Blank land tax for legal entities. How to fill out and file a land tax return

How many declarations to fill and submit

The declaration must be handed over to the tax inspectorate at the location of the land plot clause 1, Article. 398 NK RF. If an organization has several sites on the territory of one municipality (one city of federal significance), then one declaration is submitted, but for each of them a separate section should be filled. 2 declarations.

If the organization has several sites in a federal city, then you can choose the tax inspectorate at the location of one of them and submit a declaration there for all the sites, notifying the other tax inspectors Letter of the Federal Tax Service of April 26, 2005 No. 21-4-04 / [email protected] .

If the organization owns several sites in different municipalities, then the number of declarations depends on the number of the Federal Tax Service Inspectorate, which control these territories 2.11:

if one IFTS is to submit one declaration, at that a separate section is filled for each of the sections. 2 declarations with the corresponding OKTMO code;

if different tax inspectorate - the declaration must be passed to each of them.

You can find the OKTMO code using the "Know OKTMO" service posted on the Federal Tax Service website (http://nalog.ru/rn77/service/oktmo/) FTS information.

Which sections of the declaration to fill

Any land tax return includes clause 1.2 of the Procedure for filling out the declaration:

Payable or reduction for the year, calculate the formula section 5, Art. 396 of the Tax Code, paragraphs. 7, 4 h. 1 tbsp. 2 of the Law "On Land Tax").

The organization has no rights to benefits.

