What checks can be at un. Tax audit of IP: is it possible after business closure

A sole proprietor can quite easily stop their business. According to Art. 22.3 of Law No. 129-FZ of August 8, 2001, “On State Registration of Legal Entities and Individual Entrepreneurs”, it will be sufficient to submit to the tax inspectorate a statement, payment document on the payment of state duty and documents confirming the delivery of individual information to the FIU.

By submitting these documents, an individual will lose the status of an entrepreneur. However, the tax authorities have the right to conduct an on-site inspection of activities no longer conducted. Why? Let's see.

The fact is that an individual entrepreneur, even having lost his entrepreneurial status, is not exempt from paying taxes, which he had to pay during his activity. Article 44 of the Tax Code of the Russian Federation states that the obligation to pay taxes is terminated only after the transfer to the budget of all amounts due or in connection with death. Although there are exceptions, if the individual entrepreneur owes land, transport taxes or personal income tax, the heirs must pay these debts for it.

In addition, the PI is obliged to report for the period when he conducted the activity, to provide the tax return (letter of the Ministry of Finance of Russia No. 03-11-11 / 83 of 04/06/2011). And the businessman is obliged to keep documentation on business activity within four years. In this way, sP check after closinganyway take place.

The decision on the inspection is taken at the place of residence of the natural person on the basis of paragraph 2 of Art. 89 of the Tax Code of the Russian Federation. The letter of the Ministry of Finance of Russia No. 03-02-08 / 109 dated December 24, 2012 noted that the access of tax officials to housing individuals against their will is not allowed. So, if the former entrepreneur cannot provide the inspectors with premises, the event can be held at the tax inspectorate premises.

Documents requested by the inspection, in the form of certified copies, must be submitted within 10 days. If this is not done, then you will have to pay a fine - 200 rubles for each document that was not submitted. But even if the former businessman did not submit the documents to the tax office, the inspectors cannot come to his home without his consent. But even without his consent, they can:

- - make a request necessary for verification of documents;

- - call to testify any person who may know something about the activities of the IP;

- - to inspect any non-residential premises belonging to the former merchant;

- - attract experts;

- - carry out the seizure of documents and any items that are in non-residential premises of the individual entrepreneur;

- - request documents relating to the activities of individual entrepreneurs from other persons.

In all other aspects sP check after closing carried out according to established rules.

According to the Federal Law No. 127-ФЗ dated October 26, 2002 “On Insolvency (Bankruptcy)”, a former entrepreneur can avoid paying taxes and fines only if he is declared bankrupt. First, he will have to pay off the debt at the expense of his property, and then, if the value of the property is not enough, he is discharged from obligations related to his activities.

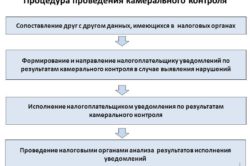

Cameral control ( Tax Code, Article 88) PI is held regularly as reports are filed with the tax authorities. SP prescription (notification) is not served. An entrepreneur may not know about it. In this article, we will look at how a desk audit is carried out on various types of taxation: USN, UTII, PSN and after closing.

Typically, the verification procedure lasts no more than 3 months from the date of submission of the documentation. The reasons for this are:

- delivery of the declaration and other reporting documentation;

- documents already available to the inspection body.

Features of the desk audit of individual entrepreneurs

Verification on the basis of the existing tax reporting may be carried out in the case when the declaration is not submitted. Upon detection of inconsistencies, errors, the inspector who inspects may request clarification and any documents necessary for the desk audit. Only the fact of detection of inaccuracies and contradictions is the basis for presenting such requirements to the entrepreneur. The exceptions are payers for whom benefits are provided, as well as those who have claimed the right to a tax refund (VAT return).

The IP should respond within 5 days after the delivery of the requirements. The PI can give explanations in writing, by phone or verbally, by visiting the inspection inspector in the tax office. For violation of the deadlines and failure to provide information (documents), the PI is held accountable. Upon detection of offenses, the examiner usually prepares an act of office audit, assesses taxes.

Cameral inspection of IP on the simplified taxation system, UTII, PSN, OCH of fundamental differences from the standard verification of this kind does not have and is the same for all entrepreneurs. In all cases, the basis of the same tasks, the implementation of which is carried out according to the Tax Code of the Russian Federation. First of all - this is the verification of reports submitted by the tax inspector to the PI. With proper documentation and timely delivery of its verification passes quickly and without any claims of the IP. What and when do businessmen pass on USN, UTII, PSN?

