Sample Filling a Land Declaration

Land tax falls on the shoulders of both ordinary citizens and enterprises and entrepreneurs. However, not every individual and even the organization is obliged to pay this tax!

And it's not just about the availability of benefits: not all lands are subject to taxation. Moreover, even those lands that are owned and owned by an organization or an individual can be exempted from tax on land for those controlling them. How? That is what this article will be about.

Dear readers! The article tells about typical ways of solving legal issues, but each case is individual. If you want to know how solve exactly your problem - contact the consultant:

(Moscow)

(St. Petersburg)

(Regions)

It is fast and is free!

Land tax: who pays?

Payers This tax is considered:

- ordinary citizens;

- entrepreneurs;

- legal entities.

On these persons given duty assignedif at the same time:

- the land that they own belongs to Article 389 of the Tax Code of the Russian Federation (hereinafter referred to as the Code) to taxable objects;

- they own land, as property, on the basis of perpetual use, or as a result of life tenure with inheritance.

And still not every taxpayer must pay land tax:

And still not every taxpayer must pay land tax:

- clause 5 of Article 391 of the Code stipulates that the tax base can be reduced by 10 thousand rubles, which are recognized as a kind of deduction and are not taxed. This right extends to land that is in perpetual use, owned, or inherited for life, but only on condition that the land belongs to:

- Hero of the USSR, the Russian Federation;

- disabled person of the 1st or 2nd group;

- disabled since childhood, and other citizens who are named in Article 391 of the Code.

In this case, local regulations may provide additional tax incentives for land tax;

- entrepreneurs can also use the exemption in the form of non-taxable 10 thousand rubles if they belong to one of the types of exempted persons specified in paragraph 5 of Article 391 of the Code. Moreover, they can use this privilege on land that is involved in business activities;

- in addition, Article 395 of the Code also provides for exemption from land tax, but in this case organizations are included in the list of beneficiaries.

To confirm the right to a benefit, you need to submit title documents and an application to the tax structure where the land is located.

What land does not belong to the object of taxation?

In Article 389 of the Code, in paragraph 2, there is a list of lands that not included in the calculation land tax:

All other lands are taxed.

If you have not registered the organization yet, then easiest do it with the help of online services that will help you create all the necessary documents for free: If you already have an organization and you are thinking about how to simplify and automate accounting and reporting, then the following online services will come to the rescue, which will completely replace the accountant in your company and save a lot of money and time. All statements are generated automatically, signed by electronic signature and sent automatically online. It is ideally suited for IP or LLC on USN, UTII, PSN, TS, OSNO.

Everything happens in a few clicks, without queues and stresses. Try it and you will be surprisedas it became simple!

Land tax: rates, tax base, calculation

Land tax - local tax.

But tax rates, approved by local authorities, can not be higher than those established by the Code:

- 0.3%. The rate applies to land:

- agricultural destination or part of the agricultural use zones;

- located under residential objects;

- purchased for housing;

- employed under housing and public utilities infrastructure;

- purchased or received for the organization of the dacha or personal subsidiary farm, for horticulture, horticulture or animal husbandry;

- limited in circulation due to the location of objects related to the satisfaction of defense or customs needs;

- 1.5% - for other lands.

Local authorities have the right to establish differentiated rates, based primarily on the categories of land, which are divided into:- agricultural land;

- territories of settlements;

- plots from the forest fund;

- reserve land;

- industrial areas;

- land occupied by objects of water fund;

- territories and objects subject to special protection.

The tax base is property cadastral valuewhich is recognized as taxable according to Article 389 of the Code. The base for each site is determined separately; organizations themselves, and for citizens (including entrepreneurs) this calculation is made by the tax authority.

For citizens tax is calculated for the year. But organizations the calculation is made quarterly (without a cumulative total) as a product of the tax base and базы rate. At the same time for the year, the tax is considered as the product of the full rate and the tax base, from which the advance payments paid are deducted.

Who submits the declaration?

Declaration is passed only legal entitieswhich are recognized as land tax payers. In this case, they report only 1 time - at the end of the year and not later than February 01 next year. Tax return for rent at the location of the landfor which the tax is calculated.

Declaration is passed only legal entitieswhich are recognized as land tax payers. In this case, they report only 1 time - at the end of the year and not later than February 01 next year. Tax return for rent at the location of the landfor which the tax is calculated.

Declaration form approved by the Federal Tax Service of Russia by Order No. MMV-7-11 / [email protected] from 11/28/11 A document is drawn up, if on paper, in duplicate, one of which remains in the tax authority, and the second is in the hands of the taxpayer.