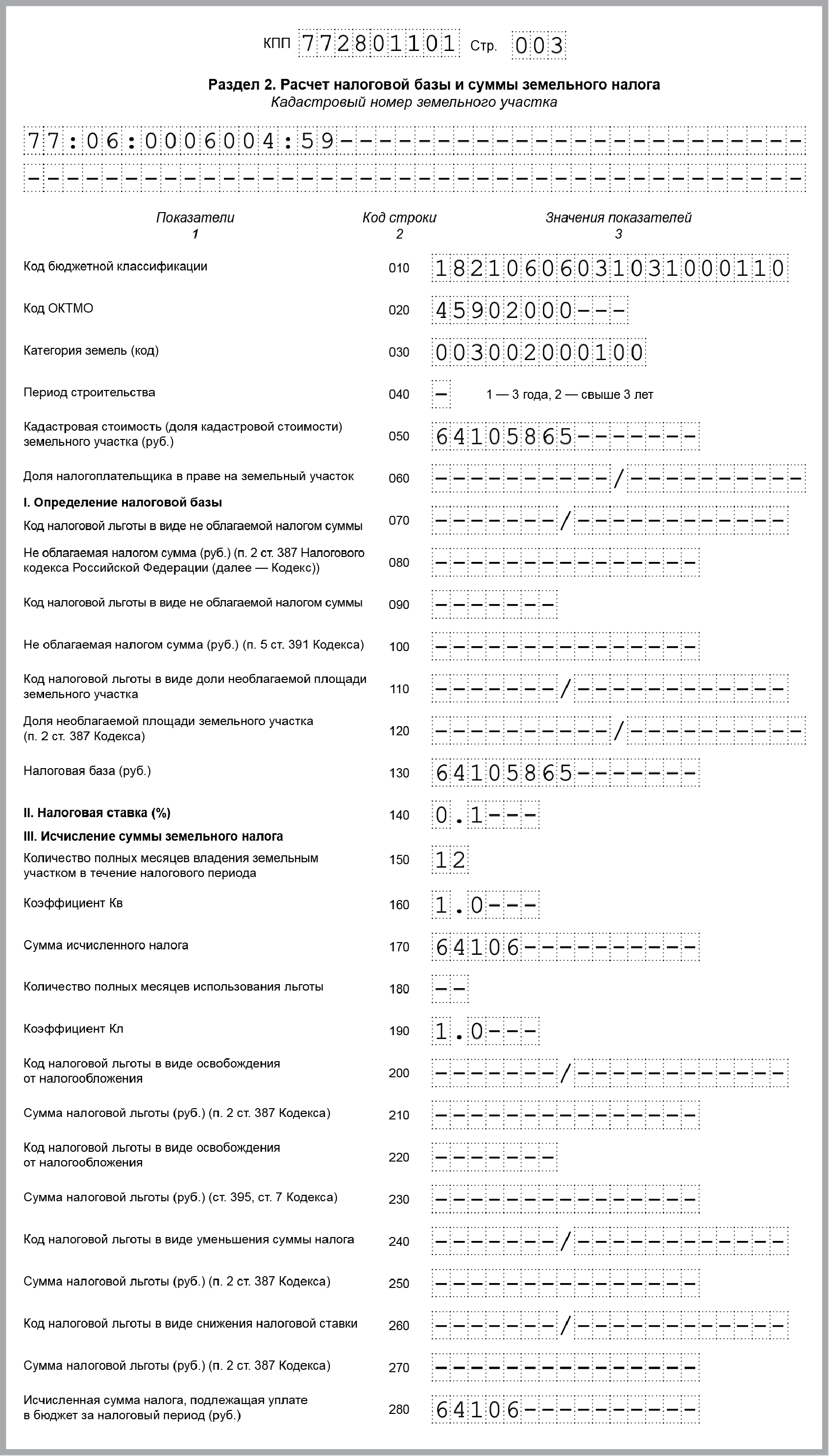

Calculation of land tax on the plot N 77: 06: 0006004: 59.

Advance payments for the first, second and third quarters - at 16,026 rubles. (64,105,865 rubles x 0.1% x 1/4).

The tax, calculated with allowance for benefits (line 280, section 2 of the declaration for this section), will be 64,106 rubles. (64,105,865 rubles x 0.1%).

Calculation of land tax on the plot N 77: 06: 0006004: 39.

No advance payments.

The tax calculated with allowance for benefits (line 280 section 2 of the declaration for this section) is equal to the tax without benefits (line 170 section 2. declaration for this section) - 72,471 rubles. (58,000,000 rubles x 1.5% x 0.0833).

The calculation of the total amount of tax payable to the budget.

Advance payments (lines 023, 025, 027, section 1 of the declaration) for I, II and III quarters - 16 026 rubles each. (64,105,865 rubles x 0.1% x 1/4).

The tax calculated on both plots (line 021, section 1 of the declaration) is 136,577 rubles. (64 106 rubles. + 72 471 rubles.).

The tax payable for the year (line 030 section. 1 of the declaration) - 88,499 rubles. (136 577 rubles. - (16 026 rubles. + 16 026 rubles. + 16 026 rubles.)).

It is a legal obligation for individuals and legal entities who own such type of property as a land plot.

Moreover, for the latter category of taxpayers, the obligatory condition is not only depositing money, but also filling out a special document - a tax return. About features of the correct design and filling of this document - further in the article.

The general list of entities subject to legislative obligation to pay land tax is listed in Art. 398 of the Tax Code of the Russian Federation. In accordance with this article, in this case are the owners of land located within the municipality or cities of federal significance.

They can fall into one of the following categories:

- (state, municipal or private ownership);

- individuals are citizens;

- individuals who are registered as individual entrepreneurs (PI);

However, they must own the land with the following rights:

- (in this case, land is provided only to citizens);

All entities that own land on one of the three rights listed above and do not have any, are obliged to pay this tax. However, another additional obligation is imposed on legal entities - the completion and submission of a special tax document, that is, a declaration.

All entities that own land on one of the three rights listed above and do not have any, are obliged to pay this tax. However, another additional obligation is imposed on legal entities - the completion and submission of a special tax document, that is, a declaration.

As for individual entrepreneurs, who until 2015 also had to submit a declaration, for them this duty was canceled after making certain amendments to the RF Tax Code.

Now these entities pay the tax calculated by the FTS bodies and displayed in the corresponding notification.

Deadlines for filling and delivery

Filling in and returning the declaration is a periodic obligation, which,  among other things, it has a clear time frame. The document is submitted once a year and contains information for the entire period. The declaration must be submitted no later than February 1 of that year, which follows the reporting year (that is, in 2016 it should have been submitted before February 1, 2017).

among other things, it has a clear time frame. The document is submitted once a year and contains information for the entire period. The declaration must be submitted no later than February 1 of that year, which follows the reporting year (that is, in 2016 it should have been submitted before February 1, 2017).

