 No. 03-02-07 / 1-62) that the Tax Code does not provide for recalculation of the amount of penalties that are accrued before the tax authority decides to offset the amounts overpaid tax.

However, according to the courts, if the inspectorate gave the go-ahead for the set-off, the accrual of penalties is illegal. Thus, in one of the decisions, the arbitrators explained that the accrual of penalties is made in order to compensate for budget losses as a result of late payment of tax amounts. In the dispute under review, the budget did not incur any losses, which means that the tax authority’s accrual of penalties is illegal. The judges also indicated that the organization had duly executed the tax payment obligations, sending a statement about the conduct of offsets before the due date for the tax payment. In this regard, the accrual of interest by the tax authority is illegal (post. FAS PO dated May 15, 2008 No. A57-14501 / 07-17).

Other courts also supported organizations and explained that, in accordance with paragraph 1 of Article 75 of the Tax Code, penalties are payable in the event of arrears, that is, the amount of tax not paid in the statutory period.

Note that in court it is important to prove that the firm submitted an application for offset no later than the deadline for paying the tax, and that the budget did not suffer any losses.

As we see, the position of the Ministry of Finance of Russia is not the only one, and if the company is ready to go to court, then there is a chance to win the case. However, not all companies are ready to defend their point of view in court, so we will show you how to act in order to overpay in time.

Local tax inspectors are likely to adhere to the opinion of the Russian Ministry of Finance and charge fines. So, the company should heed the advice of financiers. To overpay on time, the organization should:

- when overpayment is found, reconcile with tax;

- submit an application for offset before the expiration of the tax payment period, but not later than 10 days before this point (otherwise, the inspectorate has the right to accrue penalties before the date when the decision on offset was taken);

- control every tax step: whether the statement reached the executor, at what stage the decision is.

There are often situations when a firm submits an application to set off an overpayment on time and the tax inspectorate “does not notice” it. In fact, the tax is not paid, which is the fault of the tax authority itself. Therefore, claims regarding non-payment of tax, on account of which a statement of credit is written, are unfounded. So, it is illegal to collect the amount of tax and penalties and fines charged on it from the organization, since the company actually had no debt in this amount. These amounts were listed for the company due to the omission of the inspection, which did not take a decision on the offset of the excessive amounts collected in a timely manner if there were legal grounds for this. Therefore, in a similar situation, an organization should go to court and indicate the presence of a tax overpayment.

Recall that the overpayment on tax can be set off only at the same budget level (federal, regional, local) in which there was a surplus.

If the organization overpaid the tax and there is a backlog on other taxes, arrears of penalties and fines, the tax authority has the right to independently set off this surplus to repay. But if you need a credit for upcoming payments on this or other taxes, you need a written statement of the company. It should be in any form. The main thing is to indicate in it the details of the organization, the tax on which the overpayment occurred and what payments it should be sent to. It will also be useful to indicate the reason for the overpayment and attach supporting documents (for example, a payment order, bank statement).

Examination of the article:

Maxim Zolotykh ,

legal advisor expert GARANT, legal adviser

Each taxpayer may form overpayment on taxes. Overpayment is incurred if the taxpayer pays taxes (penalties, fines) in a larger amount than is required by law. Yes, and tax authorities often sin excessive recovery payments to the budget.

In any case, the taxpayer has the right to timely offset or return amounts unduly transferred or charged to the budget.

The credit and return of overpaid (overcharged) amounts of contributions, penalties, fines are also provided for by the legislation of state funds:

- Pension Fund of the Russian Federation ( FIU),

- Federal Fund for Mandatory Medical Insurance ( FFOMS),

- Social Insurance Fund of the Russian Federation ( FSS).

- Incorrect tax calculation: inaccuracy in calculating the tax base, applying the wrong tax rate, etc. Moreover, the payment is recognized overpaid, if the taxpayer himself, without the participation of the tax authority, incorrectly calculated the amount of the payment.

- Errors in filling out payment orders for the payment of tax, penalties, fines, which entailed transferring them to the budget in an excessive amount. For example, an indication by a taxpayer in a payment of an overestimated amount to payment of an incorrect BCF may lead to this.

- Amendments to tax legislation, the effect of which applies to previous periods. For example, a tax overpayment may occur when a benefit is introduced, which has been applied since the beginning of the current year.

- According to the results of the tax period, the amount of tax to the reduction is calculated.

- Change the tax regime.

- Recovery by the tax authority of the excess amount of payments to the budget.

Excessively collected the amount of tax (fine, fine) is the amount that the tax authority accrued, reflecting this in the decision on the basis of the tax audit and (or) in the claim.

It does not matter if the payer paid the corresponding amount independently (on the basis of a request or decision) or was forcibly collected by the tax authority.

Overpaid the amount of tax (fine, fine) is the amount that the payer himself (without the tax authority) calculated in excess or was mistaken in specifying the payment in the payment order (receipt).