If the declaration not delivered on time or not surrendered at all, then the penalty:

- for the organization will be charged at the rate of 5% of the amount of tax indicated in the declaration and not paid within the period established by the tax law, for each incomplete or full month, but not more than 30% of this amount and not less than 1,000 rubles RF);

- for a due person - in the amount of 300 - 500 rubles (Art. 15.5 of the Administrative Code of the Russian Federation).

But it is not enough just to file a declaration in time - it must also be correctly filled out!

General provisions for filling out the declaration

The declaration consists of a title page and 2 sections. It is issued for the tax period - a year. All its cost indicators are indicated in whole rubles, and values less than 50 kopecks. not taken into account.

Filling in the fields with the text is carried out in capital block letters. In addition, all fields in the declaration begin to fill in from left to right, either with a pen or using a software tool.

If the organization has several plots on the territory of one municipality, Section 2 is compiled for each such object separately. If all these plots are located in different municipalities, but under the jurisdiction of one tax structure, then a single declaration is submitted with filling out all sections for the corresponding OKTMO code.

Even if the organization fully or partially released from the land tax, it still remains the obligation to submit the land declaration.

All codes for the declaration are given in the order approving the form of the report. As for the name of the legal entity, TIN and KPP, they are indicated on the basis of the specified person.

Everything advance payments are calculated as:

¼ rates x Cadastral value

Moreover, if the local regulatory act does not provide for accounting periods, then it is not necessary to make advance payments, and there should be dashes in the declarations in these lines. Otherwise, for the 1st, 2nd and 3rd quarters the calculated amount of the advance is put down. But for the year the payment is considered as the difference between the tax calculated on the basis of the cadastral value of the January 1 tax period multiplied by the full rate, and the advance payments made. If this value is negative, then a dash will appear in the field.

As regards the completion of Section 2 of the declaration, this procedure is described in detail in order No. 28 of March 2011 No. MMP-7-11 / [email protected]

On the payment of land tax, see the following video:

If a legal entity owns land ownership, it is obliged to pay land tax and submit a land tax return on time. It is important not to miss the deadline for the delivery of the land tax declaration for 2016, as the company will be fined for being late.

Who is obliged to submit a land tax return, where to pay the tax and to whom to submit the declaration. And also, in what time it is necessary to submit a land tax declaration in 2017, the form of the declaration and the sample of its filling - all this you will find below.

Land Tax Declaration for 2016

The form or form of the tax return for land tax for 2016 and the procedure for filling are approved by the order of the Federal Tax Service of Russia of 28.10.11 No. ММВ-7-11 / [email protected] Form code according to the tax document qualifier 1153005 (approved by order of the Ministry of Taxes and Duties of the Russian Federation of October 12, 1999 No. AP-3-14 / 319).

Deadline for the land tax declaration for 2016 for legal entities

The deadline for submission of the land tax declaration for 2016 for legal entities and for individual entrepreneurs is different. Companies submit a land tax declaration for legal entities in 2016 before February 1, 2017 according to paragraph 3 of Art. 398 of the Tax Code of the Russian Federation.

Individual entrepreneurs pay land tax for 2016 on timespecified in the tax notification from the tax inspectorate after receiving it.

Who and where submits the land tax declaration for 2016

Companies owning land property or using land on an irrevocable basis are obliged to submit a declaration to the Tax Inspectorate at the end of 2016, in accordance with Art. 398 of the Tax Code of the Russian Federation.

Declarations are also submitted by legal organizations that receive benefits under Art. 387 and 395 of the Tax Code of the Russian Federation or exempt from tax.

Attention! Since 2015, individual entrepreneurs and businessmen are equal to individuals and pay for 2016 land tax on tax notice on timespecified in the document.

Reporting must be submitted to the Tax Inspectorate at the location of the land plot. The exception is the largest taxpayers and investors under a production sharing agreement. They submit reports to the inspection at the place of registration of the main office.

Penalty for violation of the term of delivery of the land tax declaration for 2016

If the deadline for the delivery of land tax for 2016 for legal entities is missed, inspectors will fine the company

according to art. 119 of the Tax Code in the amount of 5% of the unpaid tax for each full or incomplete month, starting from February 1, 2017.

It is important to know! The amount of the fine can not be more than 30% of the amount specified in the declaration, and the fine is never less than 1,000 rubles.

Tax declaration for land tax for 2016, basic provisions for its filling

So that the company is not fined, it is important not only to meet the deadline for the delivery of the land tax declaration for 2016, but also to fill out a report without errors. The tax return includes three sections - a title page, section 1, section 2 - each section is drawn up on a separate sheet.