Cameral control of IP on the simplified tax system

The activity of IP at the simplified tax system is regulated by ch. 26.2 Tax Code. To apply the simplified taxation system, it is necessary to observe the requirements established by the law. Therefore, the tax inspector begins the procedure by checking the criteria. If it turns out that the inspected IP is improperly using the simplified taxation system, it will be charged additional unpaid taxes that relate to the DOS. Fines and late payments are added to them. It is noteworthy that such additional charges are applicable in similar situations with respect to all tax regimes.

Accounting at USN is not provided. Tax accounting is carried out on the basis of the accounting book of profits and expenses ( NK RF, Art. 346.24), which is conducted on paper or in electronic form. In the formation of the reporting of IP determines the object of taxes:

Based on the data in the account book, a declaration for the calendar year is completed. All duties of the payer of fees are defined by Art. 23 of the Tax Code. According to the law, the declarant must provide the tax authorities with a register of income and expenses on request:

- personally (through a representative);

- by mail (registered letter with attachment list);

- by email.

The tax inspector verifies the correctness of the reporting and the accuracy of the information presented in it. The essence of the audit itself is that the tax authorities check the conformity of the indicators of the declaration, the absence of contradictions in the information, the observance of the calculation of the tax base, the timeliness of tax payments.

At the tax object “profit minus expenses”, the costs (their validity, documentation), and counterparties fall under the check. If during the inspection by the inspector will be found errors, inconsistencies, other non-compliance with the norms established by law, the IP will be informed about this. For 5 days, the entrepreneur must, according to the requirements of the auditor, provide clarifications and make corrections.

Cameral check of SP on UTII

Accounting for UTII is minimal, since the amount of tax does not depend on the profits, and is carried out in an arbitrary form. An individual entrepreneur without a staff member, in addition to statistical reporting, leads and submits a declaration for verification every quarter (no later than the 20th day after the reporting quarter). Here he is obliged to reflect the taxes paid, typical for UTII.

When UTII is combined with other special regimes (USN, OSNO, etc.), the individual entrepreneur leads and reports to the tax authorities on each of them separately. Accordingly, during a desk audit, the inspector will check the submitted documentation on all modes (when combining different types of activities) or only the EBRD declaration, if only this mode applies.

Cameral check of SP on PSN

Under the patent system of taxation, the IP does not submit any declarations, but only keeps a book of accounting on expenses and income in paper or electronic form. It contains data on profit for the tax period, it has no expenditure part. The activity of the IP on PSN has its own specifics

| Patent | Features of the activity | Reporting without workers | Staff Reporting |

| To retail | Do not need a cash register; upon request any document is presented to the buyer upon payment |

A profit and cost account book is maintained; PI pays mandatory contributions to the FIU, MHIF |

PI annually until April 15 confirms the type of activity in the FSS; required: ledger, design form 4 FSS every quarter, the number of employees certificate 6-NDFL once a quarter; PI pays personal income tax and compulsory insurance premiums |

| For the provision of services | The client is given a must-filled strict reporting form. | As with retail | Same as retail |

If an individual entrepreneur is engaged not in one type of activity, but in several, then he needs to keep such an account book separately for each type. The account book is necessary for the inspector to check whether the payer has exceeded the 60 million p limit. by annual income. This is a prerequisite for those engaged in entrepreneurship on PSN. An accounting book is submitted upon request.

Cameral control after closing the SP

The tax service has the right to check the PI after closing in accordance with Russian legislation for 3 years. During this period, the PI, in turn, can, if necessary, check and return overpaid taxes. Entrepreneur by law must be 4 years ( NK RF, Art. 23, item 1) keep information:

- on tax and accounting;

- other documentation on the part of the calculation, payment of taxes;

- documents about profit and expenses incurred.

After closing, the off-site control is carried out only in relation to an individual who was registered as an IP. It is carried out by the inspection inspector at the tax office and at the place of residence. The duration of the audit is 3 months from the date of submission of reports to the tax authorities. Get under control:

- first of all, a tax return;

- iP documents on business activities;

- accounting reports.

During the off-site control, the tax inspector initially checks the declaration for inaccuracies, errors, and absence of contradictions. In the attention of the inspector gets the correctness of calculations of taxes paid, timeliness of payments of IP in extra-budgetary funds. If during the audit it turns out that the calculation of the tax is incorrect or other violations are found, the inspector can ask for clarification from the already closed IP or charge additional tax. After 3 years for the identified offenses, the SP is not brought to justice ( NK RF, Art. 113).