In the second case, in accordance with article 78 of the Tax Code, the tax authority must inform the taxpayer about each fact of taxation that has become known to tax authorities and the amount of overpaid tax within 10 days from the date of the discovery of such a fact.

Attention! In practice, the tax authorities do not report the presence of an overpayment, since there are no sanctions for non-compliance with this procedure.

In case of discovery of facts testifying to the possible overpayment of the tax, a joint arrangement may be carried out upon the proposal of the tax authority or the taxpayer. reconciliation of calculations. The total time for reconciliation of payments is 10 business days. The results of such reconciliation are documented by an act.

First of all, the overpayment is sent to pay off the arrears and penalties. In this case, the tax authorities can, without an application from the taxpayer, pay the arrears on account of overpayment. This tax report to the taxpayer during 5 working days from the date of the decision.

Attention! The tax authority does not have the right to independently offset the overpaid tax to repay arrears and arrears of penalties, the possibility of compulsory collection of which has been lost.

If the taxpayer does not have any arrears or penalties, he is entitled to set off the overpayment on account upcoming payments. However, such a credit is possible only at the request of the taxpayer. Independently set off overpayment to the account of forthcoming payments, the tax inspectorate is not entitled.

The statement indicates the tax on which the overpayment occurred, the amount of the overpayment, as well as where it should be credited: to pay off arrears or upcoming payments.

If there is an error in the payment, it is advisable to attach this order and an extract from the bank. If the taxpayer made a mistake in calculating the tax and, this was the cause of the overpayment, then together with the application for offsetting or refund, it is necessary to submit a revised declaration.

Attention! Credit is possible only between taxes of one kind.

Federal tax can be credited only federal, regional - regional, etc. For example, income tax and VAT can be credited to each other (both taxes are federal). Transport tax with property tax (regional taxes) will also "fit" each other.

| ? | What is the time limit? |

| Within 10 working days. | ! |

The decision on offsetting overpaid tax against future payments must be made by the tax 10 working days. In this case, the moment of payment of the "necessary" tax will be the date of the decision on offset.

Another 5 days is given to the tax authorities in order to inform the taxpayer about his decision.

Attention! If the overpayment was formed before the arising of arrears on the same tax or in the same budget and completely covers the arrears, then the fines should not be charged. Since in such a situation there was no real underpayment to the budget. Such a conclusion was made by the Plenum of the Supreme Arbitration Court of the Russian Federation in Resolution No. 5 of February 28, 2001.

The taxpayer has the right to expect to return the overpayment if the following conditions are met:

- ✓ overpayment occurred in three-year period from the moment of excessive tax payment;

- ✓ no debt on taxes and penalties.

The form approved by the Order of the Federal Tax Service dated 03.03.2015 No. MMB-7-8 / [email protected]

The statement indicates the tax on which the overpayment occurred, the amount of the overpayment, as well as the details of the current account, where the overpayment should be returned.

If a positive decision is made, the amount is returned within a month, that is, no later than one month from the day the taxpayer submitted the application.

If this period is violated, for each day of the violation, starting from the next day after the expiration of the one-month period for returning the overpayment, the taxpayer is charged interest. They are calculated on the basis of the refinancing rate of the Bank of Russia, which was valid on the days of violation of the repayment period.

Attention! It is important to distinguish payments from, since the first tax authority must return you with by percent. As for overpaid taxes (penalties, fines), interest is charged on them only if the tax authority violates the deadline for returning the overpayment to the taxpayer.

The general scheme is as follows

Also, the taxpayer has the right in case of tax in case of refusal of inspection in the offset (return) or if the application does not respond to submit an application to court within three years from the moment of overpayment.

Attention! In case of tax, the taxpayer has the right to apply to the court without prior appeal to the inspectorate.

The right to a refund or credit of an overpayment is not indefinite. The application must be sent to the tax office within three years old from the date of payment of this amount

Attention! The Decree of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 17372/09 of April 13, 2010 noted that the moment when the taxpayer found out or should have known about the fact of overpayment of the tax should be determined taking into account the assessment of the totality of all the circumstances relevant to the case. for which the taxpayer allowed overpayment of the tax, its ability to correctly calculate the tax according to the initial tax return, changes in the current legislation during the tax period under consideration, and other x circumstances that may be recognized by the court as sufficient for the recognition of the period for tax refund non-omitted.

You can apply for a credit or return directly to the tax authority. At the same time, we recommend to have with you a copy of the application or its second copy. It is necessary that the tax authority officer responsible for receiving and registering incoming documents mark on it the date of receipt of the application.

Submission is also permitted. by mail. It is better to send it by a valuable letter with an attachment list.

It is very convenient to send an application to in electronic format via telecommunication channels. To send reports via the Internet, you can purchase an electronic digital signature at the Central Bank Accounting Center and use it for one year to submit reports to the Tax Authorities, Pension Fund (PFR), Social Insurance Fund (FSS), etc.