Receive tax notices electronically. What to do if a tax notice arrives

What taxes are included in the single tax notice

The Tax Code of the Russian Federation until 01/01/2015 (until the entry into force of Law No. 52-FZ of April 2, 2014) provides for a notification procedure for the payment of property taxes for individuals. If until 2012 a separate notice came for each type of property, it decided to save on paper with the FTS and now sends a single tax notice for payment to individuals - the owners of the property registered for them:

A new single notice with contains a single term for the payment of property tax, transport, land tax - until October 1 (earlier - before November 1, and from January 01, 2016 - the deadline for payment is changed again - shifted to December 1 (Law of 23.11.2015 320-ФЗ, effective from 01.01.2016) of the next year, which means that:

Before sending a notice, tax authorities are obliged to calculate every tax and (as prescribed by paragraph 2 of article 52 of the Tax Code of the Russian Federation) no later than 30 days before the due date, send a notice to the taxpayer about the payment of property taxes.

The notification must include: the amount of tax, the calculation of the tax base, the deadline for payment of tax. For the convenience of the taxpayer, they put an already completed receipt into this envelope.

All this is due to the fact that our tax authorities are not very punctual, but they differ in that they can send a notice to pay a tax to a deceased person or a car that has been sold for a long time, or demands to pay taxes over the past 10 years.

Previous tax recalculation

Since 2010, it has become “fashionable” among the tax authorities of many regions to recalculate taxes already paid at new rates (ie, tax rates approved in subsequent years) and to illegally require additional taxes for previous years. This is what is called, the obvious cases where the tax is not necessary to pay, but there are more complex (and, unfortunately, also illegal) cases when the tax authorities (using the confidence of citizens and the fact that the Tax Code of the Russian Federation is written in Russian letters, but to understand it sometimes the content is extremely difficult even for specialists) they try to fill the budgets of various levels by any means.

It should be noted here that (for example) the Law "On the tax on property of individuals" provided for the possibility of tax recalculation, but only if:

from the BTI or the traffic police in the tax inspectorate received erroneous information;

information about the value of the property came from the BTI or the traffic police to the tax inspectorate with a delay (information must be received by the tax authorities each year before March 1 of the year for which tax will subsequently be charged);

in calculating the tax, an arithmetic (technical) error was made.

12/22/2016 FTS clarified the following (Information of the FTS of Russia dated 12.22.2016 "On recalculation of property taxes"):

Individuals can send an appeal on the recalculation of property taxes (land tax, transport tax, property tax) to the tax inspectorate, if in the 2015 tax notice:

- contains irrelevant information affecting the amount of property taxes. Eg

- tax benefits are not taken into account. (For example, the taxpayer has not previously applied to the tax office for the use of the tax benefit.)

If there are grounds for recalculating taxes, then the tax inspectorate:

- will reset and recalculate the previously accrued amount of tax and penalties;

- generate a new tax notice (if the tax exceeds 100 rubles) indicating the new tax deadline and place it in the "Personal Account of the taxpayer". If the taxpayer is not connected to the "Personal Account", then a new tax notice will be sent to him by mail.

The Federal Tax Service of Russia draws attention to the fact that it is also possible to send a request for recalculation of property taxes through the services of the “Personal Account of the Taxpayer” or “Contact the Federal Tax Service of Russia”.

credit can be credited or refunded only if no more than three years have passed since the date of the disputed tax payment (clause 7 of Article 78 of the Tax Code);

A more morally sustainable tax authority should send in the usual form - a notice sent by mail about the payment of tax, if such persons did not receive electronic notification and payment documents before September 1.

Everybody is interested in whether it is necessary to worry, to waste time on ascertaining, standing in queues in order to ascertain the reasons why the notification for the payment of tax did not come?

As mentioned above - until the notification of tax payment has come, there is no cause for concern, because the duty to pay tax on property, transport and land tax has not come - it is written in black and white in article 57 of the Tax Code of the Russian Federation.