A slight extension of the term is possible only if the deadline for delivery falls on a non-working day (weekend or holiday).

In this case, the deadline is postponed to the next working day.

In case of violation of the deadlines for delivery of the document (or with complete disregard for this duty), a certain responsibility is established for the payer, namely, in the amount of:

- 5% of the amount of unpaid tax for each month of delay, but not less than 1000 rubles. and no more than 30% of this value - in relation to the organization (in accordance with article 119 of the Tax Code of the Russian Federation);

- from 300 to 500 rubles. - for an official who is responsible for the delivery of this document (this is established by Art. 15.5 of the Administrative Code of the Russian Federation).

As for the body for treatment, it is the territorial division of the Federal Tax Service of the region in which the specific land plot is located. It is worth considering that if there are several objects of real estate and they are located in different constituent entities of the Russian Federation, then several documents will be filled in and surrendered, for each of them.

In addition to meeting deadlines, correct completion of the document is also an important condition..

After all, if there are errors or inaccuracies in it, it will not be accepted by the Federal Tax Service officers, but will return to the payer to correct the defects. This, in turn, may lead to a violation of the deadlines and the imposition of a fine.

It has the established form and is approved by law, by order of the Federal Tax Service of Russia of 28.10.11 No. MMB-7-11 / [email protected] (hereinafter - the Order). Its volume is rather small, the document consists of the following parts:

- Title page. Here is detailed information about the company that is a tax payer.

- The first section "The amount of land tax payable to the budget." This section contains the amount of advance tax payments that were paid during the reporting period, as well as its total amount.

- The second section "Calculation of the tax base and the amount of land tax." Here, the algorithm for determining this value is described in more detail and the indicators required for the calculations are displayed.

In more detail the rules and features of filling in each of these sections will be given below.

You can get a form to fill in as in the territorial division of the Federal Tax Service, and on the Internet, on the official website of this body or on another third-party resource.

Over the past few years, no changes were made to the document itself, however, the adjustments could affect various codes and reference books that are used in its preparation. Therefore, all these points should be taken into account before filling in the declaration and, if necessary, recheck the data displayed there.

General rules for filling

All sections of the declaration must be completed in accordance with the requirements contained in the Order.

The most important of these include:

- The values of all cost indicators must be entered in full rubles. If, after calculations, the indicator turned out to be with kopecks, then it is rounded in accordance with the general arithmetic rules: if kopecks are less than 50, then in a smaller direction, otherwise - in a larger direction.

- All pages of the document are numbered. It begins with the title page and does not depend on the number of sections to be filled in, as well as their presence or absence. The page number is recorded in a special field from left to right in this form: 005 for the third page, 015 for the fifteenth, 105 for the one hundred and fifth.

- Correction of errors with the help of corrective means is not allowed. Also banned erasures, typos or clerks in the text, fatty strikethrough, the use of an eraser or proofreader. If changes are necessary, erroneous information should be crossed out with one thin line, after which the correct data should be indicated next to them, as well as the signature and surname of the person who made the record.

- When filling in the declaration, ink of the following colors can be used: black, blue, violet. Text can be handwritten or typed on a computer. All letters of text fields must be printed.

- Duplex printing of the form is not allowed. Each page should be printed on a separate sheet. It is also forbidden to fasten the sheets in ways that could harm the paper carrier (for example, to staple or staple the stapler).

- All fields are filled from left to right, starting with the first familiarity. Each field is intended to add only one indicator to it (except for fractions, which can occupy several fields). If any of the indicators is missing, then a dash is entered in the appropriate field.

In principle, these requirements are not unique - they are established for the majority of declarations and official documents that are submitted to state bodies.

However, their compliance is mandatory, because otherwise the adoption of the document may be refused.

The declaration can be submitted both in paper and electronic form using special telecommunication channels provided for in the RF Tax Code.

When a document is submitted in paper form, it is necessary to prepare two copies of it, since one will be handed over to the tax authority, and the second, with the appropriate note, will be returned to the payer. This can be done both personally and by mail or through a legal representative.