Example # 1. Cameral check of SP when combining the USN and PSN

SP rented non-residential premises. In his activities, the entrepreneur used the simplified taxation system, and for certain real estate objects - the SPE. Due to non-payment, he lost the right to use PSN. Therefore, he now has to pay taxes for the “patent” activity in accordance with the general regime. Accordingly, the tax authorities should be provided with reports on a simplified and general tax. In this case, there will be no claims against the payer in the office audit.

If the individual entrepreneur, for example, ranked everything (including profits from “patent” activities) to the simplified taxation system and submitted reports only on the simplified tax system, then it would most likely be presented with a desk audit. In such cases, the examiner may charge the individual income tax during the period of validity of the lost patent.

Example # 2. The timing of the on-site verification of IP

The declarant has filed a tax return with the tax authorities 26.03.2016. The tax inspector conducted a desk audit, during which he compiled and sent to the payer a request for documents. The sent request is dated 06/19/2016. SP received these requirements 06/20/2016. Since the requirement the inspector put in the statutory period (3 months), the payer of fees is obliged to respond to it and submit the necessary documents to the verifier.

Answers to current questions

Question number 1: What are the penalties for not submitting documents in response to the requirements of the inspection inspector?

The violator is fined in the amount of 200 rubles. for each document that was not submitted, if there were no signs of offenses ( clause 1, Article 126 of the Tax Code of the Russian Federation). Administrative responsibility is also provided for ( art. 15.6 Code of Administrative Offenses).

Question number 2: Is it possible to cancel the closing of the IP and change the address to avoid the cameral check?

No methods like those described will help to exclude off-site control. All tax returns submitted to the tax check.

Question number 3: Can I submit a revised declaration after drawing up the inspection report?

After finding errors, inconsistencies, contradictions, etc., the declarant is obliged to make corrections and corrections, and then submit to the verifier an updated version. Also, the payer has the right to make the necessary changes to the declaration and submit it with clarifications. If such a declaration is filed after the deadline, this is not a violation.

Question number 4: Are the results of the check (statement) emailed?

Not. A drawn-up inspection report on the violation is handed over personally to the payer (or his representative) signed by the recipient (or against a receipt with the representative), and can also be delivered by mail.

Question number 5: How many times is a desk audit conducted at UTII?

Cameral control in all tax regimes is carried out on the basis of submitted reports. This means that as soon as the declaration (reporting) is handed over, it will be checked immediately for 3 months.

Question number 6: Are tax authorities obliged to warn about the approach of the deadline for delivery of the declaration (reporting)?

No, the tax authorities should not warn in this case. Timely return the declaration (other statements) - the duty of the payer of fees.

Question number 7: Do inspection bodies report detected errors if an inspection report is made?

During the off-site inspection, the inspection inspector is obliged to notify about the detected errors, inconsistencies to the entrepreneur before drawing up the verification report.

08 Apr 201111 Apr 2011

Tax audit is always an unpleasant event.Hello! The search engine did not find the desired topic. Tell me, please, can they check IP during the first 3 years, there seems to be some sort of law. if you can give a link to the law. and if you shouldn't check it out, then how is this in practice? and if you came, how to behave? Thank you all in advance!

For reference: if your documents (accounting) are serviced by a third-party organization, they will not be able to remove them when checking them, the more chances to put in order the missing “elements” to date and double-check the presence of all components. A tax audit will be reduced to the pure formality of the inspection of employees and the execution of relevant documents on them, together with registration documents (copies) of the individual entrepreneur himself.

According to the first part of Article 87 of the Tax Code of the Russian Federation, only three calendar years of taxpayer activity immediately preceding the year of the inspection can be covered by a tax audit.

Short. Usually, a routine check of an IP occurs 3 years after registration. They may conduct a field audit, for example, if there is an error in the report. You can just "not very well" get a spot check. And can arrange a test on learning "well-wishers."

What was meant by the "hype" of the previous "speaker" did not quite understand.

12 Apr 2011

12 Apr 2011

thank! I SP on UTII. What can I check? please tell me! What documents do I need to pay attention to first? so they were fine. and yet, how to know that there was a tip "well-wishers"

Usually, those who are at UTII (without employees) check only the correctness of tax returns and the transfer of taxes. But this is my personal experience.

What are you doing? What activity?

You can find out about the "well-wishers" tip only by the appearance of inspectors on the threshold or they will notify you about the check by letter.