But if you carefully study the Tax Code of the Russian Federation, you can learn more nuances:

- If the tax authority missed the deadline for sending the tax payment notice

Of these nuances almost out of the blue, many people had a lot of trouble. To avoid trouble, you can contact us for professional help.

Practice shows that the earlier a person turns to professionals, the less effort must be made to solve his problems, and problems are easier to solve.

The article was written and posted on October 17, 2011. Updated - 11.03.2012, 10/17/2012, 03/05/2013, 04/04/2014, 11/21/2015, 07/22/2016, 08.26.2016, 12.26.2016.

ATTENTION!

Author: lawyer and tax consultant Alexander Shmelev © 2001 - 2017

Useful links on the topic "What to do if a single tax notice for the payment of transport, land, property tax has not come"

During a tax audit or because of questions about the payment of taxes or fees, the tax inspectorate has the right to demand a verbal explanation from the taxpayer and ask him to visit the tax inspectorate at a certain time. How does the taxpayer know that they want to talk to him orally? You will receive a notice about the taxpayer’s call for clarification.

The reasons for calling the inspection may be different:

- If the tax audit revealed errors or discrepancies in the information provided by the taxpayer and the information held by the tax inspectorate. The need for a call will depend on the complexity of the situation and the number of questions made mistakes;

- The taxpayer may receive a tax claim for clarification on issues related to the implementation of the realities of the law;

- The taxpayer may be called to the tax office for delivery or to familiarize with various documents on the tax audit being conducted. This may be a decision that the tax audit period will be increased, the audit will be terminated, suspended, expert examinations appointed, the need to provide additional documents, etc.

Tax call for explanations

The tax notice is sent in accordance with the form given in Appendix No. 2 to the Order of the Federal Tax Service of Russia No. MMB-7-2 / 189 dated May 8, 2015. The full name of the company, full name of the entrepreneur or natural person is indicated in the document header.

The main part of the notification contains the following information:

- date of completion;

- name of the tax authority;

- where they call to the tax office for explanations: the exact address, with the number of the room;

- visit time: days and hours of reception;

- indication of the reason for which the taxpayer is called to the inspection;

- Name, signature of the inspection officer;

- contact number;

- date, signature, full name of the taxpayer, confirming receipt of the notice within the specified period (if the notice is served on paper).

A taxpayer’s call for clarification can be sent by inspectorate by registered mail, transferred to a company or individual entrepreneur (as well as to a legal or authorized representative of an organization or an individual entrepreneur) directly against a receipt, sent electronically through an electronic document operator.

If an organization or an entrepreneur is required to submit tax reports electronically, they should also receive a tax call to provide explanations electronically (this applies to the largest taxpayers, employers with an average staffing number of more than 100 people, etc.). Within six working days from the date the tax inspectorate sent the taxpayer call for clarification, the taxpayer must send a confirmation of receipt of the notice (for example, a receipt for receiving this notice).

If the notification was sent by mail, then it is sent to the address of the location of the company, which is listed in the register. If the recipient is an individual entrepreneur, the notification of the call to the taxpayer is sent to the address of the place of residence of the individual entrepreneur or the address provided to them for sending documents contained in the Register. The date of receipt of the notification sent by mail is considered to be the sixth business day from the day the registered letter was sent.

Letter of tax demanding clarification

Please note that the tax inspectorate has the right to call you for an oral discussion of issues or require you to provide written explanations on the issue of interest. If you received a notice of the submission of explanations (form on KND 1165050 , annex No. 1 to the Order of the Federal Tax Service of Russia No. MMB-7-2 / 189 dated May 8, 2015), then within five working days it is necessary to answer the inspection questions in writing. The form on which explanations are to be drawn up is not legally approved, therefore it is possible to submit explanations in free form. The entrepreneur has the right to attach documents confirming the authenticity of the information presented to the written explanations.