Title page- the cap is filled and all the specified details.

Section 1 “The amount of land tax payable to the budget” - this section directly applies the tax amount - line 021. Also, if the local administration establishes a quarterly or so-called advance payment of land tax in 2016, then these amounts are reflected in lines 023 , 025, 027. Otherwise, a dash is put.

Section 2 “Calculation of the tax base and the amount of land tax” - this section should be drawn up for each land plot separately, including a separate sheet to be filled in and for each part of the plot share if the company is a share owner of the plot. It also specifies the procedure for calculating land tax in 2016 - lines 130 and 140. Tax incentives, if any.

The company fills in all sections of the declaration. If there are several objects of taxation on the territory of one municipality, then one declaration shall be submitted. But at the same time for each land plot you need to make a separate sheet of section 2.

Below is a sample of filling out a land tax declaration for 2016 with comments in the places where difficulties arise most often.

The land tax declaration is an official document that contains the necessary information on the collection and is subject to delivery to the authorized bodies within the statutory period.

It is necessary to compile it very carefully. In this material you will find all the necessary information on the declaration, namely:

- who is obliged to pass;

- deadlines;

- the form;

- penalty for failure to provide;

- sample fill;

- form.

Who should report?

Organizations that own or own land and are recognized as land tax taxpayers in 2016. Since it is local, it is payable to the budget at the location of the object. The authorities of the constituent entities of the Russian Federation set land tax rates by their legislative acts, therefore, they differ in different regions and should not exceed the limits allowed by the Tax Code of the Russian Federation.

In accordance with the amended Federal Law № 347 dated November 4, 2014 for individual entrepreneurs, the payment is calculated by the tax authorities, after which they send a notice of its payment by mail.

Deadlines for reporting in 2017

Land tax declaration deadlines 2017 - for enterprises no later than February 1, 2017, this period is set by the Tax Code of the Russian Federation in paragraph 3 of Article 398.

Reporting form

Land Tax Declaration 2016 and the procedure for filling is regulated order of the Federal Tax Service of Russia No. MMV-7-11 / [email protected] from 10.28.11 "On approval of the form and format for the submission of a tax return for land tax in electronic form and the Procedure for filling it out". The form on the KND - № 1153005. A declaration on land tax can be downloaded at the end of the article.

Penalty for failure

If the organization misses the deadline for submitting the declaration, it will be liable in the form of paying a fine in the amount of 5% of the unpaid tax amount or on the basis of the information provided in the completed declaration. Penalty is charged for each complete or incomplete month since the day established for the submission of the report. The fine should not exceed 30% of the amount of tax and can not be less than 1,000 rubles.

Sample fill

The tax return for land tax is a sample of the filling, the rules and the filling procedure are governed by Appendix No. 3 to the Order of the Federal Tax Service of Russia. The document consists of three pages:

- 1 page - Title page;

- 2 page - Section 1. The amount of land tax payable to the budget;

- 3 page - Section 2. Calculation of the tax base and the amount of land tax.

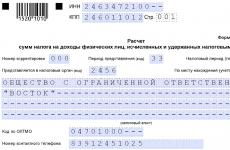

The tax return for the land tax sample filling for the Russian commercial organization LLC “Tulip”, which is registered in the federal city of St. Petersburg. Carries out activities in the wholesale trade of food, beverages and tobacco, the company owns one land plot located in the same city, the cadastral number is 60: 003: 56915938: 63 / 01012015. The cadastral value of the plot is 1.2 million rubles. The organization owns it for 12 months, the tax rate is set at 1.5%. CSC 182 1 06 06031 03 1000 110. OKTMO - 40306000 LLC during the year made advance payments to the budget and transferred the following amounts:

- I quarter 4500 rubles.

- II quarter 4500 rubles.

- Quarter III 4500 rubles - see the procedure for calculating advance payments in the section on completing Section 1. A sample of the completed declaration can be downloaded at the end of the article.

1 page - Title page

sample fill form

The title page is filled out directly by the payer of the collection, with the exception of the field “filled in by a tax authority employee”.

Consider a sample of filling out the land tax tax return for 2016 for each field separately:

- In the "INN" and "PPC" indicate the corresponding values, then they are automatically put down on each page.

- In the “Adjustment number”, if it is submitted for the first time, we indicate 000, with subsequent adjustments 001, 002 and so on.

- In the “Tax Period”, we enter the required number of the tax period. For the calendar year - 34.

- In “Reporting year” - the date of filling out the form.