13 Apr 2011

Hello! Tell me, please, what should I pay attention to? What can check in the first place? I have just taken shape, the SP on the simplified tax system is 6%, I rent a small area for receiving orders, I go there twice a week, the rest of the time at home. Activity - PC related services. I work without cash, with BSO. Cash calculation.

The question of whether the tax inspectors can check the IP after closing is given to both former entrepreneurs and businessmen who are only planning to close their business. It would seem that after the PI is considered to be officially closed, and commercial activities are terminated, the tax inspectorate can not have any claims against an individual. In practice, everything turns out to be quite different, so every entrepreneur needs to figure out how the state can check the SP after the official closure.

Note!!! The tax inspectorate is entitled to inspect the individual entrepreneur even after he has completed his business activities. This right is governed by the laws of the Russian Federation and cannot be changed.

Existing firms check on the basis of data from the state register, information on commercial activities remains in the database even before the start of liquidation or reorganization of the IP. But non-existent enterprises, the tax inspectorate can check on the basis of general tax information - every owner of an individual entrepreneur is an individual, therefore, the tax inspectorate is entitled to the taxpayer identification code. Even such information can become the basis to check the company after closing.

Within three years after the end of the operation of an IP, the following types of audit may be conducted:

- tax;

- cameral

Article 113 of the Tax Code states that an offense detected three years after the closure of the SP cannot have legal force, such crimes are annulled under state law. Any verification after the closure of an individual enterprise is carried out only on the basis of state standards and requirements.

In the audit of the existing and liquidated enterprises there are significant differences. An offense in a functioning business can be considered only by an arbitration court in turn. And cases of offenses of a closed IP are considered exclusively in the general courtroom and have a completely different algorithm of action.

Do not forget about the rights of the entrepreneur after the closure of the business, any individual can submit relevant documents to check or return overpaid taxes during the operation of the enterprise! Articles 80 and 81 of the Tax Code guarantee to every entrepreneur such a right for three years from the moment of the closure of the IP.

If you decide to check the overpayment of taxes after closing your own business, and in the case of identification, to return your money, then you will need to go through a desk audit. This audit can be carried out on the basis of the following papers:

- settlement documents;

- tax returns;

- papers confirming the economic activities of the taxpayer.

The tax inspectorate may carry out the procedure only at the place of registration of the individual, that is, in the department in which the taxpayer received a certificate of state registration. The supreme governing bodies should not be aware of all the desk audits being conducted; the operation is carried out within three months after the submission of all necessary documents. The declaration of calculations is, in this case, the main and most important document, is the basis for the audit of the tax status.

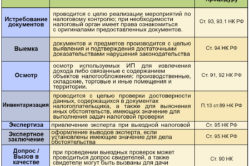

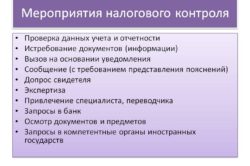

During a desk audit, employees of fiscal government agencies perform the following manipulations:

- checking the correctness of calculations of all types of taxes that the former entrepreneur paid;

- comparison of indicators of various reports and reports in order to identify errors takes into account oversights of one and the other side of tax relations.

Note!!! The tax inspectorate conducts cameral audit exclusively for individuals who had an individual enterprise. Legal entities at the closure of their business are deprived of such an opportunity!

In preparing for the audit, collect all documents that were related to your commercial activities. It is best to submit the originals of the papers, as copies are often left for further consideration, so you run the risk of delaying the procedure for verifying your tax payments.

Legislative aspects for this type of inspection is Article 88 of the Tax Code of the Russian Federation. Cases of fraud are strictly punished by law, it is not necessary to falsify the closure of your business, in order to register the certificate of an individual entrepreneur again. Tax debts are quickly and accurately detected, so you will not be able to avoid paying taxes.

- Control of cameral plan

- Exit check

- Possible test results

- Additionally

After the end of entrepreneurial activity, many businessmen will have to go through checks at the closing of the IP. Moreover, such a system is not mandatory, but still exists in some cases. Any entrepreneur expects a similar raid during the first 3 years since the official closure of the IP. It is worth remembering that with the termination of a legal entity is removed from the register as an individual entrepreneur, but it will remain in the database as an individual taxpayer. If during a thorough inspection will be found any errors, then the former entrepreneur may be held accountable. So you need to take these measures seriously.