By the end of 2017, many citizens will face a situation when a tax notification arrived at their address or in their personal account on the website of the Federal Tax Service of Russia. What to do with this document? How to pay the amount of land / transport / property tax calculated by the inspectorate, as well as the personal income tax that is not held by the tax agent? About this - in our consultation.

Form

So, the tax notice has come. What to do with it? If this is a document on paper, then first of all, you should make sure that these are not tricks of fraudsters, but really the so-called consolidated tax notification from the IFTS. His hat looks like this:

The appearance of this document is fixed by the order of the Federal Tax Service of Russia of September 07, 2016 No. MMB-7-11 / 477. This form according to KND has an index of 1165025. It was put into operation relatively recently - from April 01, 2017.

It is somewhat simpler when tax notices arrive in the payer's personal account on the website of the Federal Tax Service of Russia www.nalog.ru. Here you can be sure of the authenticity of the document.

Analysis

If a tax notice has arrived, it can immediately include 4 tax liabilities:

- on vehicles;

- to the ground;

- on the property of an individual;

- on personal income tax, which the tax agent (employer, etc.) could not withhold earlier.

However, the tax inspectorate will include in the notification only those parts for which the payer exists or has a tax obligation to the budget. Therefore, it can come both in extended and in reduced form. The principle is this: there is no object - there is no tax.

A consolidated tax notice in 2017 can come not only for 2016, but also for previous tax periods (no more than 3 years ago, not counting the current year). This happens in the case of recalculation of taxes.

By law, a consolidated tax notice automatically generates a special computer program of the tax authorities. But this does not guarantee that there is no error in the notification.

Therefore, when the tax notice arrived, we strongly advise you to immediately examine in this document:

- all the source data that your tax data provides;

- correctness of all calculations.

Many naturally ask the question: where should the tax notice go? As a general rule, it is sent to the address of the registration of an individual according to the passport.

Sometimes it happens that the tax notice is later than the due date. How to act in this case, we wrote in the material "".

Payment

After forming the notification, the inspectorate immediately uploads it electronically to the personal account of the physical person in the section “Tax payer’s documents”.

Please note that after uploading to your personal account, a consolidated tax notice is considered to be delivered. That is - there is a duty to transfer to the treasury one or another tax.

It is important that the unloading of the notice occurs along with payment receipts for the relevant taxes. Therefore, the payment of taxes on the tax notice should not cause any particular difficulties.

You can pay in 3 ways:

- Directly through a personal account.

- Using the site service FTS "Pay taxes".

- Through the bank, pre-printed bills.

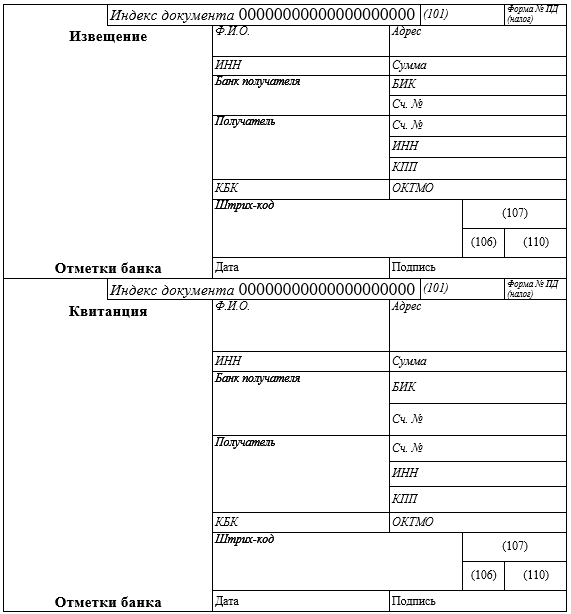

Upon receipt of a paper-based notification, the inspection also applies the necessary receipts to it. In this case, payment by tax notice is possible through a banking institution.

After making the payment, it is not necessary to confirm the payment of taxes according to the notification. True, payment confirmation is better to save.

If you find an error, please highlight a piece of text and click Ctrl + Enter.