Entering data by sections

Each section of the declaration is intended to display certain information that is entered in accordance with legal requirements. Therefore it is worth considering the content of each section in more detail:

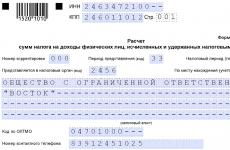

Title page

Here it is necessary to enter the following data:

- INN and KPP (in accordance with company documentation);

- the number of the adjustment (in the case of initial delivery, zero is put, if specified, 1, 2, 3, etc.);

- (its code);

- reporting year;

- the code of the department of the Federal Tax Service where the document is submitted;

- code of the type of economic activity according to OKVED;

- full company name;

- contact phone number;

- number of pages of the document.

Below, the representative of the payer puts his full name and signature, as well as the seal of the enterprise.

To confirm his authority, a special document must be provided (this may be a power of attorney or an order appointing a manager for the position).

First section

The following information is entered in the appropriate lines of this section:

- budget classification code;

- oKTMO code;

- the established amount of tax for the entire period, and for each quarter.

The accuracy of this information is also confirmed by the signature of the authorized person.

Second section

In this section, the calculation of the tax by way is displayed in more detail and it contains the following data:

- cadastral number put on;

- budget classification code again;

- and OKTMO code;

- construction period (if the work of this type is carried out on the site);

- cadastral value of land;

- the benefit code and the amount that is not taxable (if there are benefits);

- the size ;

- value;

- the duration of ownership of the site (indicated in the number of full months);

- calculated amount to be paid.

When filling out and calculating these sections, the payer should not have any difficulties, since the procedure for calculating the tax is simple, and all the fields of the declaration are described in sufficient detail.

In the case of some difficulties, it is worthwhile to use the data from the Order, which contains sufficiently detailed instructions for completing each section and field of the document.

Required Applications

The Order contains not only general rules for completing and filing a declaration, but also a list of certain annexes that the responsible person may need when filling it out.

These include:

- Appendix №1. Codes defining the tax period. In general cases, this period is the calendar year, but there is also an option when the company is liquidated.

- Appendix №2. Codes of reorganization forms and organization liquidation code. Each of these forms (mergers, divisions, etc.) has its own numerical value.

- Appendix №3. Land tax return tax codes. With the help of this application, a code is determined that reflects where exactly the declaration goes (according to the location of the lot, the payer's accounting, etc.).

- Appendix №4. Codes defining the method of submission of land tax returns to the tax authority. This may be paper or electronic media, personal delivery or mailing, etc.

- Appendix №5. Reference categories of land. For each of the categories stipulated in the legislation (industrial, water or forest fund, etc.) there is also a code.

- №6. Codes of tax benefits. If there are certain benefits, this is reflected in the declaration by the corresponding numerical value, depending on their nature and type.

These codes are not very many, so choosing the right and appropriate for a particular situation value will not be for the payer special work.

Features of the amended declaration

In the event that the declaration submitted to the tax authority contained any errors or inaccuracies in the tax calculation, which were discovered only after it was submitted, the taxpayer is obliged to prepare and submit a new sample document.

This is done through a revised declaration, which is filled in the same form and according to the same rules and requirements as the usual one, in the manner prescribed by Art. 81 of the Tax Code.

It is obligatory to provide it in the event that an error has led to  underpayment of tax to the budget. If the situation is the opposite (that is, more money has been paid), the right of choice remains with the payer (this means that he may not file it).

underpayment of tax to the budget. If the situation is the opposite (that is, more money has been paid), the right of choice remains with the payer (this means that he may not file it).

If the document was submitted before the deadline for filing the main declaration or until an error in the calculations was discovered by the FTS officers, no liability will be applied to the payer. In other cases, he will need to pay a penalty and penalty for each day of delay, provided for the late filing of the declaration.

In addition, the filing of “clarifications” usually threatens the company with increased attention from the tax authorities and may even lead to an unscheduled inspection (in the case of its delivery after the deadlines).

In accordance with the norms of current legislation, organizations and individual entrepreneurs who own land plots, a tax declaration for land tax must be provided to the FTS.

This document is filed with other documents - the declaration of the simplified taxation system or UTII. It should be noted that the land tax is charged only if the object is designed according to all relevant requirements and rules.