- Each inspection to which reports are submitted has its own non-recurring four-digit code, in its IFTS or on the official website of the Federal Tax Service. The 2 digits of the code at the beginning indicate the region, the other 2 digits indicate the code of the inspection itself. The land tax declaration for 2016 is submitted to the Inspection of the Federal Tax Service on the location of the land plot or share in the land plot. In our case, the IFTS No. 9 of the Central District of St. Petersburg is indicated.

- The taxpayer shall affix the code at the location (accounting). According to the conditions of our task - 270.

- The name of the organization is entered in the most empty and long field of the title page, separating words from each other by an empty cell. For our example: OOO Tulip.

- The code of the type of economic activity of the taxpayer, is indicated using data from OKVED. In our case, OOO "Tulip" OKVED 46.3.

- In the next line enter the payer's contact phone number.

- Next, put down the number of pages to be submitted to the inspection. Our company LLC Tulip delivers a report for 2016 on 4 pages, without attachments.

- In the place where it is necessary to indicate the taxpayer - we affix the value 1 and the name of the director or proxy representative.

- At the end put the date and signature.

- In the “Name of the document confirming the powers of attorney” - a dash, since the report was signed by the director of the company himself.

2 page - Section 1. The amount of land tax payable to the budget

sample fill form

- First, you must specify the name of the agreement on production sharing, since in our situation it is missing we put a dash.

- In 010, we write the budget classification code of the ACC in accordance with the legislative acts of the Russian Federation on budget classification. Every time we check the relevance of the indicated BCF. Our allotment is located in the city of federal significance of St. Petersburg - we indicate the BCC 182 1 06 06031 03 1000 110.

- In 020 “OKTMO”, the code of the municipality in which territory the payment of the mandatory fee is made is indicated. For our company, in the land tax declaration 2016 we will enter 40306000.

- 021 - the total amount of payment, calculated and payable to the budget according to the relevant codes of the BCC and OKTMO. The value indicated in paragraph 170 and 280. 18000 rubles, we look at the counting rules in the field 170.

- From 023 to 027 recorded values of the advance payments paid for 1, 2 and 3 quarter, respectively.

Advance payments =? * interest rate * cadastral value of land (share) =? * 1.5% * 1200000 = 45000 rubles.

- 030 is calculated as follows: 021 - (023 + 025 + 027). If the result is a value with a “-” sign, then a dash is written everywhere.

- 040 = 021 - (023 + 025 + 027). The amount is calculated to decrease, therefore if in the end it goes:

- negative value - put it without a minus sign;

- positive - put a dash. In fields 030 and 040, under the terms of our example, we put down dashes.

- After filling in all the data at the end of the page, the director of the organization or his representative puts his signature and date.

3 page - Section 2. Calculation of the tax base and the amount of land tax

sample fill form

Consider a sample of filling in the land tax tax declaration 2016 for each field separately:

- TIN and PPC is automatically affixed from the first page.

- We enter the cadastral number of the plot, this number is entered in the certificate of state registration of ownership, from an extract from the USRRP or from a cadastral passport. 60: 003: 56915938: 63/01012015

- 010 of order of the Ministry of Finance No. 150n of December 16, 2014 select and specify the budget classification code.

- 020 from the All-Russian Classifier of Territories of the Ministry of Defense we affix to the OKATO 2016 Land Tax Declaration.

- 030 of Annex No. 5 to the order of the Federal Tax Service No. MMB-7-11 / [email protected] select and specify the category of land code. Other land - 003008000000.

- 050 from the relevant documents of the Federal Registration Service or from the cadastral passport we take the cadastral value of the site.

- 060 prescribe the size of the share. If the land belongs entirely to the organization put a dash

- From 070 to 120 in the declaration fill out the relevant information about the benefits that we take from the Tax Code of the Russian Federation and from documents confirming the right to benefits. In most cases, businesses do not have benefits. In our case, there are no benefits either, so dashes are put down.

- 130 here indicates the cadastral value of the object. We have 1 200 000 rubles.

- We take the rate 140 from the legislative acts of the local level of regulation, since the collection is local. For the category of our site applies a rate equal to 1, 5%.

- 150 indicate the term of ownership of the site during the tax period. Indicated in full months. Full months 12.

- 160 is calculated as follows: p. 160 (Kv) = Tenure / 12, we have = 1, since Tulip LLC owned a plot of 12 months.

- 170 is determined by the formula: 050 (cadastral value) * 140 (rate) * 160 (coefficient KV). This amount is reflected in the 280 field. 170 = 1,200,000 * 1.5% * 1 = 18,000 rubles.

- From 180 to 270 - fill, data on the existing benefits. In our case, they are not - put down dashes.

- 280 total amount of payment that the organization pays to the budget.