When a check is expected when the SP is liquidated, the former entrepreneur should be notified by the services in advance, the main documents to be checked at this time should be indicated in the check warning. It is worth remembering that the same documentation can not be thoroughly checked twice a year. If for some reason the entrepreneur cannot attend the inspection, he has the right to postpone it to a date more convenient for him. There are various types of checks that need to be sorted out. For example, what is the office audit for when closing the PI?

Control of cameral plan

This is a regular type of inspection, intended for the secondary control of all reporting documentation of entrepreneurs. The district inspector personally monitors the timely delivery of all important reporting documentation. His competence includes the following actions:

- checking the correctness of the calculations made, filling in all the necessary documents;

- control of the reliability of the data provided for reporting;

- if during these actions no tangible violations are found, then the entrepreneur will not even be notified of the passage of this measure;

- in the event of any shortcomings on the part of the taxpayer, the corresponding notification is sent, after which clear deadlines are set for correcting all these errors.

Back to table of contents

Exit check

In case of revealing some shortcomings, for example, submission of unreliable data, untimely submission of reports, this type of verification can be appointed.

Representatives of the tax service immediately leave for a registered enterprise in order to conduct a forced inspection. The duration of such a measure is several months. At this time, the businessman is obliged to provide the tax authorities a separate office for work.

Representatives of the tax service immediately leave for a registered enterprise in order to conduct a forced inspection. The duration of such a measure is several months. At this time, the businessman is obliged to provide the tax authorities a separate office for work.

In the absence of the necessary office space, such a control measure is carried out at the premises of the Federal Tax Service. The duration of this administrative measure can be as long as six months with the following violations:

- in the presence of violations that require a secondary inspection;

- SP violated deadlines for quarterly reporting;

- some force majeure situations have arisen (ignition of an enterprise, etc.).

Back to table of contents

Possible test results

When the tax audit is completed at the time of closing the IP, a confirming act is issued in two copies. In this important document in detail should be reflected all reliable data on the order of passing, on the results obtained, all revealed violations and shortcomings should also be spelled out here. The prescription form must specify the procedure for their elimination.

The entrepreneur is given 2 weeks for a possible appeal of the contents of this confirming act. All arising objections are also described in the act itself, they are transmitted to service representatives.

With a clean accounting, timely submission of reports and payment of taxes in full, the owner of the enterprises will have to go through audits of the office plan. This entire system of inspections is of a regular nature, so all businessmen should conduct business more closely, not forgetting about timely payment of all obligatory payments.

With a clean accounting, timely submission of reports and payment of taxes in full, the owner of the enterprises will have to go through audits of the office plan. This entire system of inspections is of a regular nature, so all businessmen should conduct business more closely, not forgetting about timely payment of all obligatory payments.

In case of violation of the current federal legislation, failure to provide mandatory tax reporting, the IP should expect careful monitoring of its financial activities, when tax officials literally settle in his office for 2 months. With such a check, the punishment of the violator is sure to overtake, so you should not leave all cases without control.

Anyone who wants to liquidate his enterprise must be ready for liquidation desk verification, it is obligatory. If everything is in order, then it will pass so that the entrepreneur himself will not even notice it. Only after passing through these stages, the entrepreneur is removed from the registry, he is no longer listed as a legal entity.

Tax services just do not let those who are in their sight. Therefore, you should not relax after exiting the registry, it is better to prepare all the documents required for verification.

Such inspections of closed IPs are conducted not so often, those businessmen whose activities cause a lot of controversial issues or some people who are just so selected fall under suspicion of tax officials. But the likelihood of such raids is not excluded, therefore all reporting documentation must be maintained for at least 3 years after the official closure of the SP. Saved documents can serve as an excellent argument to the tax service and proof of their own right, so you should not hurry to throw them away.

Also, when submitting documents for the closure of an IP, all taxes must be paid up to the immediate closing moment, when a debt is detected, even if it is of minimal size, it will not be allowed to close. All mandatory payments to the Pension Fund must be made, with the exception of only enterprises with zero reporting. Only on recognition of the company as an official bankrupt entrepreneur will be exempt from all necessary payments to the budget. In order to make sure that there are no debts on compulsory pension payments, you can contact the Pension Fund for a supporting certificate. The tax service will continue to file a similar request, it is better to do so in advance, to prevent possible problems in the process of closing the PI.

If these requirements are not complied with, when resisting the inspection, the tax authorities are entitled to impose a fine on the person being inspected. Even if the entrepreneur will be categorically against this check, he will refuse to provide the necessary reporting documents, the tax authorities do not have the right to check them against their will.