Tax return for land tax in 2017

Starting from the tax period of 2015, tax returns for land tax by individual entrepreneurs are not submitted.

The obligation to submit a land tax declaration is assigned only to legal entities.

In general, for individuals and individual entrepreneurs who are obliged to pay the land tax, now the tax authorities will even calculate the tax amount. This is stated in paragraph 3 of article 391 of the Tax Code of the Russian Federation.

The deadline for the payment of tax for individuals is no later than December 1 of the year following the expired tax period. Those. not later than December 1, 2017, it is necessary to pay land tax for 2016. And for 2017, individuals must pay land tax before December 1, 2018.

The amount of land tax for individual entrepreneurs and individuals will be indicated in the notification, which will come to the person at the place of registration. The inspectorate must send a tax notice no later than 30 days before the due date.

The following information will be indicated in the tax notice:

- the amount of tax payable;

- object of taxation;

- the tax base;

- tax payment term.

If the person, being the owner of the land plots, did not receive a notification one month before the deadline for paying the tax, the FTS of Russia recommends taking the initiative itself and contacting the inspectorate personally or through a trustee.

In such a case, the notice will be transferred to the individual (his legal or authorized representative) personally on receipt.

There is another way to get a tax notice for the payment of land tax. It can be transmitted electronically via telecommunication channels or through the personal account of the taxpayer.

Who pays land tax in 2017?

Taxpayers are organizations, individual entrepreneurs, individuals who have the right to own property, the right of permanent (perpetual) use or the right to lifelong inherited possession of land plots recognized as a taxable object in accordance with Art. 389 Tax Code.

What land plots are subject to taxation?

According to Article 389 of the Tax Code of the Russian Federation, land plots that are located within the municipality are subject to taxation, and land tax has been introduced by the regional authorities.

Not subject to tax:

- land plots that are not subject to sale and if they contain especially valuable objects of the cultural heritage of the peoples of the Russian Federation;

- land plots with objects included in the World Heritage List;

- land plots with historical and cultural reserves;

- land plots with archaeological heritage sites, reserve museums;

- land plots that are part of the common property of an apartment building.

Land tax is paid only by the owner of the land. Organizations, individual entrepreneurs do not pay land tax if the land is with them on the basis of:

- lease agreement;

- agreement of free urgent use.

Submission of land tax declaration in 2017

The tax return for land tax must be completed at the end of the year. In accordance with the statutory deadlines, it is transferred to the tax authorities.

The declaration is submitted to the tax office at the location of the land plot. If the organization owns several plots and they are located in different territories, each document is filled in separately and transferred to the appropriate tax authority.

Both the individual entrepreneur and his authorized representative can submit the declaration.

The 2017 land tax tax return is completed in two copies: one remains with the inspector, the second - with the organization.

The completed document can be sent by mail. It is necessary to send documents by a valuable letter (with indication of the inventory in the attachment). The deadline for filing the declaration will be the date of sending the letter.

The declaration can be sent by e-mail. To do this, you must complete the form posted on the website of the Federal Tax Service. Alternatively, you can order this service in a specialized company.

Deadline for filing your tax return in 2017

The land tax declaration must be sent to the Federal Tax Service Inspectorate before February 1 of the year following the expired tax year. For 2017, the declaration must be filed before 01.02.2018.

Rules for filling the land tax declaration

The basic rules for completing this document in 2017 are as follows:

- It is possible to fill in a document on paper or in electronic form.

- Only one value can be entered in the cells of the rows.

- Corrections to the declaration must be noted by the official.

- The declaration can be filled with a black or blue pen.

- In the absence of any value in the document lines put a dash.

- Each page of the declaration must be printed on a separate sheet.

- All pages must be numbered.

- The document cannot be stapled (stapled).

- Text should be written in printable characters only.

- Filling in the declaration, it is impossible to use corrective means.

Free download land tax declaration form 2017

Download the tax form for land tax in 2017 by the link below. The document is in Excel format.

Land tax calculation

The following innovation will facilitate the calculation of land tax. On the official website of the tax service posted a calculator that allows you to automatically calculate the amount of tax of any land or any real estate cadastral number.